Anyone understands what is up with their stock in trade and erratic topline qtr after qtr? Why for last 2 qtrs they posted 135-140 cr topline but extremely low profits? Why in this qtr, with 90 odd cr topline they posted 11 cr pat? Why stock in trade in last qtr was 90 cr? Lots of questions. They said they have closed their trading business. Then why such erratic numbers?

Here’s a video that didn’t really get publicized but worth watching. The MD talks of the GST impact and that growth will be back on track in the coming quarters:

Standalone results good but when we look at consolidated results , sales are down by 33% and profit is almost three times YOY. How should we see decrease in sales on consolidated basis. Rest all figures looks good in Standalone and Consolidated P&L

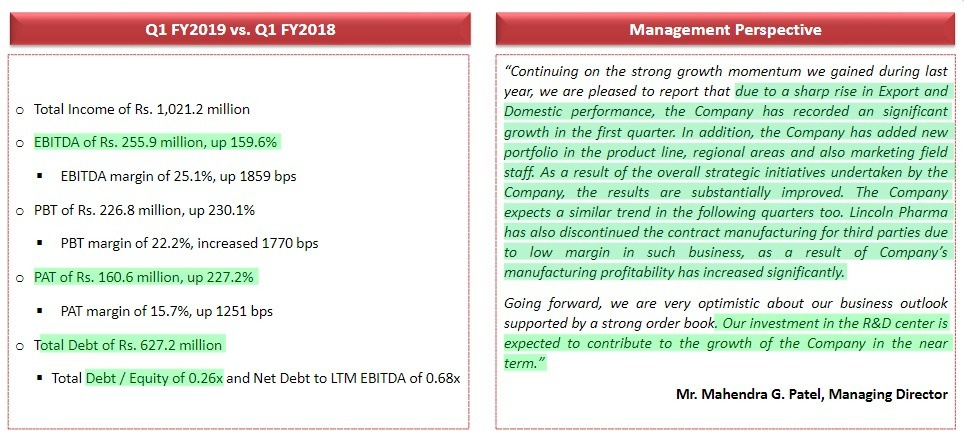

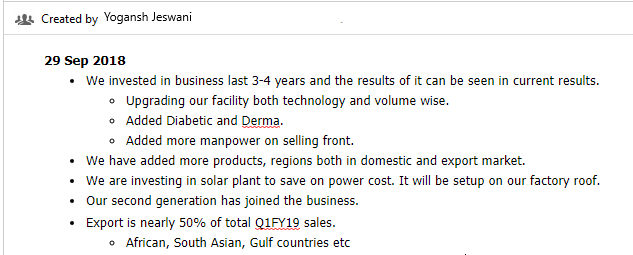

Highlights of Q1FY2019

· Net Revenue is at Rs. 96.63 Crores as compared to Rs. 87.75 Crores in the corresponding period of

the previous year.

· EBITDA growth 185% to Rs. 23.91 Crores as compared to Rs. 8.38 Crores in the corresponding

period of the previous year.

· EBITDA Margins are at 24.74%, Margin growth on account of increasing in Sales as compared to

last year.

· Profit after Tax up 246% to Rs. 15.60 Crores as compared to Rs. 4.50 Crores in the corresponding

period of the previous year.

· PAT Margins are at 16.14%, a growth of 1101 bps compared to last year same period.

· Earnings per share up 246% to Rs. 7.80 as compared to Rs. 2.25 in the corresponding period of the

previous year.

Lincoln has been put under ASM list for two months. Don’t know what to make of it? Seems like it is due to recent surge in volume but then the results were good so why to put it in ASM?

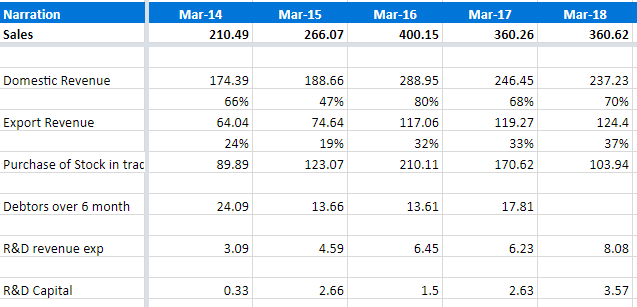

Thanks for sharing the important snippets from the presentation. I went trough last few years of annual report of the company and nos…there are lots of negatives (like volatile nos in past, related party transactions, same products, promoter action etc) however some of the things seem to be improving and positives are there like - improvement in margins and balance sheet over last 3 years. The nos don’t look good at the face of it but if one breaks them down then it seems the company has consciously reduced the trading part of the business substantially which was low margin and an area of concern + R&D expenses have increased and there are hints over product development and expansion. Here is the breakup of nos for last 5 years:

Because of the reduction in trading business, the topline was de-growing but Q1FY19 has been a pretty strong quarter and if this can be maintained in terms of topline and margins, then the valuations are attractive. The concern is that in past the nos have been very un-predictable.

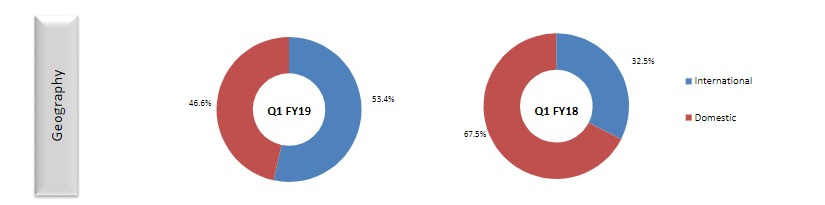

It seems the next generation has joined the business - we should try to see if they are involved and are the reasons for the change in business?

Regards,

Yogansh Jeswani

Disclosure: Tracking

Please Note: These are my personal running notes of the AGM and can possibly have error in listening, writing or interpreting while preparing these, please do your own due-diligence.

I find it a bit odd that receivables shot up so much in 6 months especially considering that Trading volumes were down significantly in Q1 and Q2 FY19 and Especially considering unremarkable growth in the overall sales numbers of H1FY19. While I understand non-trading revenues are growing quite healthily, is it possible that the company has had to give unusually lenient credit terms to its new export markets to market its new and old products? Any thoughts?

Yes receivables have increased a lot, I am also concerned about the same, dont know why there is a sharp increase in it. It is fine if they were lenient or if they have some strategy to push new products by providing loose credit in the beginning but at the same time management has to be prudent with their WC or else may face good amt of liquidity problems and screw the whole credit cycle. Lets make sure that if some one can contact the management then we will ask the reason for such increase in trade receivables.

Regards

Rushikesh

Disc- Invested