http://www.bseindia.com/xml-data/corpfiling/AttachHis/a7c61f46-e8f3-4901-a7eb-f577d6db557e.pdf

Thank you, Sanmam. Sorry - I don’t know why I read Unni’s comment as Unit 5 to start on or before Dec 14. I went and looked at Corp Announcement but found nothing regarding Unit 5 start date. My brain is thinking of only Unit 5 when it comes to Lasa.

Finally !!!, light at the end of tunnel. This will put to an end to the question on Unit V starting up.

http://www.bseindia.com/xml-data/corpfiling/AttachLive/5161cec8-f67d-47dd-80ad-0d8ffb738d7f.pdf

6 Likes

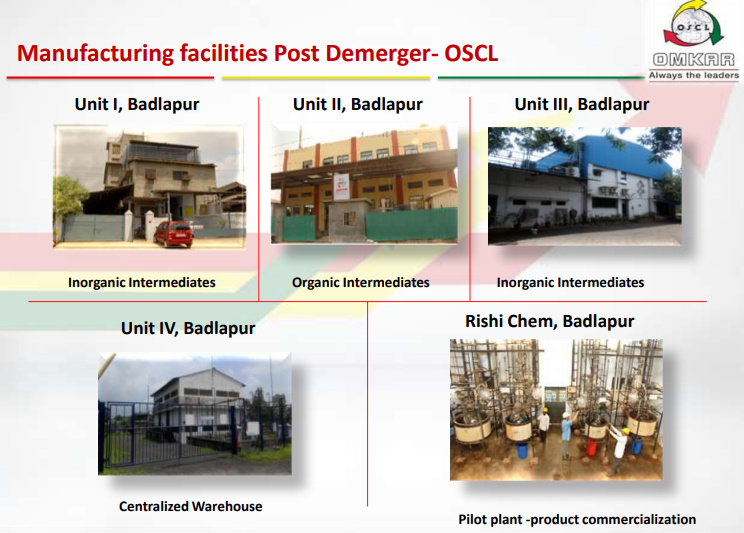

Any idea why does it say unit lV?

Unit V was the original designation when it was the unified entity with OSCL. After Lasa demerged, it is now designated as Unit IV. That is my understanding.

I have added a couple of slides for better clarity

5 Likes

Thanks. You are right.

Anyone has any update on the stock moving out of T2T category

I think that will happen in january or february only. Shareholding pattern gets reviewed only when quarterly shareholding pattern are submitted.

1 Like

Hi

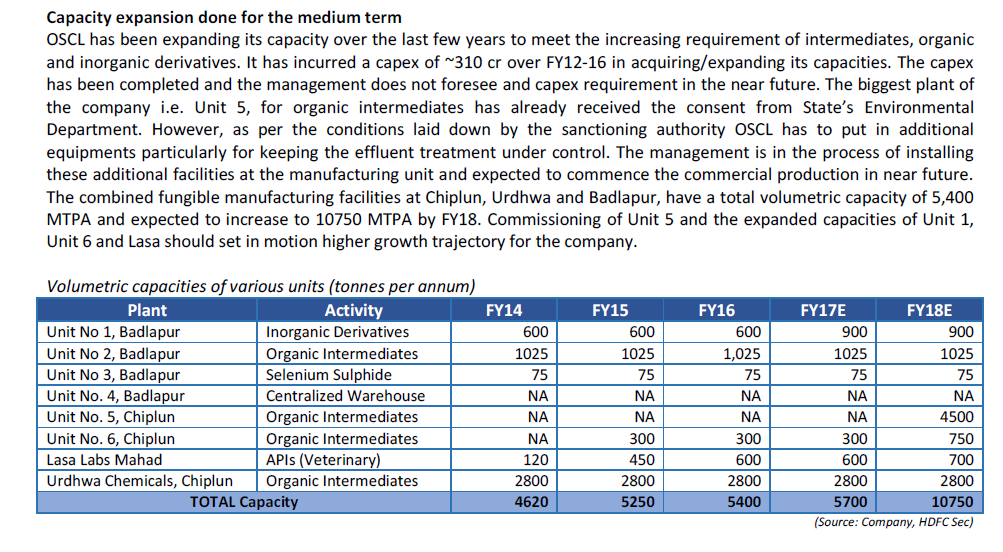

What is the revenue potential of this unit 4 capacity alone? Does this mean the incremental capex requirements are going to lessen way forward?

Thanks

Hi @srnarayan, This partially answers your question ( The source is an HDFC sec research report for the combined entity. The plant designation should be read accordingly).

The revenue potential is discussed in the concall transcripts earlier in OSCL thread (am not able to find it at this point). There is no further capex requirement immediately as per the disclosures. Opex will be a different matter though.

Hi @adityajp

Many thanks for sharing the data…

Some basic calculations going through OSCL Annual Report

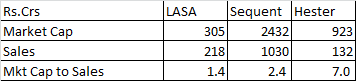

So conservatively assuming if OSCL guys make roughly about Rs.24lakh per ton in revenue terms; then Unit V of OSCL (now Unit IV for LASA) assuming it to be at 4500T alone translates to a rough ~750crs revenue potential which in addition to comparison of peers below translates into one of the cheapest company in this business on market cap to sales alone…

What is it that i am missing or markets are discounting?

Regards

1 Like

You have figured out the numbers right. Mr Market may have other considerations which puts Lasa on “Wait and Watch” mode, based on the past of the combined entity (The past may be past, and we should be looking at the future potential - Yes true - But…)

The main concerns are highlighted here:

Falling institutional holding

Institutional shareholding in the company has come down over the last couple of years from ~15% in Q1FY16 to 4.4% in Q3FY17. Institutional investors are long term investors and provide stability to the stock prices.

Decreasing share of export revenues

Exports accounted for 28% of the revenues in FY13 which has halved to 14% in FY16. Revenues from exports fell 14% in FY16. In 9MFY17 it has further declined to 12%. Slowdown in exports is likely to impact topline growth.

Delays in commissioning plant

Delay in commissioning of its Unit V plant is taking a toll on OSCL’s finances as the company had taken loans and already incurred capex for the same. Further delays would continue to escalate its costs.

Foreign exchange fluctuations

OSCL is a net forex earner and most of its exports are done in dollars. Recent strength of the rupee against the dollar could hurt its profitability going forward.

Share sale / Pledging by promoters

Promoters have sold their shares in the open market to repay loans taken by them. Their holding has declined significantly making the company vulnerable and keeping share price under check.

Raw material price fluctuations:

OSCL faces the risk of fluctuations in its raw materials (~70% of sales) which it may not be able to pass over in sluggish/competitive times.

Regulatory risks

The plants of the company run regulatory risks of inspections and environment clearances. Although the plants are fungible its operations are likely to be impacted in the short term if a ban were to be imposed on any of its plants.

Debt equity ratio remains high

OSCL has funded its capacity expansion over FY12-FY16 largely through raising debt. As a result its debt-equity ratio has remained on the higher side.

Long story short, Lasa is a story waiting to be unfolded. One need patience here. Please also read the transcript of Mr Omkar Herlekar in one of my earlier posts in this thread, to get an idea of their business and what the promoter is doing to reduce debt.

5 Likes

The 5th unit commissioning atleast clears one of the key risks.

The other ones to watch out for is the promoter holding. Has anyone in the group visited their plants?

Hester and lasa are not comparable. Hester is into vaccinations in a big way . For sequent a part of them is into animal antibiotics. But also into human api. Apart from that the pledge is a big dampener

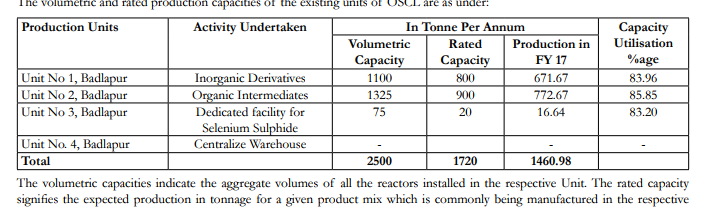

Here again, there is lack of clarity as the capacities indicated by the company of Unit IV as per its intimation dated 22.11.2017 are not clear. http://www.bseindia.com/xml-data/corpfiling/AttachHis/5161cec8-f67d-47dd-80ad-0d8ffb738d7f.pdf.

The various items listed in the above filing totals over 1300 MT and in addition, the intimation informs of the existence of some additional capacity related to the backward integration of few new launches. If one goes by the practice followed by the company these must be Volumetric Capacity and one cannot be sure of the quantum of rated capacities.

Any industry expert on this board may help us by sharing about the potential of these products.

@nkgambhir - From what I can see, this company doesn’t have a single product/commodity and so speaking of capacities blankly in metric tonnes makes no sense first and foremost. They seem to have multiple organic and inorganic intermediates (about 30 of them in all). Without understanding what intermediates will be manufactured in this new unit, what the demand for them are and what’s the pricing trajectory and competition and so on, speaking in terms of 4500 tonnes and doing some extrapolation based on current revenues without knowing where the contribution is from or what the pricing for those were, is extremely dense at best.

I see most of the valuation here is based on relative basis comparing it with Sequent Scientific. One look at Sequent makes me wonder why it is so overvalued. The market has been correcting on that scrip for the last two years - From Rs.250 levels to the current Rs.99 levels and still it seems so extremely richly valued IMHO. Its ratios are abysmal and it seems to lack pricing power. So using Sequent as a benchmark itself looks very flawed.

6 Likes

If I remember correctly, Omkar Herelekar had given a revenue projection of Rs 800 cr of Lasa including unit-5 with an Ebitda margin of 25%.

Yesterday Mr madhur kotharay and nitin rao ji inaugurated unit 4… Production started

Batch charged with their hands

As per info recd. Unit 4 has a prodn capacity of 3400 T while all the other units have a combined capacit of 4300 T. As for the product mix, the profit margins etc , that depends on the management of the company. What we know is that the company has the capacity to produce 7700 T of its products every year.

2 Likes

I recently met the sequent ceo and raised the zame concerns about valuation at 100. He assured me thr worst is over and his performance is better than the share price. My concerns remain and this stock may be stuck in a tight range for a long while. The swap ratio for solara shares is not favourable and animal biz is not doing well. If i had to choose a pure play animal health id rather look at lasa or hester, or re invest in sequent at a much later date post demerger and if valuation comes down dramatically

How did you know, Gambhir Sir?  In this market, almost nothing can be kept secret.

In this market, almost nothing can be kept secret.

Actually, I did not go for inauguration. I went to find out the ground level picture. As it happened, Dr Omkar was not there. And only two of us investors were there. So they asked us to inaugurate.

I am still rattled by the 12 hour car drive to and fro Mumbai. So will write in brief. But in short, a few observations:

- Lot of hunger for growth.

- A committed but simple team, which is sold on to the growth dream.

- Smart, Indian jugaad to get things done.

- Costs kept low; no expenses on unnecessary things. No painting on reactors and no board on the factory. Even the plant walls were barely painted but lot of machines were put in that place. Money was spent on important things. Non-essential staff is on contract basis. So no union issues.

- Found large tracts of adjacent land bought for expansion (probably, some companies were bought). In my view, they can go 1000 crore in this much of land. Needs equipment though.

- Working 3 shifts. Sweating the assets very heavily. While they bought a new expensive SFD (Spin Flash Dryer), they still used the old tray dryers alongside to squeeze some extra output.

- Saw a tearing hurry to get things done with respect to production. Nitin uses the word ‘relentless’ for the execution.

- They make their reactors because companies like GMM and Swiss Glascoats typically take 6 months after ordering. Their in-house production guys just assemble the reactor and get it going in 3 months. At one point, I pointed to an incomplete structure and asked if it will be ready in 2-3 months. The local guy said in Marathi, “come on Wednesday. It will be ready by then”

- I am convinced the new plant operations will increase gross margins and EBIDTA. Along with new production, they are going for backward integration. I saw 3 of their Chiplun plants. One of them (Unit II) makes Halquinol. I saw they had input as 2,4:DCP (2,4-Dichlorophenol), which they bought from Atul. The reactor we inaugurated (they poured 3 bags with labels, catalyst 1, catalyst 2, and raw material inside the reactor, after we broke coconuts and put flowers on the reactor) was actually to make 2,4:DCP. The Halquinol plant head told me proudly that he makes 2,500 kg of Halquinol a day. I saw the bags and drums of them and my estimate was about the same. As per my calculation, that would be about Rs 90 crores of production a year. In the plant II yard, I saw the drums of 2,4-DCP, with labels from Atul. They have bought a JCB to level the grounds but I learned that they were going to use the same JCB to empty out the reactor from plant IV and carry the drum to plant II (which makes Halquinol, which is about 500 meters away from Plant IV), saving on other transport costs. Essentially, with this new reactor, they will have an increase in gross margins as they will save on raw material costs (basically, they will make Atul’s margin). So do not count this reactor for increase in turnover but increase in profitability.

In short, treat this like a complete startup. No fancy presentations, sleek brochures, lovely photographs. No MIS. I doubt how they could give expenses for operative capex with the kind of tearing hurry (“get things done quickly”): if something breaks down, just replace the parts and get things running again in 3 hours, etc.

They clearly have cash crunch. If someone were to hand them 100 crores, I think they would just put all those growth related infra, reactors, storage, QC centre, at one go and ride the growth. Currently, they looked like doing capex using the cash that the business generates. Get some payments, build another reactor, etc. Complete bootstrap operation.

My personal belief, post-visit:

A) They will hit 500 crore in turnover in 3 years, that they have been claiming.

B) There will be a lot of confusing developments along the way.

For my visit, I was expecting to understand about the capacity of various reactors, the plant setups, the pollution issues, the expansion possibilities, like a typical investor would want to.

I came away with a realisation that at this stage of operations, it is impossible to have all those sleek numbers and presentations.

I came out with a firm decision to get out of their way and let them run the way they are planning. I will just keep an eye on the business turnover, EBIDTA, debt and profit numbers. As long as they deliver on the business numbers, I am going to stay put.

Part of my bias comes from my experience when I had started my own business in 1992. We used to completely bootstrap, saving on unnecessary costs and spending a lot on essentials and we had no clue about the breakup of marketing costs versus admin costs, etc. We were growing at 20% a year, facing a cash crunch all the time, and I did not know why we were suffering for cash, with such a growth (it was working capital and capex management, I learned later, being a technocrat). I saw exactly the same thing happening in Lasa, albeit on a larger scale and in a different industry. So I could fully understand when some of their people said they did not know which molecule gave them higher margins, adjusted for production time, labour and capacity.

I also get a the strong feeling that this company’s strength is Dr Omkar, with all the warts everyone has noticed. It should have been obvious to me from the beginning but somehow my scepticism overlooked that. Short of faking numbers, you cannot take a company from 14 crore to 200 crore turnover in 5 years, in a mature field (all molecules and their production technologies are 20-50 years old), without something special.

My judgement is Dr Omkar spends 10-12 hours a day in his lab, figuring out how to make the molecule cheaper and faster using catalytic chemistry. This R&D gives him an edge with much cheaper cost of production. He is able to sell the molecule slightly cheaper than the competitors, because of his higher margins and so is able to capture the market fast. I should have realised that you cannot grab 60% market share of any molecule in 1-2 years without such a strength.

The most important thing, which I gathered when I met Dr Omkar, and this subsequent visit when he was not present (so his people opened out more, perhaps), is he is a master in catalytic chemistry.

People wrongly slot Lasa as an animal API company. Catalytic chemistry can be applied to many chemical molecules from diverse fields. Dr Omkar can take a molecule and figure out, after some R&D, how to make it cheaper and faster using better catalytic process. While the molecule is out of patent (and in India, product patents are invalid), the process patents are valid in India and if he finds a new process to make the molecule, he gets a patent for it and others cannot copy that without breaking the Indian law. He can thrive on that and so Lasa can go into any field, as long as the market is able to offer good margins to him. I have heard he is one of the very few companies in India that is exporting API to China. This is purely because of the cost advantage he gets.

All in all, two risks in Lasa:

- Keyman risk. No one will buy this company, for example, if he cannot buy Dr Omkar.

- Equity Dilution: no idea if the cash crunch will force them to dilute

My first shares of Lasa (bought before demerger) went into LTCG on 24th Nov. Just before I bought them, Girish Deshpande had warned me to be prepared for a roller-coaster ride. I remembered those words as our car passed Imagica (Fame Adlabs’ theme park) en route the plants yesterday. I think this ride will be far more scary than anything Imagica offers, and I believe, far more rewarding.

Disclaimer: 30% of my PF is in Lasa. I intend to stay in it till they deliver on growth and EBIDTA numbers.

Disclaimer 2: I still do not have a lot of answers and some things are confusing, for sure. My personal valuation matrix is 250 cr sales and 25% EBIDTA for FY18. So at 10x EV/EBIDTA, EV of 600 cr. Minus debt of 60 cr, gives me market cap of 540 cr. So fair value for me is about Rs 220. You do your own calculations.

42 Likes