I am invested and continue to hold on to it…though i am not really happy with the management handles the share price issue…if you find something different which i am missing, please enlighten me…i infact have written an email today to their email adress provided on nse …lets hope for the best.

Think why they would release such news on one side and sell on the other side. Request you to always think skeptically even if you like the company.

Hi Mr.Mayur mengji,

Thanks for writing to us.

The transfer of promoter group shares were towards an increase in pledge requirement on a previously availed loan by the company. The transferred shares are under pledge and are still owned by them. These shares will be returned to the promoter group once the loan is repaid by the company.

As you know the company has no control over the price action of the share price, However we are effectively communicating with our investors through conducting quarterly conference calls or through emails they send us. The company is not getting delisted. What ever news regarding corporate action relating to the company will be published publicly on Stock Exchanges website.

With Best Regards,

Investor Relations Team…

This is in reply to my email sent to them…so they have not sold any shares…they have increased the pledge…

2 Likes

I believe Lycos needs to settle the Daum issue and continuously pay dividend for next few Qtrs to settle market fears.

that is right. Daun issue is very important for lycos. Promoter said it will take time for 1-2 quarters.Even if lycos has to pay the extra amount of another 16-20 million dollars it won’t hurt the balance sheet. Just to remind lycos has profit about 60 million $ protit per year

About auditor issue people try to fine out negative point in lycos. As per conferance call you may see the statement for auditor. each subsidy has different auditor and only last account is sorted out by Indian auditor.that + or - thing only. now where is the chance of manipulation?

I can’t understand your argument of auditor. PROMOTOR has already given statement about it and will change to another auditor.

I think this will clarify doubt about lycos.

Unbelievable that people are still trying to invest in this paper company (no customers, no real management, no real product ) . If you have already invested get out and if you haven’t invested yet, stay away.

1 Like

okay a newbie here, but been following the company as my friend has invested a lot in the company.

I downloaded the offical Annual report and been trying to find whether the company is really what it is or its just on paper.

First thing first,

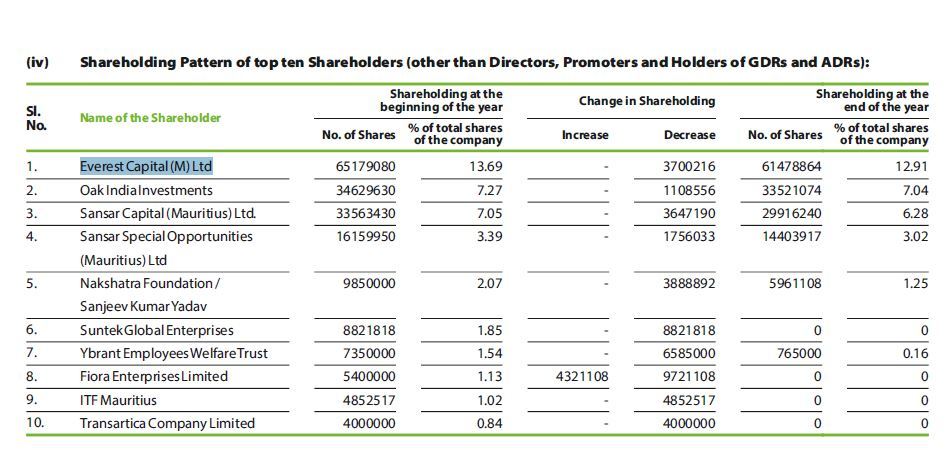

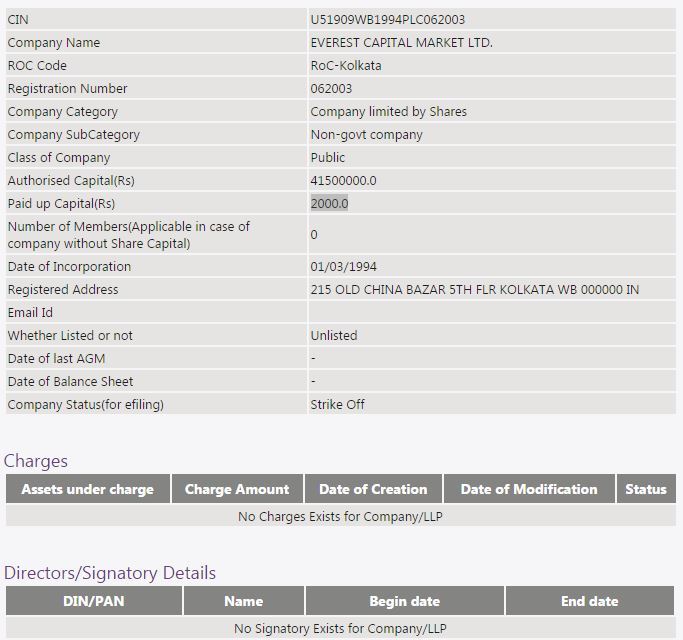

Everest capital market ltd is the main share holder of lycos. Owing 13% of the company’s share.

So i went to the offical MCA site and tried to find out the details of the company who hold 13% of lycos.

Now see this, the company is already strike off and having share capital of just 2000 Rs.

How can a company with a share capital of just 2000 can invest in lycos more than a 100 Cr.

And the problem is this company has been striked off way long. Although the company sold their shares.

Now the 8th and 10th company on the list were Fiora Enterpriese Ltd and Transartica Company Limited.

Non of which is registered on MCA. Maybe i can give benefit of doubt that maybe they must be a foreign company. Still they should write that down.

Being a Chartered Accountant myself, and have audited listed companies, I know who the books are cooked and by looking at the books of lycos, I can see there is something fishy.

However I think the share is currently at its very low around 11. If you are in the long game, you can certainly earn if you want to sell it around 20. Just quickly get in and get out. If you want to see this share as a multibagger, I certainly doubt that.

As this one a quick analysis of the annual report, will definitely post more once I get more time.

1 Like

“However I think the share is currently at its very low around 11. If you are in the long game, you can certainly earn if you want to sell it around 20. Just quickly get in and get out. If you want to see this share as a multibagger, I certainly doubt that.”

Fully agree with this statement. Too many controversial comments on this counter- company is internet based and so are the controversial comments. This is a speculative bet and only invest to the extent you are willing to write off in full.

1 Like

Bro its not Everest capital market ltd, its Everest Capital (M) Limited, a Mauritius based entity of Everest Capital!!

simple googling would have helped!

1 Like

THANKS crushkiller. I also check on internet. Both are different entity.Everest Capital(M) Limited and other two FII are mauritius base entity. Don’t post false message.

1 Like

A speculative bet here is purely a bet that a greater fool will come along and buy at a higher price. Also this is not an “internet company” as you generously classify, it’s just a good old fashioned scam. Show me one legit customer or one legit management employee or even one legit shareholder!!

1 Like

What is the basis of these statements? If you have any evidence please post so others can also examine it, otherwise please refrain from making generic statements which are not at all useful.

mvr99 you are right. MR.peguy has posted thing which do not have any base nor any link.I request Vp member to take note of this matter and do needful.

Media.net which is in similar ad tech space as Lycos, has been sold for 900 mln$, while having revenues of 232 mln$ (2015) which is a multiple of 3.9 times. Lycos on the other hand, with FY15 revenues of 1957 cr has a market cap of ~500 cr, which is a multiple of 0.25 times… shows the extent of undervaluation here !

You are asking me to prove a negative!

- Employees - Go to linkedin and get me the names of how many IITians/BITSians/NITians work on product development for this awesome tech company? Answer is zero

- Products - Can you explain to me in a simple fashion as to how this company makes money. What do they sell and who buys it? Ad tech is an inventory business with 20% gross margins. Since you are an investor can you give me a simple breakdown of revenues and profits by segment?

3, 730 crores of receivables, random numbers in the balance sheet which come in and go out (108 crores in non current investments), net profit of 405 crores and zero cash generation inspite of almost zero capex. You should learn to identify a meaningless P&L statement when you see it!

7 Likes

go through conferance call transcript posted on lycos website for last 2 years yo will get answer of all your question.

Boss simple question, what is revenue and profit by segment and who are the customers in each segment. Why do I have to go through a transcript to get this answer? If one doesn’t understand how a company makes money, one shouldn’t invest in it.

I am sure if I asked you that question for any IT stock or even tech stocks like Justdial or Infoedge you will have an instant answer.

I will try to answer the best I can :

-

From a simple search I can see on linkedin ~400+ employees for Lycos / Lycos media / Brightcom (you could have done this search yourself). I dont have time to go through each profile to check if there are IIT/BITS/NITians there, but let me assure you there are many great companies which dont have any employees from these institutions, and many companies full of such employees which have crashed and burned. Bill Gates and Mark Zuckerberg didnt even graduate, forget prestigious institutions, and they built great businesses, fyi.

-

If you dont know how this company makes money, what are you doing commenting on this board instead of reading some annual reports of the company first to get an idea of what the company does? Anyways, FYI, Lycos has multiple divisions but their primary one is Advertising. What they do in advertising, simply put is connect publishers (i.e. owners of websites, like cnn.com, facebook.com or even yourblog.com) and advertisers (Airtel, Coca Cola, Hyundai, ICICI, Lenovo, Maruti… all these are real customers of Lycos). Without companies like Lycos, Airtel would have to talk to thousands of websites to get their ads on each of their websites, and CNN would have to talk to thousands of advertisers to get all their ads for their site - Lycos solves this problem by being the intermediary and makes money in the process. Hope this is clear.

There is lot of tech related interventions they further do in the ad matching process e.g. contextual advertising, programmatic advertising, video and mobile advertising and so on.

Other smaller divisions are Lycos Media (which is a network of sites i.e. they are a decent sized publisher themselves) and Lycos Life (the new IOT division). Plus new ones like the Apollo JV.

All these above together form the Digital division.

They also have a Software Services division (which is like any other typical Indian IT services company) which is a legacy of their merger with LGS Global. Currently they report revenue and profits for these two divisions (Digital and Software) separately, please check their annual report (page 117 in FY15 annual report) or investor presentation for the numbers. -

They have been reducing their receivables (in terms of days sales) consistently for past few quarters, and the numbers are in line for their industry as far as I know. Cash flow statement from FY15 annual report (page 93) shows 275 cr cash generation from Operating activities, not sure where you got the “zero” number from. Where this cash is utilised is also shown on the same page.

They have ~20 global subsidiaries, which when clubbed together give the consolidated numbers. As such it is difficult to verify all the numbers, but that does not mean they are fudging anything, unless you can show specific inconsistencies in the numbers.

5 Likes

Ready made answer will not satisfy your query. You have to study this by your own. Mr. mvi99 has given good answer to you. But study by yourself to convince yourself.

Suresh Reddy himself is an alum of IIT KGP.