All the best for the upcoming Management Q&A.

Sorry I will not be able to accompanybecauseof the Kaveri groundwork in Nagpur belt. Am leaving tomorrow.

Below is my set of top of the mind questions. If we systematically query along these lines, and the Management answers transparently, we might be able to have a good comfort feel. As you mentioned before, the only way to get comfort feel (beyond what we have put forward) will be by talking to Management to know more.

You and Anil Kumar have done lot more work on the company, so kindly add to these base questions. Let;'s get the maximum out of the interaction.

Others - Please go through. Sometimes the questioning itself gives a good feel about the company (as it did for me over the last 2-3 days). You may feel compelled top contribute more and add/refine.

Question for Lumax Auto Technologies

Management

-

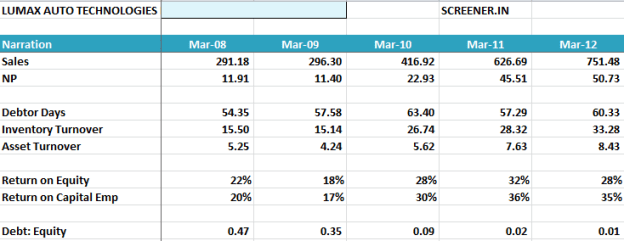

1. GROWTH

Lumax Auto Technologies has grown

rapidly in the last 5 years and more. Sales have grown by over 26%

CAGR while Net Profits have grown by over 40% CAGR. Kindly take us

through this journey and the key success factors.

-

2. QUALITY OF GROWTH

What is even more remarkable is the

quality of this growth. You have continuously reduced debt to almost

zero debt. Inventory turns have have gone up more than 2x in 5 years

(7x to 18x). Fixed Asset Turns have also almost doubled (4.3x to

8.3x)

This kind of numbers is perhaps

uncommon in Auto Ancilliary industry. Kindly educate us on what

makes this possible?

Is this sustainable, especially as you

gain more business from other segments like Gear- shifters (MSIL),

and Plastic Moulds (HMSI) which may be more capital intensive than

Lamps?

-

3. PRODUCT SEGMENTS.

Lighting (55%), Sheet Metal (11%),

Gear-Shifters & Parking Brakes (15%), Rest from Light Adjuster

mechanisms,, Mouldings.

Kindly educate us on the major product

segments.

-

| Lumax Auto Technologies Product Mix |

|

Lighting

|

|

|

|

Gear-Shifters & Parking Brakes

|

|

|

|

Sheet Metal

|

|

|

|

Level Adjuster Motors

|

|

|

|

Others

|

|

|

|

Total (Cr)

|

756.26

|

100.00%

|

|

Do you see this product-mix changing

significantly over the next few years, as you scale up other

relationships (non BAL)?

-

4. CUSTOMER SEGMENTS

BAL (49%); MSIL (6%); LIL (12%) ,

After-Market (21%)

Kindly take us through the major

segments, with some colour on the relationship, growth &

profitability picture,etc.

BAL: (Head

Lamps, Tail Lamps, Sheet Metal, Chassis)

What is the scope

of supply to BAL? All above and more?

Is it right to say Lumax Auto-Tech was

started at the behest of Rahul Bajaj? Kindly tell us more on the

long-term nature of this relationship.

Does LATL cater to all the major

platforms? Boxer, Pulsar, Discover? How are the plans drawn up for

these platforms. How early is LATL taken into confidence?

What percentage of BAL's requirements

is catered to by LATL? Platformwise?

How do you see this relationship

scaling up in the next 3-5 years? Can moulded products (around Lamp

assembly) be supplied to BAL also, post HMSI success?

Who are the other prominent

competitive suppliers to BAL in these categories/platforms?

--

LIL: (Head

Lamps/Tail Lamps, anything else?)

The next biggest customer is Lumax

Industries. What does LATL manufacture for Lumax Industries, and

why?

Given that it is a related company in

the same line of business as your biggest product segment, how do

you ensure there is no conflict of interest?

Could you throw some light on

following Related Party Transactions.

Sale of Raw Material & Components

: 108.96 Cr (104.23)

Sale of Finished Goods

: 31.92 Cr (22.14 )

Purchase of Raw Material &

Components : 19.70 Cr (8.48)

Purchase of Finished Goods

: 45.93 Cr (43.87)

-----

MSIL: Maruti Suzuki India Ltd.

(Gear-Shifters/Parking Brakes)

MSIL is the biggest customer for

Gear-Shifters and Parking Brakes. Is it correct that LATL supplies

around 70% of total Maruti's requirement for these 2 products?

Which platforms does this relationship

cover?

How do you penetrate deeper into the

relationship? How do you see this relationship growing over the next

3-5 years?

Is it correct that you have Toyota,

Daimler, Fiat and Tata Motors as new customers in Gear- Shifters and

Parking Brakes segment? How much does MSIL contribute today and how

much do the rest?

What are the plans for penetrating

deeper into these new accounts, and addressing new customers?

Who are the competitive suppliers in

this segment?

---

After-Market: (Tail

Lamps/Head Lamps, others?)

Is it correct After-Market Sales now

comprise a healthy 20% of Sales today? How has the after-market

sales grown over the years? What are the key success factors?

How strong is LATL's pan-India

distribution network today? What was the strength and level of

business 5 years back?

Trading Sales today ~212 Cr (212 Cr)

or 27% of Sales. Is it right to say most of Trading Sales address

after-market sales?

Is it right to say most of trading

sales comprise Lumax Industries products after-market sales?

What percentage of after-market Sales

is from LATL's products? How much from LIL products? And Others?

-

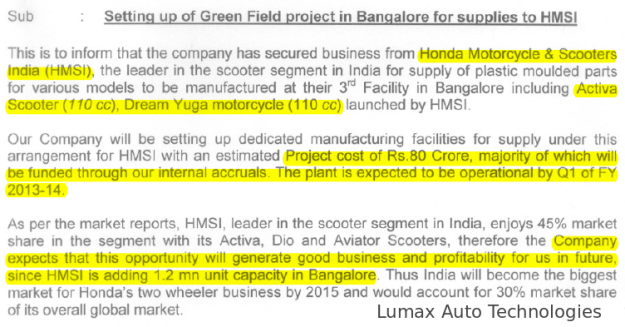

5. Honda Motorcycles &

Scooters India (HMSI)

Kindly

tell us more about this new relationship? Is the new plant on

schedule? When will commercial supplies start? Is this a sole

supplier relationship?

This seems to a

big investment (80 Cr)in the midst of the general auto slow-down?

How much has already been spent (FY13) and how much will be spent in

FY14? Kindly comment.

What is the

potential sales from this factory in FY14? What are the plans? Where

do you see Sales in 3-5 years from this segment?

This is for

plastic moulded parts? Is it correct to say that the plastic moulded

parts are for around the Lamp assemblies?

Who is supplying

the Head & Tail lamps? Is it Lumax Industries?

Is there any

restriction on LATL for approaching new customers for Head & Tail

Lamps? Any restrictions for approaching Japanese customers like

Maruti, Suzuki, Toyota's?

-

6. Lumax DK Auto Technologies

Can you tell us

more about this 100% subsidiary? The IPO prospectus mentioned setting

up Automotive lighting unit at Pantnagar, and Leveling Motor unit at

Manesar. Subsequently Gear-shifters & Parking brakes have been

also introduced?

Kindly give us a

break-up of product segment contributions from Lumax DK Auto?

| Lumax DK Product Mix |

-

|

Lighting

|

|

|

|

Gear-shifters & parking Brakes

|

|

|

|

Level-adjuster Motors

|

|

|

|

Moulded Parts

|

|

|

|

Others

|

|

|

|

Total (Cr)

|

310.66

|

100.00%

|

|

Kindly tell us a

little more on level Adjuster Motors? Is it true that you are the

only local manufacturers of this product currently in India? Is it

true that this is mandatory for use with Headlights today?

Who are your

customers currently? Where do you see this segment in 2-3 years?

Looks like this

is not a Capital-Intensive business â initial investment of ~4 Cr

only? Are there any other barriers to entry? Is it likley that OEMS

will buy Level Adjuster Motors assembly along with the headlights

manufacturer only, not stand-alone?

----

Kindly tell us

more on the Moulded Parts business? Is this catering to Head/Tail

light assemblies?

----

Is it correct to

say Gear-shifter & Parking brakes business is only carried out

from Lumax DK Auto?

----

So there seems to

be overlap between Lighting business and Moulded Parts business

between this wholly-owned subsidiary and parent company? How do you

prevent overlaps in jurisdiction between marketing/after-sales, and

customers, etc.

-

7. Lumax Industries Ltd

Lumax Industries

is a leading player in this market. Is it correct that it holds over

60% market share in Inidan market? Do you enjoy exclusive/majority

supplier relationship with some customers?

Kindly comment on

other leading players like Varroc, Minda Industries & Rinder?

What kind of market shares do they enjoy in Automotive Lamps? Do

they have exclusive relationships/majority supplier relationships

with some customers?

What are the

plans for this company along with the JV partner Stanley?

Given the

dominant industry position, it looks likely that either Lumax

Industries or Stanley should look to buy out the entire stake?

Kindly comment.

Is there any

possibility of merging Lumax Industries with LATL being considered?