@Madhurkotharay, thanks a lot for such a comprehensive report of your visit.

1 Like

As far as the stock market is concerned, the market has a mind of its own. Mr Madhur has indicated a fair value of 220 , but a market that values a loss making and fv2 scrip like Sequent so richly, while valuing a pofit making , high growth and fv10 scrip at just 130, defies logic, to say the least. We have no option but to trust the wisdom of the market and wait patiently for it to realize and correct such anomalies.

2 Likes

@nkgambhir. Sir whatever the results be of this script but your enthusiasm is commendable. One of the reasons I am still holding is your constant update. Nice.

2 Likes

The above are the pics of the unit 4 startup .

1 Like

Awesome news …let us see how this story unfolds now on…

The market is giving the promoter of sequent arun kumar some benefit of doubt. Or else your analysis is correct and it could potentially be quoting at Rs 50. He has a track record with strides including the one time dividend from mylan which was distributed to shareholders. Hence it is still holding 100 levels.

Thanks, Kothary ji for your efforts in bringing the real story of the company on this board and putting to rest all guesswork. No more information is now needed to build conviction in Lasa.

Thank you very much for your honest, detailed and informative report. Your report really gives strength to investors like me to stay put in this counter for better prospects. May God Bless you for your honesty and openness in writing facts without any bias. Eagerly awaiting the Q2 numbers. Fingers crossed. Your golden fingers which inagurated the Plant IV will bring us wealth and happiness. Long live Dr Omkar - your hard work, simplicity, innovative ideas, focused approach and inspiring leadership will take Lasa to new heights and bring happiness in the lives of investors. - A retired person.

3 Likes

Nagaraj sir,

I hope you do not go overboard with your Lasa investment. If you are a retired person, your risk taking ability is probably less than mine.

As I have clearly mentioned, there are a few things I still have no answers to. For example, I do not understand their capex numbers (given by earlier Omkar Specialty) for the plant(s).

I hope they show similar topline in Q2 as they did in Q1 and similar EBIDTA (24-25%), as they have claimed. I have no clue what PAT they will have because apparently, interest costs should be lower in Q2.

Also, I have a technical query to CAs in this group: in Q1, they showed some deferred tax reducing PAT. Is the quantum of deferred tax somewhat discretionary or do they have to follow exact guidelines? If the latter is true, the deferred tax should not change much from Q1.

All in all, Nagaraj sir, please do not treat Lasa as a buy and forget scrip. Do keep a regular check on its numbers and other developments.

6 Likes

I am also puzzled by the “deferred tax”. Surely it is not mandatory, as most companies do not make this provision. If they have done it voluntarily, then it reduces the profits in that quarter artificially, and serves to decrease the tax outgo in the final quarter. Wha is the logic behind this and do any guidelines exist for this ? I also hope someone in this board will have the answers.

Just a wild guess, Does this have to do anything with the cash flow management ?

For example, for a given quarter, if a company has more cash than the current working captial requirements, but anticipates higher capital needs in the near future, maybe it is simply preponing the tax payment ? This would allow is pay less tax next quarter & at the same time act as a buffer for unforseen working capital requirements ?

So is it perhaps simply a matter a managing cash ?

1 Like

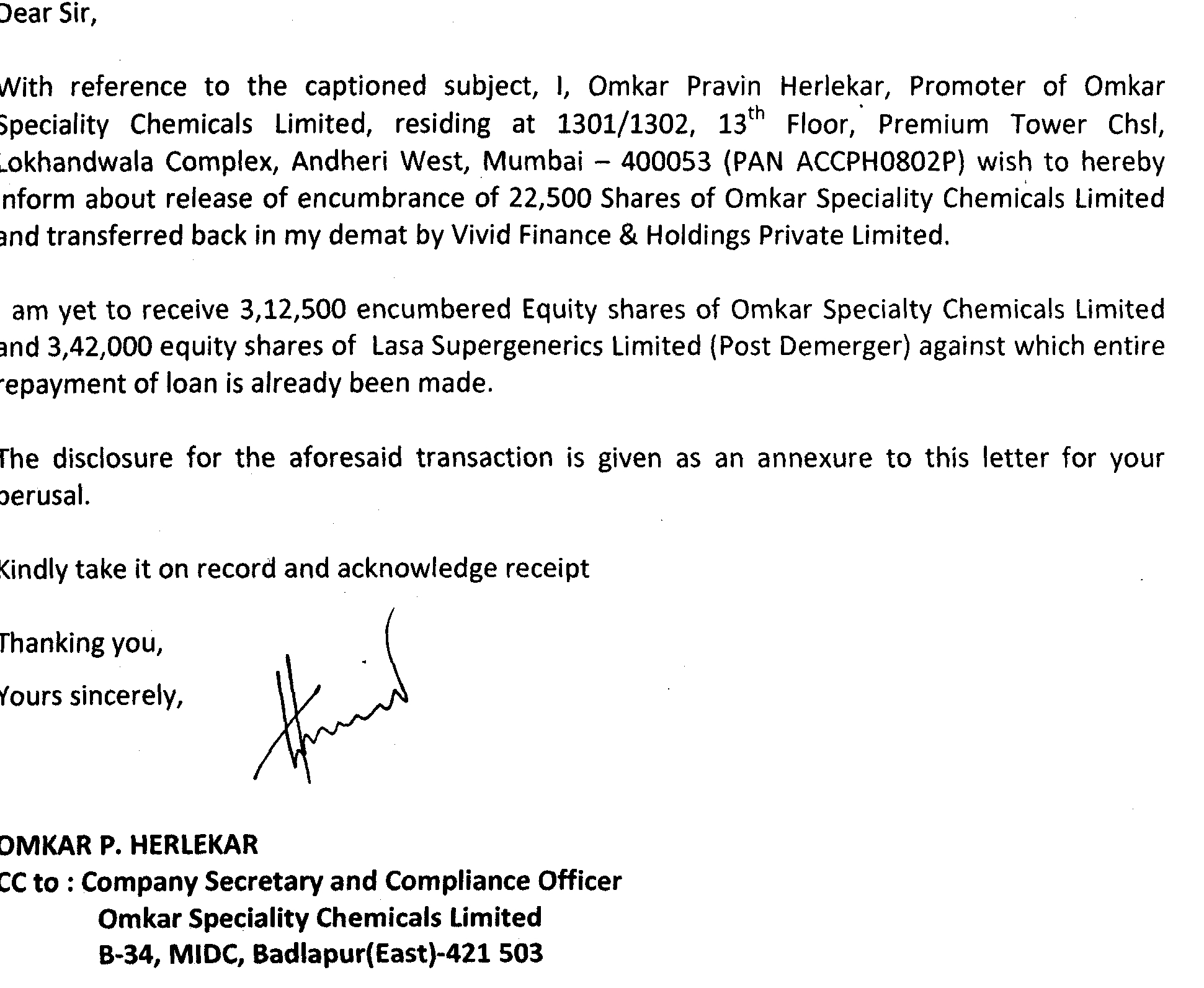

A way of managing cash or perhaps to smoothen out the fluctuations in earnings over the four quarters. Recently Omkar Herlekar has given a declaration , as a promoter of Omkar speciality chemicals, about pledged shares of OSCL as well as Lasa.

This declaration is strange, to say the least. What is the meaning of the statement, that he is yet to receive 342000 pledged shares of LASA, for which the loan has been repaid ? And if the paymnt has been made for depledging of LASA shares, then why was this disclosure not made on the page of LASA ?

The taxable income as per Income tax act is different than the one calculated as per P & L account drawn in accordance with the Companies Act. This is mainly on account of the different treatment of certain expenses and different depreciation rates provided for under the income tax act. This tax liability is shown as Income Tax Provision and to match with the one due as per P & L account the difference is recognised as Deferred Tax Liability or Deferred Tax Assets.

1 Like

Deferred tax is tax effect of timing difference. Difference between the tax expense (calculated on accrued basis) and current tax liability to be paid for particular year is called differed tax (assets/ liability) For eg. the company has purchased some asset of Rs 1,00,000/- on 30 September. The rate of depreciation as per Income tax is 40% and as per company law is 30%. The depreciation amount as per income tax works out to Rs 40,000 (Full depreciation since asset put to use for more then 180 days) and as per company law is 14960/- (Base on no of days). In this case tax liability for current year will be less due to higher tax provision so company will make additional tax provision in form of deferred tax liability. the position is reversed in case of defered tax asset i.e tax as per income tax is more. Regards

1 Like

Why would company prepone tax payment…and lose interest income on cash on hand.

They are not preponing tax payment. In my view, they are just making a provision for it in advance, so as to avoid taking the hit in a later quarter.

Dear Kotharay ji, Many thanks for your advice. As advised, I will keep a regular check on the numbers and other developments. With warm regards

Hester and NG fine chem .Both are doing really great. LAsa with consistant performance can do well over a two year period.

Dis:holding 8 percent of protfolio