Company is not showing any sign of consistancy in performance (QoQ) after change of bussiness model from trading to branded formulation. The reason migth be higher API price which company was importing from China which now has stopped, domestic supplier are expensive. Company is coming with API plant, which is not so quick solution as it takes time for research (!) and manufacturing trials, stabilization of plant etc. Big pharma are suffering due to margin pressure, its interesting to see how management leads company in future.

Promotors groups acquired 12L shares in this week. Anyone knows whether these were bought from open market?

This is almost 5% of the total outstanding shares.

No that was not from open market, it was just a swap between existing promoter entities. No new shares were bought in total. Share holding remains same.

1 Like

Hey Guys, I had recently picked up this company and learnt a great deal about it from this thread. Since there has been no post on this for the last 9 months, I would like to start with some notes from the latest annual report shared with me by @yogansh.

Annual Report FY19 notes:

- Appointed Darshit A. Shah as CFO of the Company w.e.f. March 28, 2019.

- Promoter holding: 32.39% (PY 32.14%)

- However, when one looks at the top 10 public shareholders it looks like there are some family members (Patels) who are classified as non-promoters who hold more than 10% in LPL. Therefore, it seems that the cumulative shareholding is close to 43%.

- On product basket-

- Company’s main focus is on Cardiac and Diabetic Segments as we have till now achieved a good growth in these segments.

- Respiratory segment we have expanded our basket with new set of products, so we are expecting extensive growth in this.

- Revenue break-up:

- India: 155.6 Cr (PY 201.1 Cr)

- Export: 197.4 Cr (PY 124.4 Cr)

- 1 customer contributes more than 10% of the revenue.

- Subsidiaries:

- Lincoln Parenteral: Sale 50.86 Cr | PAT 2 Cr (47 Cr sale is to Lincoln Pharma)

- Zullinc Healthcare: Sale 3.48 Cr | PAT 10 Lac

- Savebux: Sale 12 Lac | PAT 2.64 Lac

-

R&D expense 4.20% (PY 3.58%) of turnover.

- Capitalized: 4.53 Cr (PY 3.58 Cr)

- Expense: 10.27 Cr (PY 8.08 Cr)

- Non-Current Loans given:

- Loans given to others 13.3 Cr (PY 6.28 Cr)

- Security Deposits given to Lincoln Parenteral (Subsidiary) 15.57 Cr (PY 14.66 Cr)

- Inter-Corporate Loans 2.5 Cr (PY 1.62 Cr)

- Loans and advance to others: 1.75 Cr (PY 4 Cr)

What I like about this company-

- Even though revenues look muted for the last 3-4 years, the company has reduced its trading activities and has forayed aggressively in branded exports segment. LPL had around 120cr of export revenues in FY17 and has done 116cr of export revenues already in H1FY20. This highlights their focus on their exports business. Purchase of stock-in-trade has reduced from 210cr in FY16 to 52cr in FY19.

- Margins seems to be higher in the export business and hence PAT has increased significantly from 12cr (on a revenue of 210cr) in FY14 to 49cr (on a revenue of 366cr in FY19).

- The company has reduced its long term borrowings from 25cr in FY15 to 0.5cr as on Sept’19.

- LPL has spent 54cr on R&D since FY14 out of which 15cr was spent in FY19 alone.

- LPL claims to have 4 patents and over 1700 product registrations with 700 more in pipeline.

- The company is planning to set up an API unit which is a positive but has not provided with updates on this. For the last 3 quarters their business presentations carry the same update on it- “Applied to Pollution Control Board for permission of APIs Unit.”

Key Negatives-

- Debtor days have deteriorated after export revenues picked up.

- The company has given loans and advances and hasn’t given details on them. For example, loans to others at the end of FY19 was 13.3cr and another 1.75cr for which no details have been provided. Similarly, LPL has given interest free security deposits to its subsidiary, Lincoln Parental, of 15.57cr. And some inter-corporate loans of 2.5cr.

- Advance to suppliers under Related Party to Sunmed Corporation of 1cr

- Even though managerial remuneration looks low at 1.27cr, there are a couple of entries in the Related Party Transactions where the promoter family is taking away 94L in commission.

- Intense competition in the domestic generic formulations industry, which limits the company’s revenue growth in the domestic market and constraints its pricing flexibility

If the company can reduce these related party transactions and improve their communication with the investors (business presentations have been similar for a lot of quarters now) then there can be real value unlocking done. The company is long-term debt free and export sales are increasing which have better margins. This coupled with their investments into R&D and a lot of products in the pipeline waiting for registrations augurs well for the company.

Disc: Tracking

12 Likes

I have a small (2%) tracking position in this company. Have read last few years of annual reports, this thread and also saw some videos from the company on YouTube.

Has anyone been able to figure out reason for the high trade receivables ?

I was looking at some metrics like trade_receivables/sales in a year. The midcap pharma companies I have invested in, the number is around 10%-25%. For great mid-cap/large-cap companies(Dr reddy’s, Cipla, Aurobindo) as well this number is close to 20-25%.

However, for Lincoln Pharma, this number is around 42%. This is what worries me. The company has a market cap of 300 odd crore and trade receivables of 148 cr. How does this make sense?

I also dug through the 2019 Annual report (https://www.lincolnpharma.com/wp-content/uploads/2019/09/Annual-Report-2018-19-1.pdf) and found some things :

- If you CTRL+F for “trade receivable” You come on to the page 58 of the annual report (page 60 of PDF) where it says that trace receivables are explained in Note 14. I go to note 14 which is page 78 of annual report (page 80 of PDF). The thing which confuses me here is why “trade receivables considered good” keep growing every year. If they are considered good, when would they be paid to the company? This row keeps growing every year!

Another thing to note is the following line on this page:

“Details of receivables from firms / private companies in which directors of the company are partners / directors (Please refer note no. 53)”

Note that note 53 is printed as note 52 (which occurs twice) in this annual report. Thankfully the related party trade receivables are on lower side compared to total trade receivables.

@aga.ayush11 @yogansh @ayushmit any idea why the trade receivables are growing every year but management is still showing them as “good” and not taking provisions?

2 Likes

Hi Sahil,

Rather than looking at absolute amount of trade receivable, I look at debtor days. Though they are on higher side for the company but they had improved a bit in recent years (2016 seems to be aberration) vs 140-150 days few years back (most of the export oriented pharma cos have debtor days of 90-100 days as Lincoln is exporting more to African countries in its own brand, it might be a bit higher at 120 days)

I feel there have been some small improvements in the company over last 2-3 years and this reflects in overall ROCE too.

I’m aware that there has been a poor past for this company and people might have poor opinion but there seems to be some changes happening with the involvement of next generation who have grown the export business in a decent way and seem to be trying to improve things. Importantly the company has become almost debt free.

Overall - i agree with the concern you have raised.

15 Likes

Results for Q4’20 and FY20 are out:

Some key highlights for me:

- For FY20: The trade receivables have gone down from last financial year. From 123cr (FY19) to 101cr (FY20)

- For Q4’20: PBT has gone up substantially from 7.2cr to 11.5cr.

- For Q4’20: Although PBT has gone up, PAT has been roughly flat (8.5cr to 8.9cr). This is because last year the tax was only 0.2cr whereas this year it was roughly 2.6cr (including some deferred tax).

- Overall EPS for FY20 is at 25.7 versus 24.4 last year.

- Operating Cash flow has gone up from 53cr to 75cr (In FY20). The increase is largely due to the decrease in trade receivables.

- From page 16: "During the FY20, Company had paid its outstanding debt to the Financial Institution and now it become a zero net-debt company. ". Although I couldn’t understand this from the financial statements since it still seems to have some long-term borrowings in the balance sheet.

Waiting for the Annual report with hopes to see management’s commentary about this financial year.

Disc: 4-5% of direct stocks PF and looking to add more at lower levels.

2 Likes

Net-debt means debt adjusted for cash. After debt repayment, cash on the books is higher than the debt, hence net debt free.

3 Likes

Interesting management interview

5 Likes

809867be-fc7e-434d-b47f-eb912176e3f9.pdf (191.8 KB)

In this exchange filing Co i have read few days back Co is not sounding bullish in the first half. They are saying that there domestic market is impacted due to lockdown. Also stating that some price increases of end product due to increase in api prices. But in the interview they are giving growth guidence for the quarter. Am I not understanding something. If I am wrong plz guide. Thx in advance

Hi,

Decent quarterly results.

Company has launched products to boost immunity.

Tracking for investment.

Thanks,

Deb

4 Likes

@ayushmit Hi Sir, good results from Lincoln pharma and now net debt free as well. Entering into EU market also. Cheap valuations. are you still tracking it? your views would be helpful. thanks

1 Like

Decent set of numbers Reported by Lincoln Pharma.

My interpretations based on Q1 results and management interview to CNBC TV-18:

- The percent of exports in revenue is growing. From 11% of total sales in FY13, it grew to 56% of total sales in FY20 to about 78% in Q1-FY21.

- Cost of materials consumed has gone from 21 cr to 27 cr YoY which is a jump of about 29%. Since sales have only gone up 7%, does this depict a reduction in pricing power for the company?

- Changes In Inventories of Finished Goods, Stock-In trade and WIP has gone up from 1cr to 7cr. Not sure how to interpret this, but this potentially represents products for domestic sales which could not be sold due to suppressed demand due to covid-19.

- Total Revenue up 7%, Net profit and EPS up 23% YoY. Profits outpaced revenue growth mostly due to reduction in costs. For example, employee costs went down from 15cr to 13cr.

- Company has received EU GMP certification from Germany FDA and plans to start selling in EU sometime in this financial year.

- CNBC TV-18 anchors were upset with the management for guiding for 15-20% growth in Q1 and only achieving 7% growth. Mr patel tried to clarify that their anticipation of covid-impact was not accurate until now.

- Has guided for 25-50% revenue growth for rest of FY. My 2 cents are, small businesses face highest amount of uncertainty. Sometimes management might feel pressured to provide guidance. I would not take such guidance seriously.

- Vitamin C+Zinc tablets referenced above only expected contribute 10cr to topline. Total opportunity size in India is 150 cr.

All in all, would be exciting to see how the rest of the FY pans out for them and whether they can start adding serious top line growth based on exports to EU.

Disc: invested. Full portfolio here.

9 Likes

2019-20 Annual report Notes

On Covid-19 affecting the company

Coronavirus could have a moderate impact on the Company’s performance at least through the first half of financial year 2021.

Financial performance

Company achieved revenue of 376 cr as against 353 cr in the previous year. The PAT has increased to 50 cr on a standalone basis as against PAT of 47 cr in previous year representing growth rate of 6.3%

New product development

The Company manages the risk through careful market research for selection of new products, planning and continues monitoring. The company’s Research and Development (R&D) Department has developed many new Formulations. The Company has developed 600 plus formulations in 15 therapeutic areas and has a strong product/brand portfolio in anti-infective, respiratory system, gynaecology, cardio & CNS, anti-bacterial, ant-diabetic, anti-malaria among others. Company has a strong presence in the domestic market and also exports to more than 60 countries. With the EU certification, the company will expand its business network to 90 plus countries. Company has filled 25 plus patent applications and has been awarded with seven patents. For the next phase of growth, the company is building a strong portfolio in lifestyle and chronic segment especially women healthcare and dermatology to complement its strong presence in the acute segment. On the back of higher R&D, the company plans to launch many NDDS based products in India.

Number of National Locations

There is only one manufacturing unit, one R&D unit, and nineteen super stockiest across India. Company has a state-of-the-art manufacturing facility unit at Khatraj in Ahmedabad, Gujarat.

R&D

Total expenditure on R&D is 12 cr. This is ~3% of sales, down from ~4.2% in FY19.

Balance Sheet Statement

Trade Receivables have gone down by 12 cr (112 cr => 90cr). Also the breakup has become marginally better. Only 15% is considered to be high credit risk receivable in FY20 as against 21% in FY19.

Profit and Loss Statement

As the debt has gone down, credit costs (as a part of Expenses) has also come down (4cr => 2cr). Cost of materials consumed has gone up sharply by 25% (81cr => 101 cr). Given that total expenses have also gone up by ~ 24cr, this means the majority of expenses going up has been the cost of materials consumed. Revenue from operations has also gone up by ~23cr, which means that broadly speaking, the company was able to pass on the increase in cost of materials in terms of the pricing of their products.

Cash flow Statement

Largely due to a much better receivables position (and also in part due to better taxation), the net cash flow from operations has gone up by 40% from 50cr to 70cr.

3 Likes

Slow sales growth any concern here?

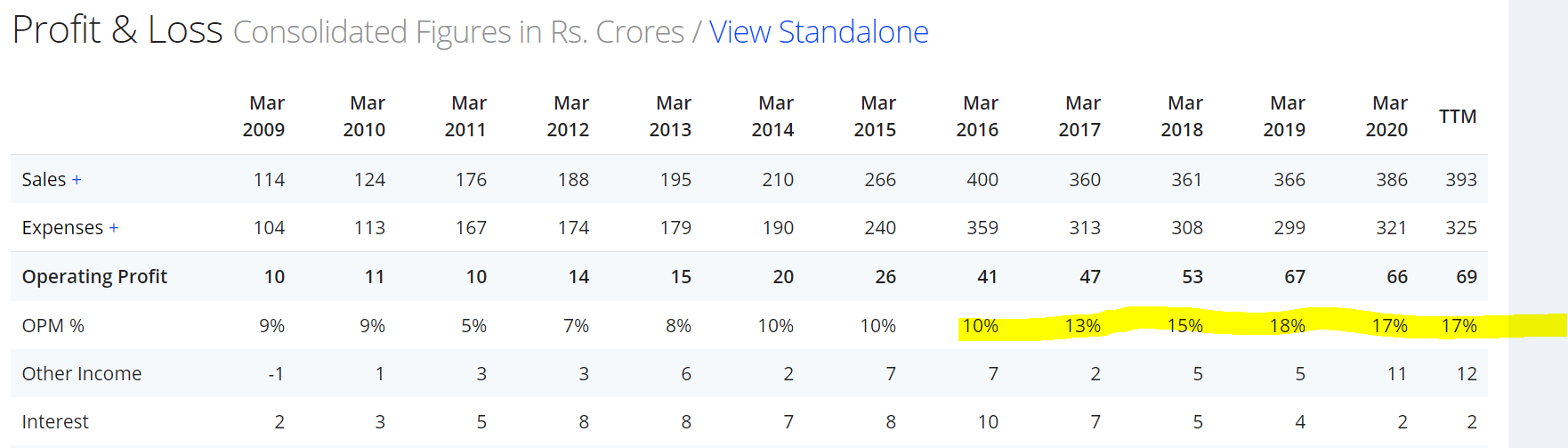

I would like to get some help in understanding the sales growth prospects as the CAGR in Sales is still negative from FY 2016 although the OPM is fairly good.

questions:

- Why is the topline not growing?

2.Are there any markers that points to increased sales growth in future

Other metrics like OPM, debt, cashflows look good but I doubt if i can be bullish on the stock for next 2-3 years unless there is an increase in the topline growth?

- Revenue till FY 16 was from

a. Selling of own brand

b. Contract manufacture at its units - Since FY17, they started to Defocus from Contract manufacturing and by FY18 they were totally out of it. This resulted in a decline in topline in FY 17, which later seems to pick pace.

P.S: I am not a professional analyst. I have been tracking this company and reading last 5 years AR. This is what i understood. Hope this Helps !! Regards

2 Likes

Lincoln Pharma gave good quarterly results. Margins were driven by higher gross margins and lower employee cost, other expenses were on a bit higher side.

-

Sales growth of 9.56% yoy.

-

PBT growth of 14% yoy.

-

Improvement in OPM from 22% to 24% yoy.

-

Highest quarterly PAT in last 12 qtrs.

-

Cash and equivalents of Rs. 104 cr as on 30.09.2020.

Regards

Harshit Goel

5 Likes

Its good to see now that Promoter bought around 1 Lakh share today…

4 Likes

Promoters have bought another 1 lakh shares. So now approx 1% increment in promoter holding.

4 Likes

Full English transcription of the interview with zee business March 2 2021

.

1 Like