ONN vs. One8:

One confusion I have about Lux is ONN vs. One8. I have provided my thoughts on what could be the management rationale as well below, but thought I’ll put it down to share with other VPers.

If the company markets One8 to premium customers, won’t they be cannibalizing their ONN premium brand. And important to remember that One8 brand is not owned by the company but just manufactures and markets their products.

My guess for the management’s rationale is that One8’s products are super-premium (priced above Jockey) while ONN products are sub-premium (priced below Jockey). So they expect that it won’t cannibalise. Can others please provide their thoughts on the same?

Working Capital Management:

Working capital was my primary concern while initially going through the financials. However, very nice to see the management’s AR FY19 theme about improving their working capital. Improvement in working capital can improve cashflows of the company.

Penning down management’s thoughts on “Sales Quality” from AR FY19. Reading that annual report helped me deepen my understanding on why strong working capital is important for a company. I’m copying down some points from the annual report as it has been a pleasure going through those.

- There is greater respect for the company whose profits are reflected in the cash and bank balance than for companies where the profit is hidden in debtors

- A greater value is being attached to companies with a high cash flow accompanied with a slightly modest net profit when compared to companies with a high profit but with a low cash flow

- There is a greater business appraisal clarity: that the strength of a brand reflects in not just the velocity of sale derived from a distinctive consumer pull but the ability in being able to extrapolate from that consumer pull to getting trade partners to pay cash down for purchases

- There is a greater acceptance of the view that companies with smaller receivable cycles are less risked and more sustainable, generally inviting a superior credit rating that could, in turn, help mobilise debt at a lower cost and in doing so, moderate the Company’s break-even point

- A company with a large part of its profits and cash flows sitting in the bank accounts of its trade partners is not representative of a company with a sustainable long-term competitiveness; rather, it is the sign of a company whose corporate policies are run for the benefit of trade partners instead of for the benefit all stakeholders

- An increasing number of analysts are seeking companies that extend the power of their brands (corporate and product) to kick-start a virtuous cycle: stronger procurement muscle to be able to buy raw materials and resources at a lower cost in exchange for the ability to put cash down; utilizing this advantage to generate a margin higher than the sectoral advantage; creating a larger surplus when marrying this increased margin with growing offtake; utilizing larger suplus to enhance organizational value, visibility and respect.

Some other statements from management in the annual report include “During the last few years, companies like ours focused totally on maximising sales. We focused on sales maximization by increasing brand investments, working closely with trade partners and getting them to buy as much of our products as possible. Since the focus was on maximizing business quantity, the one reality that became secondary at our company was business quality.”

If one is openly coming up with such aggressive statements, any rational person should be willing to put lots of efforts to improve their working capital cycle.

Margin Improvement:

Also would like to pen down the factors driving the margin improvement over the past few years. Request others to add if they think I missed anything.

- Large scale Dankuni plant which brought in lots of efficiencies - Operating leverage, efficient machines, solar plant…

- Upgradation of Tech which helps them manage their inventory better - SAP HANA

Hopefully, the merger and their new focus on business quality would help improve it further.

Some things which are pinching me a bit are:

- Allegations on the promoter about being behind his son-in-law’s death

- Management boasting a bit too much in their annual reports. Have noticed that it is generally the case in my limited experience, but I feel it is a bit too much in case of Lux Industries

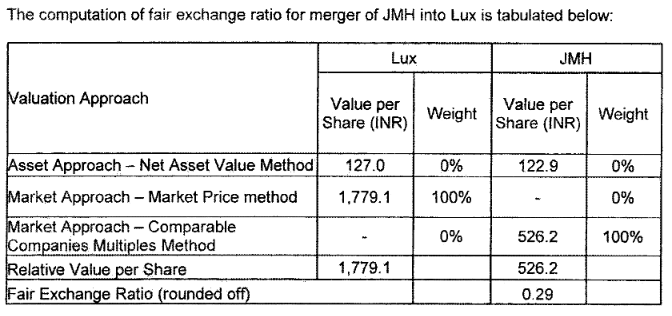

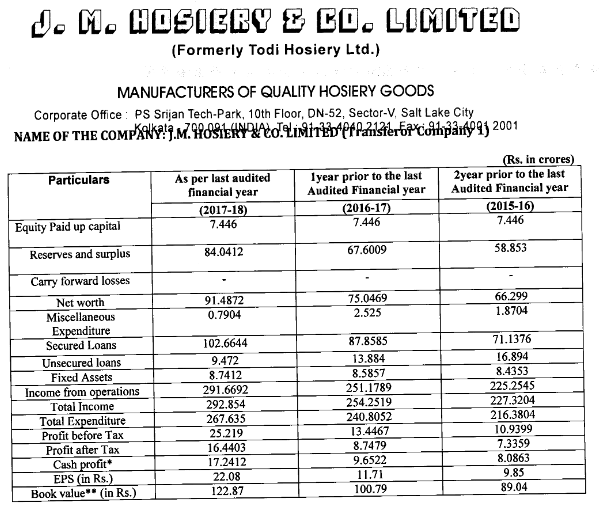

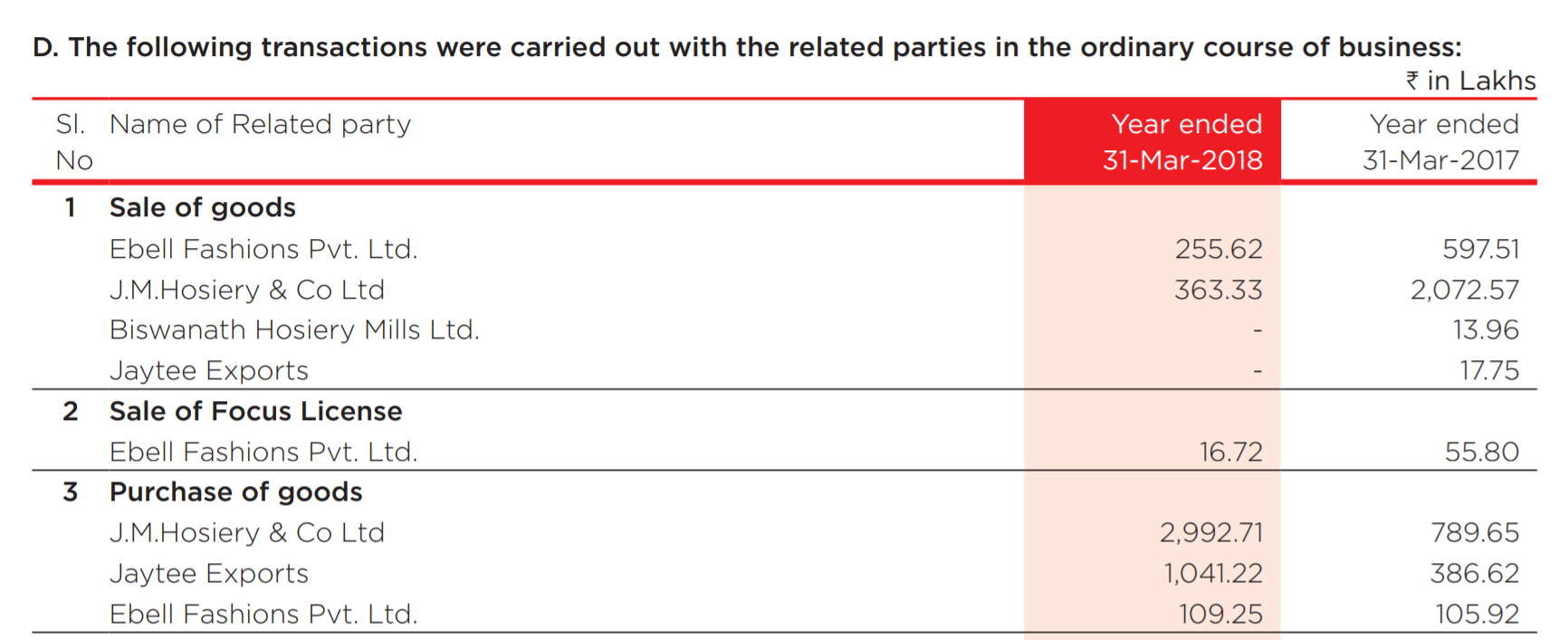

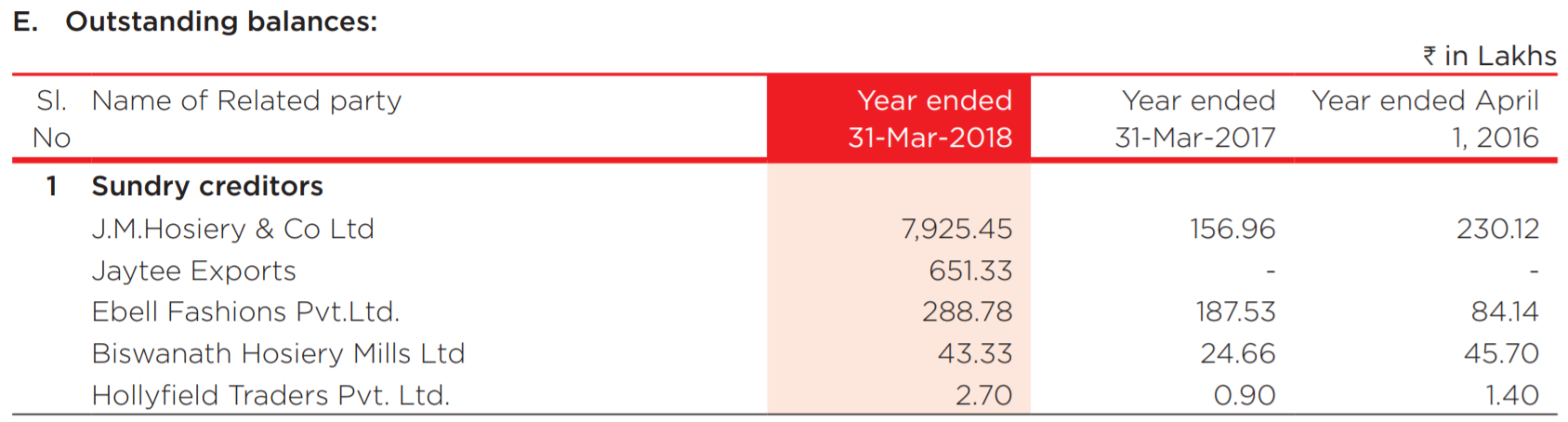

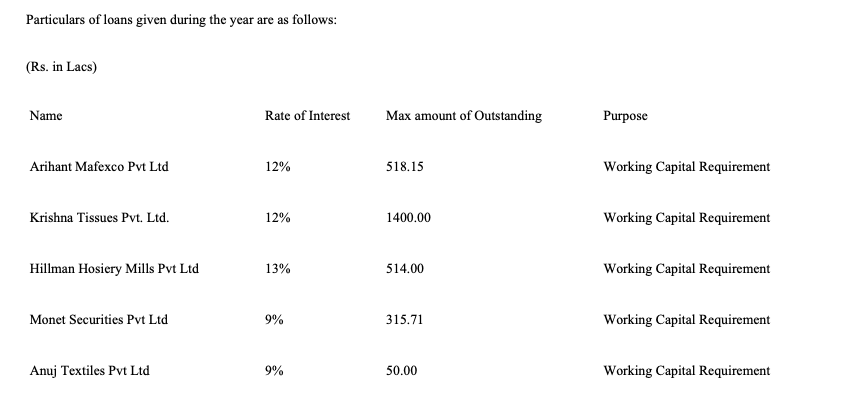

- Related party transactions but good to see the merger announcement by the management and hopefully that will reduce the size of related party transactions, in both absolute and relative terms

- Management repeatedly says Lux Venus seeing a lot of growth due to GST in conf calls, but is not visible in the numbers

- The company also keeps saying that their Northern, Western and Eastern markets contribute 63% of revenues and they are weak in Southern market. Assuming exports at 10%, it implies Southern markets contribute 27% to topline and that only means they are stronger in Southern markets. Not sure why we have this inconsistency

Overall, I felt the management is looking for respect / recognition from Mumbai by improving their business quality. Many of their actions suggest it: Margin improvement, Implementation of SAP HANA, Merger, Efforts to improve working capital, Pride in Annual Reports…

Discl: Just started tracking. No holdings. Please do your own due diligence. Not a buy / sell recommendation.