Linked portion is bigger than just retail ULIP that is popular. It consists of Linked Pension/Linked Group/Linked Health plans as well.

Non-linked is more than just the insurance part of ULIP plan. It consists of Participating Life/Par Pension/Pure Protection/Endowment plans etc. Wherever there are fixed benefits guranteed, it can be said to be non-linked.

Yes, the float definition means what WB intends.

What I have used is → Float = Shareholder’s investment + Non-linked policyholder’s investments

I could have used them separately but funds flow from shareholders to policyholders in bad times & vice versa. So I thought it would be simpler to combine them.

Return on Float = (Investment Income from Shareholders investment + Investment Income from Policyholders investment)/Float

Excellent analysis, @rupeshtatiya. Economics of an insurance company is understood/measured through its own peculiar ratios/numbers. You have beautifully illustrated what to focus on and how to calculate financially important matrix. I was kind of struggling to come out with simpler framework to understand an insurance company. I think, what you have proposed provides a very good start. Thanks again for your effort.

Excellent work by @rupeshtatiya

I have invested in both ICICI prudential and Hdfc life

According to my favorite professor Ashwath Damodaran one part of valuation is story telling and other part is financial numbers

So on story telling side I want to point out that

If any one want’s to really cover risk of his /her life than definitely he will select non-ulip policy plan and importantly person will select HDFC more than ICICI due to parents track record as money will be given to his family at may be 15 to 25 or more year later (20 years track record of parents is obvious and client don’t know profitability of individual companies)

So HDFC will command more premium if both companies have same financial numbers

Before investing in both companies I have gone through all available videos and interviews of both CEO personally I feel more future clarity of thoughts in Hdfc life CEO (may be I am bias )

hi @rupeshtatiya very nice analysis,

here are my observations relating to analysis that you made

a) Relating to Non linked portion you have derived cost of float by taking preinvestment income in which acturial cost is major component but if you look at the assumptions used in the liability computation there is one assumption that they use relating to interest rates for valuing liability why should not i consider the assumption they have used there as cost of float- assuming that pure protection and non participating policies that are issued are affecting the actual cost of float as derived by you.

b) As regards yield on investment how sustainable will it be the doubt that i had as regards policy holders investments if i go through the schedule level breakup 70-80 % of investment is in debt instruments the fact that i didnt understand is as interest rates in india have been falling the yield on float has been raising mainly on account of mark to market so i feel like going forward spread on floats should reduce as interest rates go up.

i have a opinion that yield on investments in case of non linked portion in case of icici pru will be always higher than peers as they are using a lower interest rate for valuing policy holders liabilities.

Disclosure: Views are biased invested in icici pru

The interest rate assumption used in calculating the actuarial liabilities is the reverse discount rate. e.g. If I have to pay 1L 30 years from now, what should be the sum I need to have today. So you use an interest rate and do reverse discounting to come to present value.

Please check the post from @Anant bhai to understand more.

There are some restrictions put by IRDAI as to where an insurance companies can make investments. With current rules, it is very difficult to have portfolio not skewed towards debt instruments. If these rules change in future, it can create some advantage for people with equity investing skills.

It’s actually reverse! ICICI Pru is assuming that float would grow at a lower rate compared to competition & hence present value of actuarial liability would be more and hence cost of float is higher.

First congratulation in excellent work in the sector. I would request you revert on following points at your convenience.

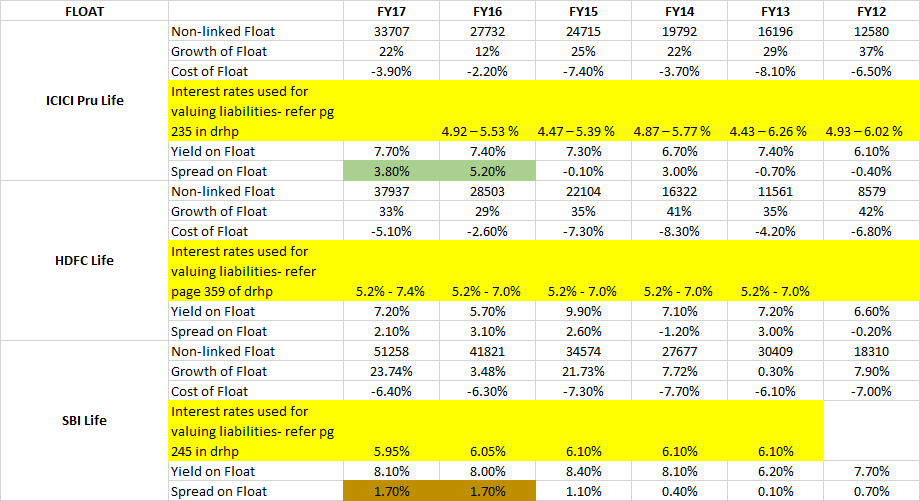

A) In Cell C68 of ICICI Prudential, how you calculate cost of float as -3.9%? (Cell C67/C43)

B) In Cell 44 of ICICI Pru sheet, how you got Return on float of Rs 2599 Cr? Income for Shareholder investment for ICICI Pru is Rs 694 Cr (Cell C27) while Income from policyholder investment is Rs 14977 Cr (Cell C22). That shall make total of Rs 15671 Cr v/s Rs 1905 Cr in Cell C70. Please let me know in case have make some wrong calculation.

For the cost of float, I have used following formula → Cost of Float = Non-linked (Premiums - Commission - Operating Expenses - Misc Expenses - Actuarial Liabilities) / Float

The return on float only considers income from investments for non-linked portion + shareholders investments.

The non-linked investment income is in cell C70 = 1905Cr. The shareholders investment income = 694Cr. Total return on float = 1905 + 694 = 2599Cr.

I actually created a google sheet first on drive & then copied data into Microsoft excel sheet. In this translation, I actually lost all the formulas & without formulas it is very difficult to understand the data. Thanks Dhiraj bhai for bringing this to attention.

I have created shareable link to original google drive link which shows actual cell fomulas →

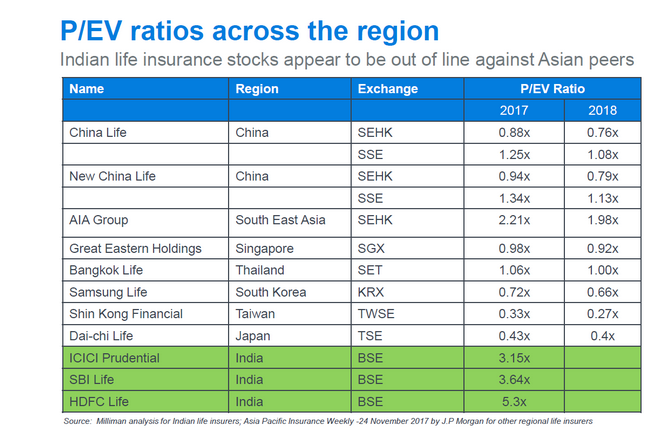

The article compares insurance companies across Asia and argues that Indian life insurers are costly.

Indeed, they are cost if we only look at Embedded value. We also need to look at growth and growth of life insurance companies is measured by Value of New Business Growth. ICICI Pru reported at VNB growth of 71% on h1fy17 in h1fy18. The author need to report VNB growth of other Asian Life insurers to make fair comparison and argument.

Yes it’s costly, but if we look at the history, HDFC Bank traded at around 5.7 PBV in 2002. It’s now trading at 4.88 PBV.But since last 15 years shareholder return is 27.4%

Some companies always remain expensive but still deliver in a strong growth economy like ours. Thanks…

To take the discussion forward, I have added more data to the google spreadsheet.

Link →

PARTICIPATING & NON PARTICIPATING PRODUCTS

We have already established that non-linked portfolio has better spread compared to linked portfolio & also more risk. The non-linked portfolio can be of two types - non-participating (e.g. protection) & participating (e.g. endowment) plans.

Lets look at the premium split across participating vs. non-participating products →

As we already know, non-linked premiums of ICICI Pru is smaller compared to HDFC Life/SBI Life.

SBI Life has highest non-par premiums while HDFC life has highest participating premiums.

Non Par premiums of HDFC Life have grown at highest rate from FY14 compared to other two players.

PARTICIPATING PRODUCTS

For participating products, the policyholder is entitled for any surplus that remains after taking care of expenses + claims + actuarial liabilities. Currently, IRDAI mandates that 90% of the surplus has to be shared with policyholders. This portion can be thought of as ownership model - where people have pooled money to have insurance & any excess is shared back to the pool.

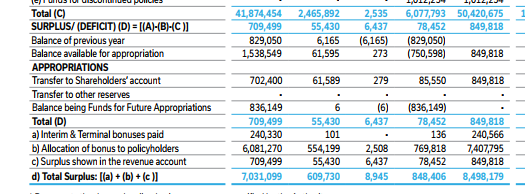

First lets see the accounting treatment of the participating portfolio →

Above image is from SBI Life FY17 AR. The columns correspond to - Individual Life/Individual Pension/Group Pension/Variable Insurance/Total for participating products. Some things to note are -

Row (b) is the bonus announced by the insurer to the policyholders. Corresponding to this amount - there is a transfer to shareholders account which ~10% of total = transfer to shareholders + bonus for policyholders.

Interim & terminal bonuses correspond to maturity or surrender or death or annuity related payments.

The bonus allocation happens only in accounting & actual bonus payments are linked to some events like above - death/surrender/maturity/annuity. For most of the insurers, the payments are not done on demand for non-annuity products.

Logically, this bonus allocation shall be accounted in actuarial liability row line for these products.

With above background, I though the spread of participating products will be very minimal & even lesser than ULIPs. Lets look at the data →

As expected, participating portfolio has lesser spread compared to non-participating portfolio. Non participating products seems to have highest spread.

I was expecting the spread of participating portfolio to be very low (e.g. assuming 3% as total spread, shareholders spread shall come to 0.30%). But that is NOT the case, the spreads are pretty decent.

I think this is because the ratio of sum assured/premium is pretty low compared to non-participating products. e.g. take a look at whole life participating plan from Max Life. Max Whole Life Participating Plan - Review, Benefits & Comparison

With premium of Rs. 21590 for 30 year, the sum assured is only around 10L. With similar premiums, once can get sum assured of ~1Cr in pure protection plans.

So participating plans also have decent profitability for insurers.

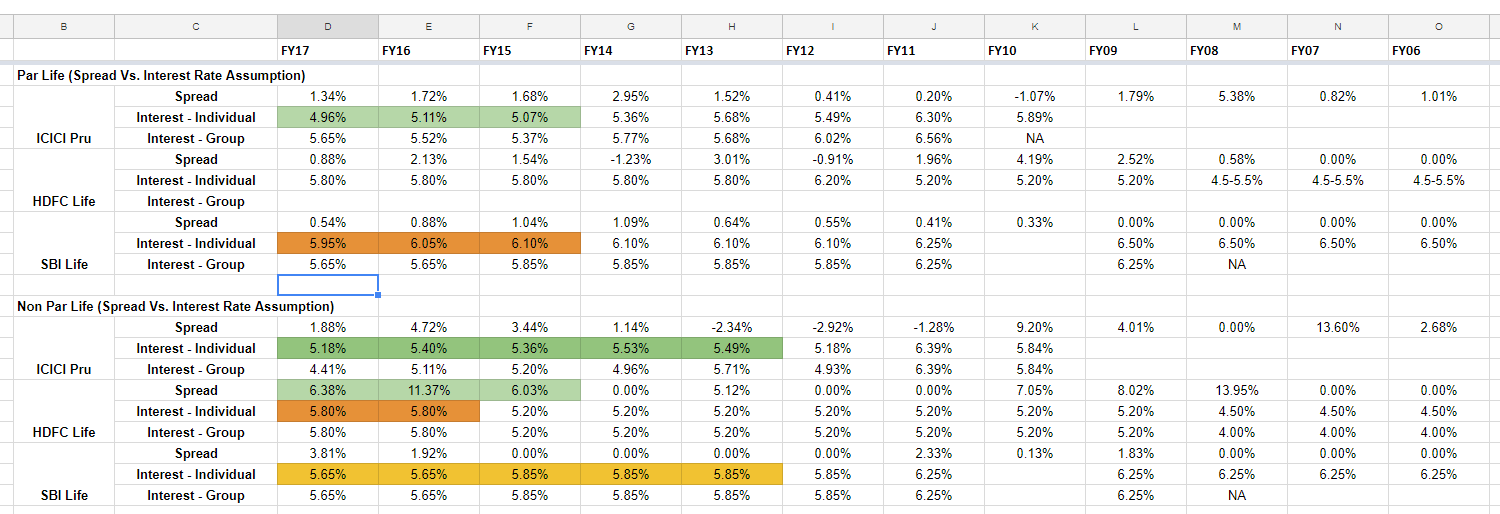

DISCOUNT RATE ASSUMPTIONS

Next I wanted to observe the discount rate assumptions for different insurers across a cycle & try to see if higher spread was a result of aggressive assumptions. Since assumptions are different for different products, I have chosen Par Life & Non-Par Life to check this. These two categories contribute highest to the profitability. Lets look at the data →

One of the important things to note is, highest assumption for discount rate is ~6.5% across last cycle. I would like to take it as a good sign that despite Fixed Deposit rates of 9%+, insurers (correctly) did not assume higher long term discounting rates for policies written in this period. It would be interesting to check if IRDAI has some regulation/guidelines in this matter.

For Par Life portfolio, SBI Life has highest discounting rate assumption and still have lower spread. ICICI Pru has been conservatively using lower & lower discounting rate over last 4-5 years and still has pretty decent spread. HDFC Life’s discount rate assumptions are closer to SBI Life than that of ICICI Pru for Par portfolio.

For Non Par portfolio, HDFC Life has highest discounting assumptions compared to other two. HDFC life increased discount rate (& hence spread) despite other two insurers reducing the rates (getting ready for IPO?). Again ICICI Pru has been most conservative comparatively & still has decent spreads. HDFC Life’s spreads are absolutely amazing (6%+) for last 3 years.

Even though comparatively, discount rates are higher/lower than one another, one needs to think if insurers can achieve absolute discounting rate over a long horizon of 20-30 years.

One of the interesting question to ponder here is - a lot of benefits/claims will be made 10-20 years later. As India becomes a middle income country, interest rates would go down & shall settle to lower average compared to today with more rating upgrades, more business friendly climate etc. Can we foresee what happens to insurers in these cases (huge asset-liability mismatch?)? It would be worthwhile to study insurance Industry of some country (US?) across 40-50 years.

INTEREST RATE FUTURES

One of the interesting thing I noticed in HDFC Life’s DRHP is - interest rate futures. They have ~3500Cr worth of interest rate futures as a part of their hedging policy.

I do not understand interest rate futures & I encourage people with skills & background in this to help analyze this part.

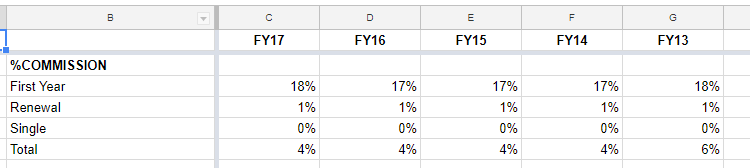

RENEWAL COMMISSION

We all know that higher persistency ratio leads to higher profitability. But I had not fully appreciated the commission outgo on renewal premiums. Look at data below for HDFC Life →

The renewal commission is at 1% compared to 18% for new premiums. In the degrowth years on the basis of new premiums, all that additional commission shall flow into PAT & consequently as dividend.

VNB MARGIN

HDFC Life claims to have highest VNB margins multiple times in their DRHP. So I spent some time thinking about what VNB Margin means. VNB Margin = VNB/ APE.

As we already know that spread is much lower for linked portfolio vs. non-linked portfolio. So for an insurer with dominant linked portfolio, numerator is small & denominator is greater. So basically, higher VNB margin means higher proportion of non-linked products (or high margin products). I think VNB margin shall not be used in isolation & growth in various products segments is equally important.

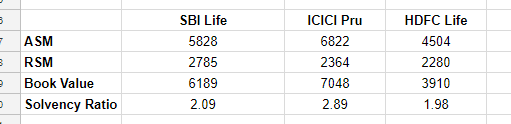

BOOK VALUE

In one of the discussion with VP seniors, it was said that why book value is not used to value insurance companies similar to banks. I have given it some thought →

For banks to grow, they need to raise capital from time to time & hence book value becomes pretty important factor e.g. RBI allows debt to equity ratio of upto 16 for banks. For insurance companies, their is no need to raise capital if solvency ratio is satisfied.

Also for banks, profit generated can be used to fund new growth. But in case of insurance companies, investment yield is at 8% for last few years. It hardly makes sense to reinvest the profits at such an yield on the behalf of shareholders. It totally makes sense to return that capital to shareholders (unless investment yields are 12%+) and hence book value will grow slowly.

Further book value does not capture the earnings power of the insurers.

In case of most insurers, book value = solvency margin (to satisfy solvency ratio of 1.5) + some additional buffer for future growth. Look at data below →

ASM = Actual Solvency Margin. RSM = Required Solvency Margin. Solvency Ratio = ASM/RSM.

I am inclined to say that P/E is not a bad ratio to value insurance business as they represent real earning/earning power if actuarial liability assumptions are acceptable. (e.g. 60-70% of profits flow out as dividend)

TODO

Study insurance industry of some country which went from low income to middle income to high income & particularly interest rate movements.

Split of business across group vs. individual businesses & understand more. (HDFC/SBI Life have much bigger group business compared to ICICI Pru).

Disc - I am invested in ICICI Pru Life & my stake has gone up in last 30 days. My views are biased towards ICICI Pru due to my investment. It forms 5%+ of my portfolio. This is not a buy/sell recommendation. I am not a SEBI registered analyst. Please do your own due diligence before investing.

If your view is that interest rates are going up, “Short” Interest rate futures (you profit because when interest rates go up, Bond prices come down).

If your view is that interest rates are going down, “Buy” Interest rate futures (you profit because when interest rates go down, Bond prices go up).

Thanks

Ashit