Lux Industries is a company engaged in manufacture of hosiery wear. The product range consists of men and women’s inner garments, leisure wear etc. Details of all its products with the photographs of celebrities endorsing the products are available on company website or in annual reports.

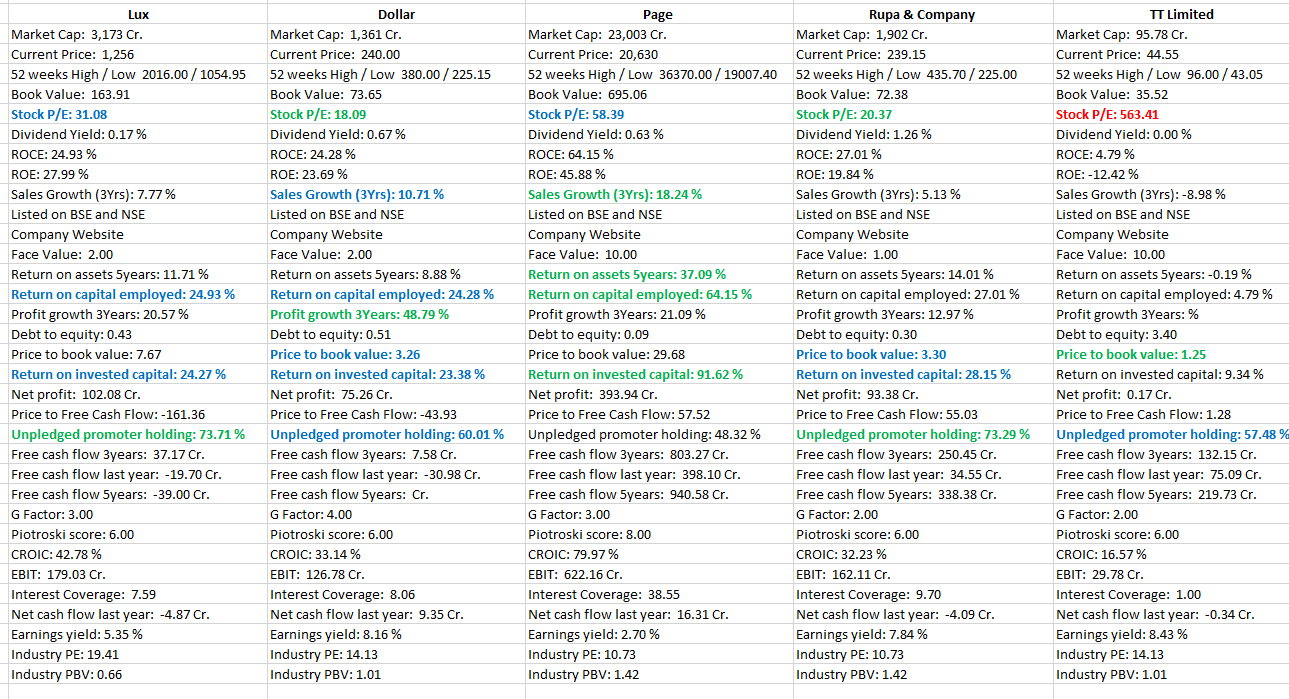

cmp 1250, market cap 3200 crores. Promoter holding 73%.

Peer is Page industries with market cap of 22000 plus crores.

MANUFACTURING FACILITIES

Company has manufacturing facilities at Agarpala, Dhulagarh, Ludhiana, Tirupur, BT Road, and a dream project at Dankuni West Bengal.

OPPORTUNITY SIZE

Addressable market in male and female innerwear in 2015 was 24000 crores which is expected to go up to 47000 crores by 2020.

This is because of expansion of category into leisure wear, sports wear etc and increase in per capita spend on the innerwear segment from Rs 150 to Rs 300.

PRODUCT RANGE

ECONOMY SEGMENT Lux Venus vests and briefs, Lux Karishma panties, Camisole, Leggies, Lux Cotswool therrmals.

MIDPREMIUM SEGMENT Lux Cozy big shot premium trunks, Lux touch panties, Camisoles, Leggies, Lux cozy glow collections, Lux inferno, Quilted thermals, Lux Cozy innerwear

PREMIUM - ONN, One 8.

Company has a wide product range from Rs 38 to Rs 1350 with over 5000 SKUs.

Luxury brand ONN has been growing at 30% CAGR.

Company stated aim is to increase sales of luxury range and thus improve margins.

Net Margins have improved from 4% in FY 13 to 10% in FY 19. Operating margins during same period has gone up from 6% to 15%.

SEGMENT WISE CONTRIBUTION AND MARGINS

ECONOMY REVENUE 34% EBIDTA MARGIN 8-10%

MID PREMIUM RANGE REVENUE 45 % EBIDTA MARGIN 13-15%

PREMIUM RANGE REVENUE 21% EBIDTA MARGIN 15-18%

Company targets to grow the premium range by 30% over next few years .

MANUFACTURING

Company is one of the lowest cost manufacturers with most of the work done inhouse. However stitching is outsourced to keep the employee base in check.

Company manufactured 20 crores innerwear pieces in a year which is the largest for any innerwear company in India.

DISTRIBUTION

Company has 950 plus large distributors and some with relationship over 35 years.

It has 160 large format stores which help in showcasing a large portion of the company’s product range. It has 9 exclusive brand outlets.

It is one of the few Indian innerwear companies to organise distributor and owner conference in and outside India.

Company has a pan India distribution network with strong presence in West and Central India with highest absolute sales coming from UP, MP and Uttarakhand.

Exports to 47 countries including those in Africa, asia and Europe and Australia. Focus is to be countries with demography similar to India.

ENDORSEMENTS

Lux has over the years roped in celebrity endorsements with personalities such as SRK, Sunny Deol, Varun Dhawan , Amitabh Bachchan etc.

Company has sustained brand endorsements of around 8% of total sales and spend 109 crores in FY 18 and 91 crores in FY 19 as advertising expenses.

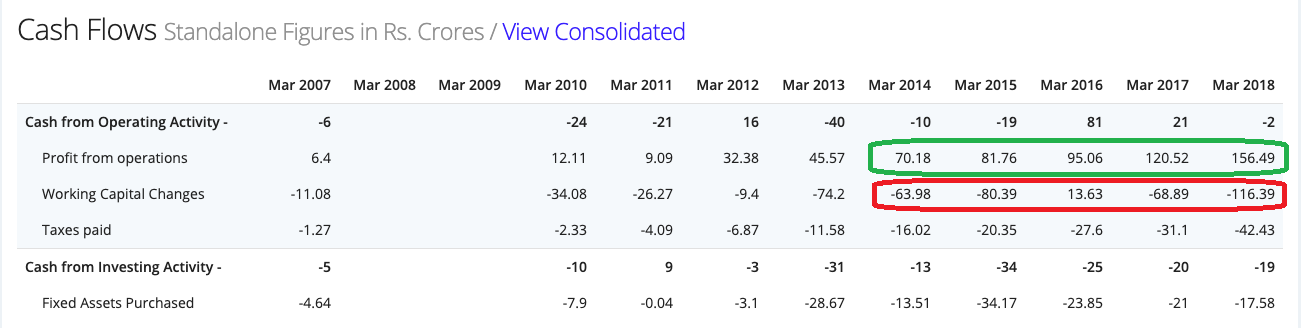

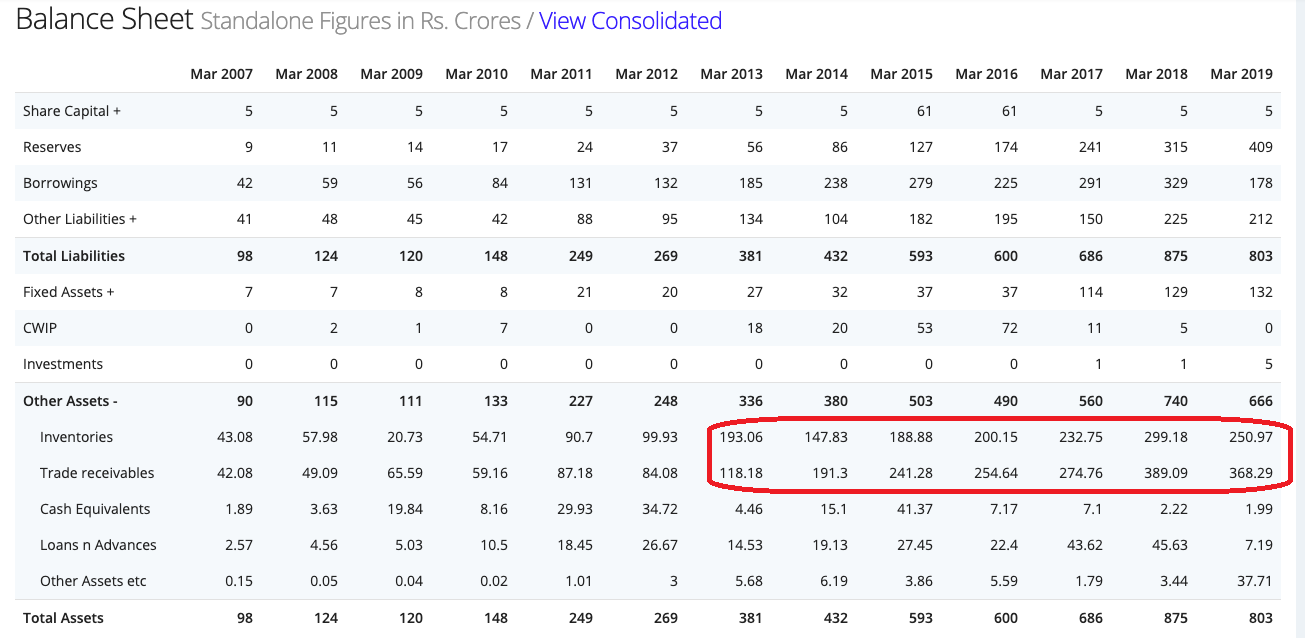

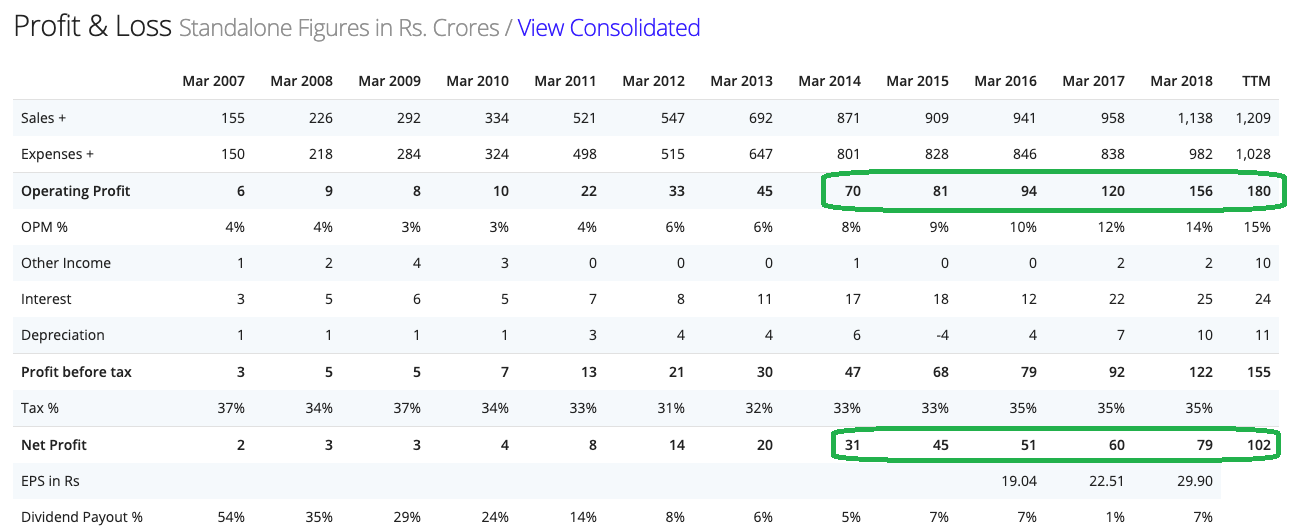

FINANCIALS

¨FY 19 REVENUES AT 1218 CRORES VS 1079 CRORES IN FY 18, INCREASE OF 13%.

¨EBIDTA INCREASED 21% TO 189 CRORES.

¨NET PROFIT INCREASED TO 101 CRORES FROM 78 CRORES AN INCREASE OF 30%

¨EBIDTA MARGINS IMPROVED FROM 14.5 % TO 15.6% AND PAT MARGIN FROM 7.2 TO 8.3%.

¨FY 19 EPS AT 40 PER SHARE VS 31 FOR FY 18.

¨LONG TERM DEBT AT 5.3 CRORES AND SHORT TERM DEBT AT 173 CRORES (DOWN FROM 316 CRORES IN FY 18)

¨SINCE FY 13, REVENUES HAVE GROWN AT 9% CAGR, PAT HAS GROWN AT 31% CAGR AND EBIDTA MARGIN HAVE IMPROVED FROM 6.3 TO 15.6% AND NET PROFIT MARGINS HAVE IMPROVED FROM 2.9% TO 8.3%.

¨FY 19 ROE 24.5%, ROCE 30% AND NET DEBT TO EQUITY 0.4%

GROUP COMPANIES MERGER.

¨JM HOSIERY REVENUE INCREASED FROM 293 CRORES IN FY 18 TO 328 CRORES IN FY 19.

¨EBELL FASHIONS REVENUES INCREASED FROM 198 CRORES IN FY 18 TO 254 CRORES IN FY 19.

¨BOARD OF DIRECTORS HAVE APPROVED THE SCHEME OF ARRANGEMENT OF MERGER OF THESE TWO COMPANIES WITH LUX. REGULATORY APPROVALS AWAITED.

VISION 2020

¨TO ACHIEVE TURNOVER OF 1500 CRORES HAVING 13-15% CAGR.

¨MAINTAIN SUSTAINABLE GROWTH IN EBIDTA MARGIN OF 100-150 BPS.

CONSTANTLY ADD NEW AND INNOVATIVE PRODUCTS TO GAIN SIGNIFICANT MARKET SHARE AND CAPTURE MORE EXPORTS FROM VARIOUS COUNTRIES

INVESTMENT THESIS

¨GOOD OPPORTUNITY SIZE FOR A DECENT COMPANY.

¨PREMIUM SEGMENT GROWTH TO HELP CONTINUE MARGIN IMPROVEMENT.

¨COMPANY HAS CONTINUED TO LAUNCH NEWER PRODUCTS AND CREATE NEW CATEGORIES LEADING TO EXPANSION OF ADDRESSABLE MARKET.

¨FOR A COMPANY WITH GOOD MANAGEMENT AND DECENT OPP SIZE, VALUATIONS ARE REASONABLE. CAN BE SOME RERATING IF GROWTH CONTINUES.

¨RISKS CAN BE SLOWDOWN IN CONSUMPTION, HIGHER TAXES.

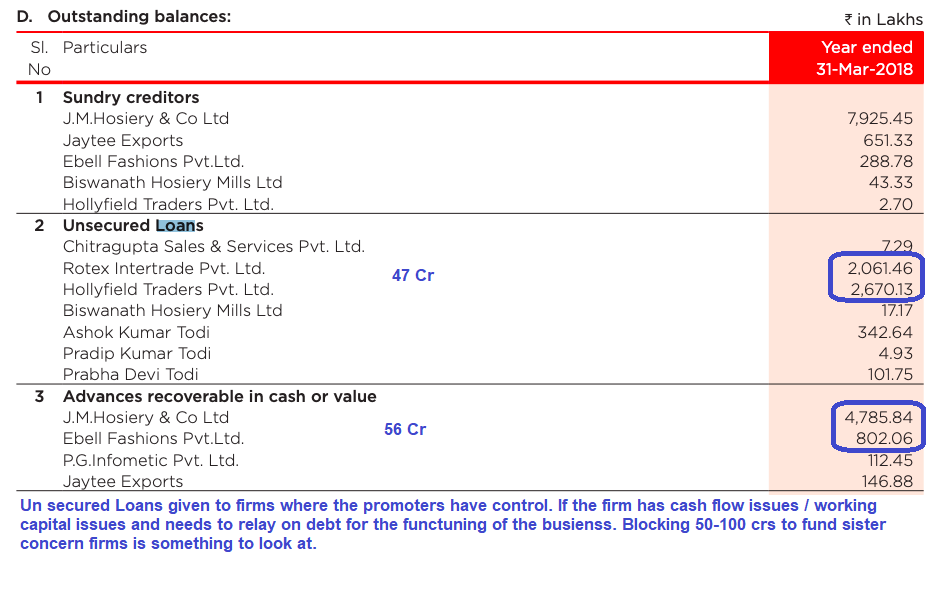

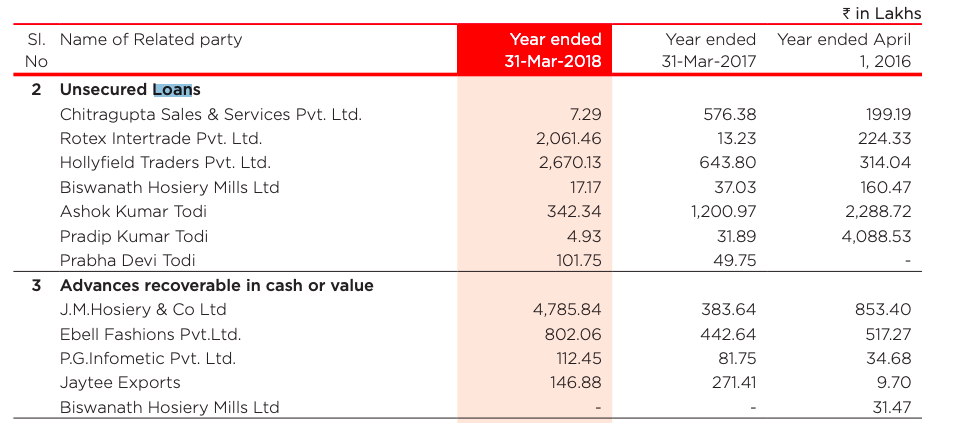

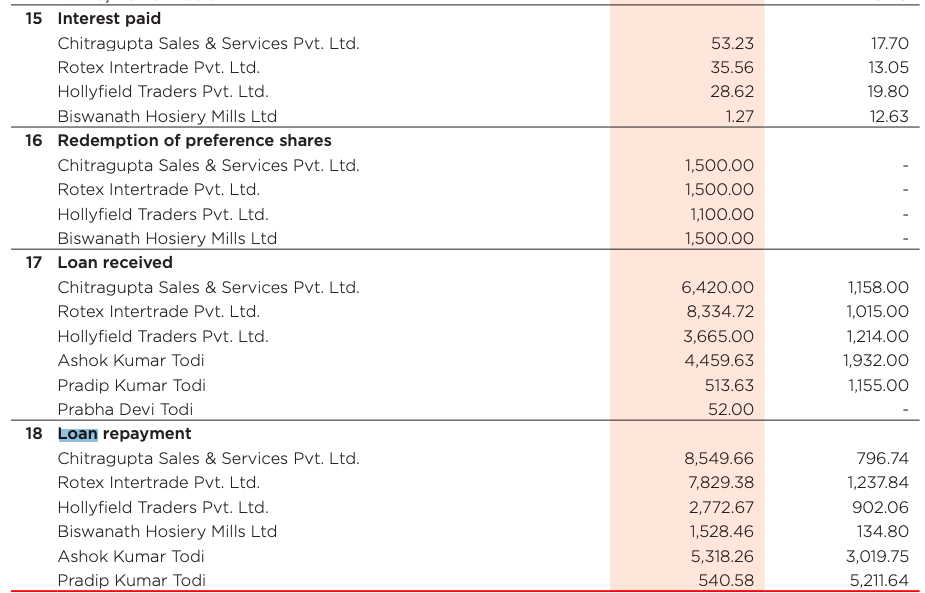

KEY MONITORABLE IS CASH FLOWS AND WORKING CAPITAL MANAGEMENT AS THE COMPANY GROWS.

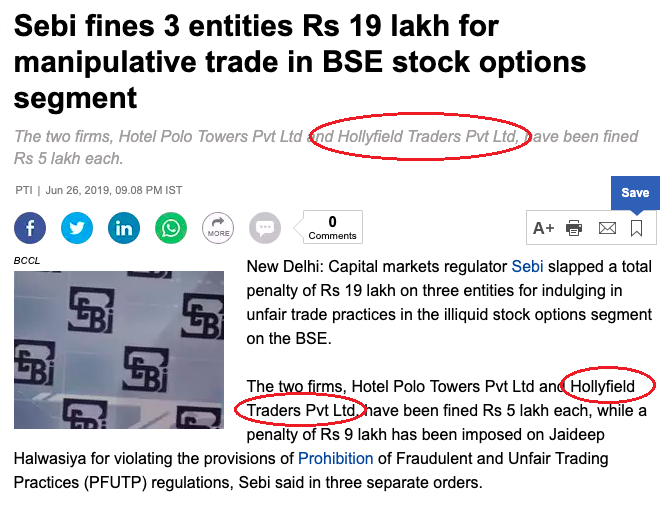

A CASE HAS BEEN GOING ON AGAINST THE TWO PROMOTERS IN SUPREME COURT FOR ABETTING SUICIDE.

disc: I hold an investment in the company.

This is not a recommendation and anyone contemplating buying or selling should do their own diligence or take advice of their financial advisor.