Just a correction Flipkart uses gati, and bluedart … they dont own any shipper so far…

Logistics stocks zoom on re-rating hopes

Diesel price cut, Alibaba sales, Q3 show drive investorsâ interest into the sector

CHENNAI, NOVEMBER 17:

Shares of Transport and logistics companies such as Blue Dart Express, Transport Corporation of India, Gati, Allcargo Logistics, Patel Integrated Logistics, Snowman Logistics and Container Corporation of India have surged on the back of expectation of re-rating of the sector. Most of the shares have hit record highs in Mondayâs trade and hit the upper limit.

Betting big

Analysts tracking the sector said after Jeff Bezos of Amazon Inc and SoftBank Corp CEO Masayoshi Son evinced interest in e-commerce space, investors are now betting big on firms that could deliver goods.

Harish Vasudevan, Strategist, SVS Securities, said the fall in diesel price and blockbuster sale of $9.3 billion in single day by Chinese major Alibaba acted as a major trigger for the rise. According to him, the day is not far off for domestic online majors to catch up with Alibaba.

Before that happens, investors will look for deliverable companies which have pan India presence, as despite Indiaâs huge Internet population, e-commerce infrastructure remains relatively underdeveloped and ripe for huge growth.

Impressive earnings

According to analysts, these firms are already raking in huge earnings, which are reflected in the September quarter results. For instance, Gati, in which Janpanâs Kintetsu World Express owns 4.96 per cent, reported a consolidated net profit of â¹12.49 crore against â¹5.76 crore it reported a year ago, clocking a growth of 117 per cent. Consolidated income improved to â¹414.91 crore (â¹366.93 crore).

Similarly, Allcargo Logistics reported a growth of 51 per cent in consolidate net profit for the quarter ended September against the comparable period last fiscal while consolidated revenue jumped 37 per cent to â¹1,476 crore.

Already Gati, Transport Corporation of India and Blue Dart Express have seen a steady increase in foreign investors investment this fiscal. However, Concor saw a decline in FIIs interest while Patel Integrated yet to attract institutional investments.

Global fund major Nomura has estimated that Indiaâs e-commerce industry could more than quadruple to $43 billion over the next five years, driven by online retail.

Benefits in store

Motilal Investments in an analysis said: âWhile 50-60 per cent of the delivery logistics today are handled by the large e-tailers themselves, this proportion may reduce as the proportion of sales to lower-tier cities increases and e-tailersâ focus on bottomline picks up. Delivery costs a platform owner 8-10 per cent, implying significant burn for firms today. Segments such as logistics, warehousing and payment gateways stand to benefit directly.â

According to Harish Vasudevan, the impending Goods and Service Tax (GST) Bill and expected general economic growth will further aid the sentiment in favour of the sector. GST would bring in stable tax regime and reduce carrying and forwarding agency costs for the logistics companies, he added.

hello everyone,

Just playing devil's advocate here.

I dont think valuations of logistics companies are justifiable. Agree that stock were RELATIVELY undervalued about an year back but giving such high multiples to companies a) who doesnt have much pricing power b) there is no barrier to enty c) no differentiating business moat is justified.

Only reason why these companies are getting higher multiples is because of SIZE OF OPPORTUNITY in e-commerce business.

Let play a number game here. Please see the attached file and check for yourself what are we discounting today.

| Col 1 | Col 2 | Col 3 | Col 4 | Col 5 | Col 6 | Col 7 | Col 8 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Open to discussions. What am i missing?

Regards,

Kunal

Apologies for weired formatting. Being my first post, i screwed up on this one.

Apologies again

Hi

I would disagree with your thesis. Logistics players do have a moat and it’s a powerful one. Pat Dorsey defines this moat as ‘Networking Effect’. Its like a virtuous circle where bigger the player gets, more the business it gets and in turn he gets bigger again. And once the mode of delivery reaches a certain capacity utilization, the cost of incremental package addition flows straight to the bottom line, creating huge operating leverage. Also if you speak to these guys, they talk about ‘charging per square foot’ of delivery. So very soon, we will see that if you order a pendrive on Amazon/Flipkart or if you order a book, you will be paying differently for shipping and handling. Just look at how big the companies in the US have become (UPS??)…Add to it the possibility of GST, which will cut costs drastically with reduced and smarter warehousing and less loss of time on the roads. Also as you eluded, ecommerce is a huge opportunity and one which is growing at 35-40% cagr. This growth should sustain in the foreseeable future, ensuring enough volume growth for years. Also things like retail boom, improving infrastructure, 3PL opportunities which will only add business. The unorganised guys with one form of delivery and that too with limited fleet, will not be able to compete with the national multi-modal players who reach every nook and corner of the country. Calculate the replacement cost of re-creating, for example a TCI (add price of warehouses, office locations, fleet, operations etc) with today’s real estate rates and you will see the barrier to entry…Even after laying down the positives, I would say that these might not be the greatest of businesses, since the capex requirement will be high but it is a business with multiple tailwinds

1 Like

Hi Akshay, I am not undermining the fact that some of the companies could see disproportionate gain if they continue to gain market share. The reason why I am not too bullish is because of following reasons: 1) there is no barrier to entry which means In the longer term very few companies will have advantage like Blue Dart (which again in my view is not trading cheap). 2) These companies dont have much pricing power except for few like Blue Dart. Hence you do see their margins ~7/8%. At the end of the day its a B2B business with low entry barriers. Also I believe companies like flipkart inorder to reduce their logistics cost either they will expand their own eKart logistics or would try to reduce cost as much as they can. Also going forward I feel that to reach last mile, we may see flurry of logistics companies trying to cash-in on the E-Comm boom. This we are already seeing with whole host of courier companies delivering orders in my home town. This does not give me much comfort on pricing. The entire story is about gaining market share. As you pointed out correctly that capex is definitely an issue as these companies still have only 40% reach of total pincodes in INdia. I am not getting into valuations for now as it would be unfair unless i understand the strong moat these companies have. Regards, KP

Hi KP,

As can be seen above, I have been invested in logistics companies since some time.

Therefore, trying to share my viewson couple of points raised by you. My views, I must point out may be biased

Entry Barriers Low = Yes. [But I believe one needs should look beyond entry barriers sometimes. I don’t mind investing in a company which operates in an industry where entry barriers are low, but there are barriers toSCALE going ahead). It is like a big tree in the forest which doesn’t allow other small weeds (that grow around it)to receive adequate sunlight. Hence yes, weeds grow but eventually they will die. It would be difficult for new entrants to replicate the size and scale of infrastructure and operations that Gatis and Bluedarts of the world would have built. And this barrier would keep on increasing for new entrantsby passage of time.]

Capex Intensive Business = Yes. (But this in itself creates a barrier for new entrants. Lot of start-ups in this space have died and would die due to lack of capital. Let me try to give an analogy although it might not fit exactly in this case. In US Amazon is the leader in online retailing. Would PE or VC be comfortable funding a new online retail start up that tries to compete with Amazons of the world. I don’t think so. Similarly once companies like Gati are able to become big, it would keep on becoming all the more difficult for new entrants to get funding. Hence this also would act as a barrier even if a player enters this segment. Again this barrier would keep on increasing for new entrants by passage of time.]

Other Ancillary Point with respect to small town players or unorganised sector(which I am sure most of us would know about):

Small players and unorganised players operating in towns etc.,would face headwinds as their price advantage (due to taxe considerations, etc.,) will start waning due to implementation of GST, as in transportation and logistics business there is a tendency to engage with unorganised playersdue totax considerations. Competitive positioning of organised players would increase. Share from un-organised players would go towards organised players. At present 90-95% share is with unorganised sector (had read in a report sometime back). Unorganised players would need to improve their service and efficiency levels, but above 2 factors would be a hindrance. Hence they would need to collaborate/merge or give up their business shareto organised players. Going ahead (long term)it would become imperative for unorganised players to collaborate (utilise supply chain facilities of organised players, etc.,), if not then either sell out or perish.

I also feel that, lot of manufacturers and end users in the long terms would not mind out-sourcing their logistics requirements to these players, once the sector is able to drive efficiency by supply chain re-enginnering, proper ware house mgmt., consolidation, etc., There are costs associated in the short to medium term but in the long term this would help in making the pricing competitive. In the long term we may reach a point where it would become more cost effective for manufacturers etc,. to hive of their own logistics arms and outsource the same.

Things like GST implementation, B2C e-commerce FDI (any money that comes in would flow to these players as any big international player would like to collaborate with players with established suppy chain), whenever implemented would only make things better for organised players.

There may be other points as well which can be discussed, but I have tried keeping my response directed towards points raised by you.

There is a lot that still needs to be done by the sector itself and in terms of other reforms etc., that would act as enablers for growth in the long term.

Not all businesses can be picked up on the basis of numbers as opporunities may take time to translate into numbers. Such businesses are easy to be invested into at lower levels when their stock prices are down. It is a difficult choice indeed at current levels as the valuations look very stretched and the margin of safety may be very low. I myself was taken aback by the steep rise in prices and these have been multibaggers for me. But fortunately enough, due to steep rise I have been able to book profits twice and then re-enter at lower levels making my holdings cost free.

I would continue to hold onto these for the very long term though.

Discl: Logistics contributes 13% of my portfolio at present(due to rise in stock prices). I have a basket of logistics stocks (micro and macro plays)which I treat as a single stock. Stocks include Gati (major holding in this basket), TCI, Snowman, and Gujarat Pipavav.

Cheers!!!

HR.

1 Like

Hi HR/Akshay, Points well taken. Just to summarize so that we are on the same page: 1) Business moat is there because they have strong distribution network 2) Low entry barriers but scalability will be a problem for a new player 3) Operating leverage will kick in as # of packets delivered increases 4) Itâs a high capex business 5) Companies with strong distribution network and availability of cash for expansion, will keep gaining market share. Please add if I am missing anything. Dissecting each points one by one: a) Business Moat: Agree with the fact that strong distribution network definitely do wonders for companies like FMCG; consumer goods. But they work mainly because of brand loyalty. Do companies like TCI really has a brand loyalty. This brings me to my point that do they really have any pricing power? I think not unless you have a become a PAN India player with service quality much better than others. b) Low entry barriers: Does scalability is really an issue for a well-funded player. Lets assume a big business house with enough capital on its balance sheet decides to enter into this segment looking at the size of opportunity. I am sure over a period of 3/5 years, assuming he remains committed to the business can have as good a franchisee as GATI or BLUE DART. I agree with the fact that scalability is a problem for player who don’t have enough funding but we have to think from longer term perspective that why canât this be done. Lets think like an owner of a logistics companies, say I have to deliver a parcel in a small town near Varanasi. I can always tie up with the best local vendor there. For me, my job is to deliver the packet to the airport/station and the local player can take up from there. This is beneficial for both the players as I don’t have to spend heavy capex and the local player gets more business. Win-win for both. c) Operating leverage: like every other business where fixed cost is high even this business will generate good operating leverage. As rightly point out by Akshay, Capex will be a problem for most of the players but I believe we will have more logistics companies than what we have right now. Yes like always some companies will gain disproportionately from the e-comm boom but which company will benefit remains to be seen.

Hi HR/Akshay,

Points well taken. Just to summarize so that we are on the same page:

- Business moat is there because they have strong distribution network

- Low entry barriers but scalability will be a problem for a new player

- Operating leverage will kick in as # of packets delivered increases

- Itâs a high capex business

- Companies with strong distribution network and availability of cash for expansion, will keep gaining market share.

Please add if I am missing anything

Dissecting each points one by one:

-

Business Moat: Agree with the fact that strong distribution network definitely do wonders for companies like FMCG; consumer goods. But they work mainly because of brand loyalty. Do companies like TCI really has a brand loyalty. This brings me to my point that do they really have any pricing power? I think not unless you have a become a PAN India player with service quality much better than others.

-

Low entry barriers: Does scalability is really an issue for a well-funded player. Lets assume a big business house with enough capital on its balance sheet decides to enter into this segment looking at the size of opportunity. I am sure over a period of 3/5 years, assuming he remains committed to the business can have as good a franchisee as GATI or BLUE DART. I agree with the fact that scalability is a problem for player who don’t have enough funding but we have to think from longer term perspective that why canât this be done. Lets think like an owner of a logistics companies, say I have to deliver a parcel in a small town near Varanasi. I can always tie up with the best local vendor there. For me, my job is to deliver the packet to the airport/station and the local player can take up from there. This is beneficial for both the players as I don’t have to spend heavy capex and the local player gets more business. Win-win for both.

-

Operating leverage: like every other business where fixed cost is high even this business will generate good operating leverage.

As rightly point out by Akshay, Capex will be a problem for most of the players but I believe we will have more logistics companies than what we have right now.

Yes like always some companies will gain disproportionately from the e-comm boom but which company will benefit remains to be seen.

Disc: not holding any stock in logistics sector as yet because two key things are missing to my likings: a) pricing power and b) Incremental ROIIC has been low so far and hence I am questioning my theory again and again on this sector to understand what am I missing.

Logistics sector fulfills the three aspects I look for while searching for multibaggers:

-

Huge size of opportunity - E-commerce and logistics are expected to grow 10 fold in next 6 years.

-

Scope of increase in margins - Due to lower crude oil price and expected efficiency improvement after

GST is implemented the margins will expand.

- Re-rating of sector possible due to increased growth prospects being recognized by the investors.

Regards

Naveen

1 Like

Friends,

Recently during my visit to a local post office I noted a banner of International courier service of post and parcels. Parcel service rates are almost at 50% discount as compared to gati or blue dart.

Indian posts may emerge as a biggest player in this sector…if beurocracy is reduced.

regards,

peush

Hi

I have been trying to understand the business models of GATI and TCI and in that process i have certain questions (would be glad if you could answer them) -

-

What is the exact difference between the Xpress business and the freight business of TCI? Unable to differentiate since both can carry small cargo to bulk cargo? Is it only because of door to door delivery?

-

Gati nowhere talks about Freight business, its just express and Supply chain everywhere. So does it mean that Gati has no freight business at all?

-

Do you have the breakup of Gati’s Xpress business and supply chain business? I am not able to find it.

-

Which one is bigger in terms of Xpress revenues? FY 15 XPS revenue of TCI was 660 crores. How much did gati make?

Would be great if anyone could provide clarity on the same.

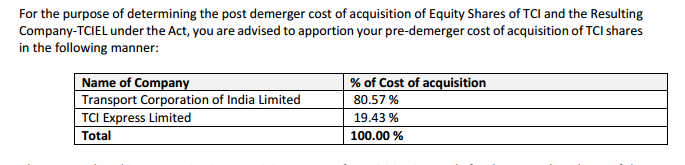

Transport Corporation of India Ltd has informed BSE that the Company has fixed August 29, 2016 as the Record Date for the purpose of Scheme of Arrangement between Transport Corporation of India Ltd (Demerged Company) and TCI Express Ltd (Resulting Company).

So anyone who holds the TCI stock before 29th August is eligible for a 1 share of Xpress against every 2 shares of TCI held.

I believe the situation provides small gain opportunity as the market might reward TCI Xpress for its growth potential and the overall growth that the door to door delivery is expected.

Disclaimer : Small amount investment.

TCI (post demerger) closed at 213. Is market valuing it 200 plus or we need to wait till Xpress is listed?

you will get 1 share of tci xps for 2 shares of tci held…so per share price of tci xps according to this calculation should be 414.