The stock is down 20% today and could not find any specific news for the sudden steep fall. Still looks a quality business for the future with improving product portfolio and brand spending. Hope its not any case of fraud that the market already got wind of before retail investers.

Look at its long checkered history!

How this stock rose from 2 to 230 in 1 year, fell to 85 in next one year, rose to 180 again in 2011 to fall back relentlessly to 30 for apparently no reason. It was rising gradually since then and got back to 140s. Today’s fall reminds me of the fall in 2011 (for no reason). This is an operator den. Stay away.

5 Likes

How long can the operators continue if the business keeps performing. Impressed by their procurememt model, product portfolio and branding (recent initiatives like signing Akshay Kumar and positioning the brand as more health concious)

The big risk is the significant amount of debt and the pledging due to the capital intensive nature of business. Contineous operator manipulation could make the banks release the pleadged shares.

I am not talking about the company, but the stock. ;-). Well, we keep saying that stock performance follows company’s performance. But here, if a stock falls from 180 to 30 for no reason (happened in 2011)…what wd it mean? At that time, company commented that they cannot control stock price. Fair enough. But no stock falls like that if the game is fair.

One of my friends who deals in dairy business doesnt speak highly of kwality promoters.

1 Like

I don’t see any fundamental red flags with this business - looks like market jitters along with some operator angle has driven this stock down (especially given the history of the stock). The company’s procurement strenghts are evident from its involvement with large B2C players like Amul, which itself is a giant in procurement.

Additionally, I believe that the current milk market in the B2C segment is ripe for disruption. Amul (and even Mother Dairy for that matter), however large is fundamentally a co-operative run for the benefit of farmers, in such it doesn’t aim to produce profits but rather maximise the farmers well being. I don’t believe that this leads to good decisions in the long run, especially due to underinvestment and not enough aggressiveness. Kwality on the other hand has expanded aggressively, evident from its stretched balance sheet and large branding expenditures. Kwality’s low free cash flow is a result of its massive growth - truly, one cannot expect a manufacturing business to expand at such high rates without capital expenditure. Regardless of this massive investment, Kwality’s return ratio’s have remained high, signalling that the business is great for further investment.

In terms of leverage, the high D/E ratio does seem like a key risk, but I believe that Kwality’s business model is sound, and with increasing share of retail sales, becomes ever less risker in terms of earnings volatility, mitigating some of this risk. As an equity holder, I am not opposed to leveraging since the co. has a ~16.3% pre-tax RoCE (EBIT/(D+E)), which is higher than its cost of debt.

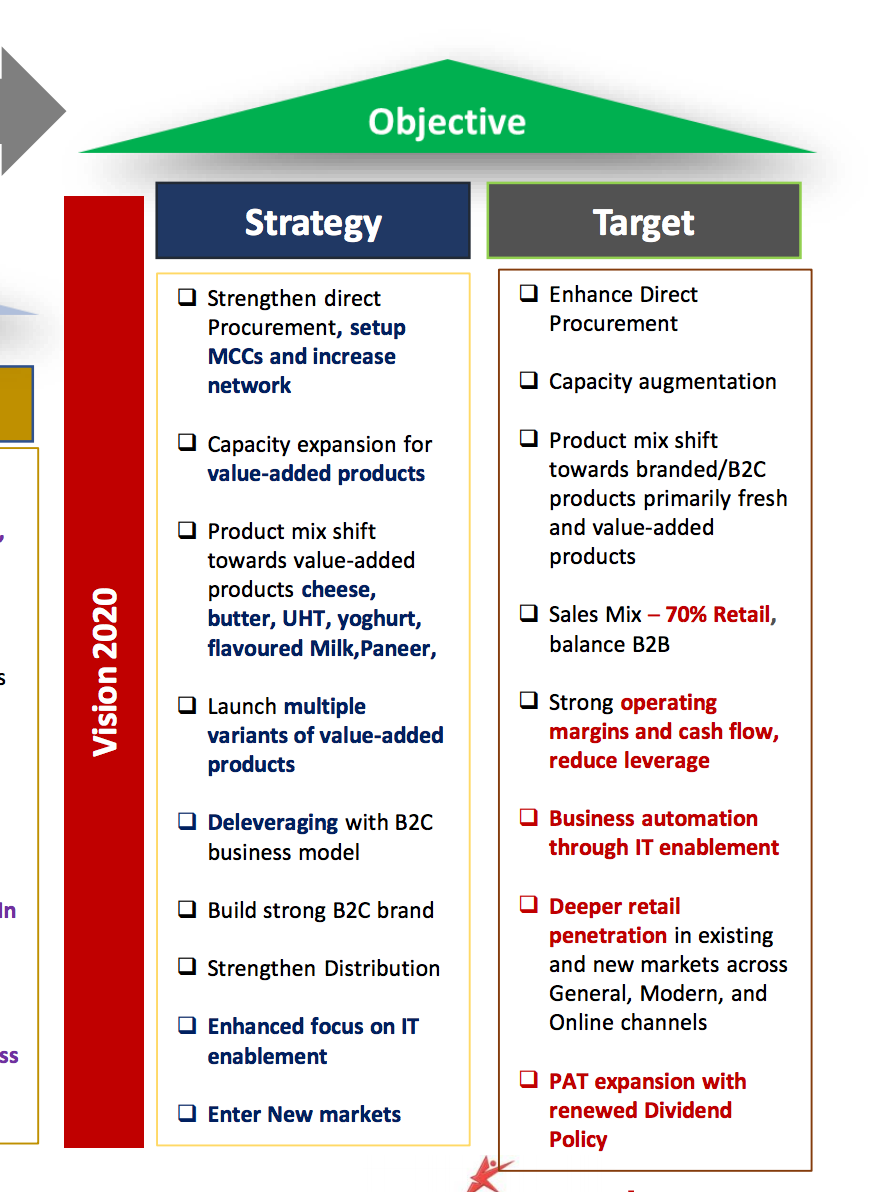

A look at the recent investor presentation also gives a glimpse of improving corporate governance standards at the co. (focus on deleveraging, improving dividend payout etc.) along with a focus on high margin value added goods.

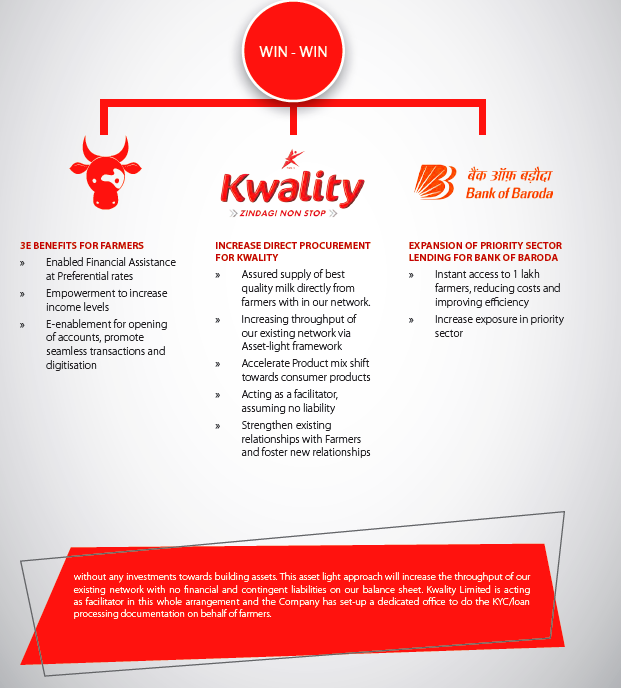

Additionally, I think the BoBaroda tie up for Rs. 4,000 cr in loans is fantastic - not only does it strengthen Kwality’s relationship with existing farmers (by providing them loans at 8.6% vis-a-vis local moneylenders of over 30%), but it also allows Kwality a larger producer base without incremental fixed cost of opening greenfield procurement centers. At the same time, it allows BoB to mobilze its large low cost CASA deposits in additional to generating priority sector lending for the bank.

Views Invited.

Disc. Not invested yet, but might initiate a position soon, given reasonable valuations (~9x EV/EBITDA)

Lot of pledging and selling by relatives and employees. Pashupati Dairies Pvt Ltd looks to have pledged all its holdings (over 5%). Something doesn’t seem right.

3 Likes

Great link - thanks! The pledging disclosures definitely need to be addressed by the management. As far as the selling goes, the entity Sonika Gupta has been the major seller of Kwality stock in recent times, although given her cost basis of only 48.75 per share (through warrants), makes sense prima-facie. Similarly, Pashupathi Dairy did sell a major chunk in April, but has bought back some (~1/5th of the sold ones)shares recently.

I am however, tempted by these valuations for a high growth business, so I might still bite, but other boarders should build their own convictions given the shady transactions (as well as in the past)

1 Like

if you see the insider data …Sidhant gupta and Pashupati Dairies have increased their stake aggressively in the open market…Sidhant gupta now holds 5.5% . Am not sure about pashupati diaries but it looks like nearly 10%.Correct me if I am wrong in looking at that. This seems to be interesting …

1 Like

What are kwality’s future growth projections?

True that the bootomline of these businesses have expanded due to operating leverage but the sector is yet to see rapid growth. Topline growth is very modest actually.

Topline growth for last 3 year look like this:

Hatsun-19%

Parag - 16.8%

Kwality- 10.2%

Heritage-9.7%

Britannia-10.1%

Could this be due to the 1500 Cr equity dilution that is mentioned under special business approved by the board? The AR I think was published on 4th Sep, so could be a reaction to this.

Management projects a 25% CAGR growth in bottom line till 2020 owing to expanded margins from value added products. If you exclude the basically stagnant B2B business of Kwality, you’ll see the B2C part growing much faster than overall top line would suggest, and because it has a higher OPM % PAT growth can be much higher.

Just in terms of the B2C goes, I think growth is a lot more visible for Kwality vis-a-vis say a Brittania because Kwality has only scratched the surface with number of distributors, and thus can potentially continue to see predictable growth by adding distributors, provided their product stands on their own. As far as the product category goes, I am extremely bullish on VAPs as they are growing much faster than the overall milk market, and I can only see this rising.

Also, as you mentioned Kwality’s comps, look at the type of multiple those companies are commanding, to see what type of stock returns are possible if the B2C transformation continues playing out like this.

kwality is cheap compared to peers , no doubt. But i think the reason behind is equity dilution and Pledging of 44% shares by promoter. Effectively promoter holding in 35 %

This i cannot believe is trading this cheap considering all the great things happening behind the scene in the company .

You should read the annual report , its a amazing read.

some of concerns people are sharing here like dilution ? Some 2 lacs shares given as options to employ is that the thing ? this is like drop in the ocean .

Pledging is not a worry … its the growing business and lots of fruits to Capex now will start coming. Plus ROCE is around 15-20% average then whats the harm in taking debt.

Effectively promoter holding is 35% is a very wrong statement, pledging doesn’t mean you lost ownership right away.

1 Like

when you have 44% of promoter holding which is pledged , you are going to see that affecting the price of a stock in any market. A long term debt of 1500 cr is also on the books.Operating Capital is increasing at the same time yoy. OPM is just like a commodity business. We have to see how they increase their OPM with high margin products which Kwality does not have many.

If its cheap because 44% is pledged then i believe this is a value buy,

Why do you think they will run into bankruptcy event ?

Why do you think these are pledged forever and they will never repay their loans ?

I believe if things continue to play out as it is the debt will go away eventually , pledging will go away eventually.

These are not very high risk business , People not going to stop consuming milk . With increase in per capita income and urbanization more and more people going to consume branded milk.

Do you know today the organized sector just has the market share of 22% ? why company would not grow or bankrupt, what are chances for pledging to get revoked in this market scenario ? Even demonetization had no effect. On recession as well people don’t stop buying milk (they might stop buying Maruti )

This for me is the most impressive trick that played by the company. I don’t know if others have done the same or not but its a brilliant idea.

debt repayment and depleging possible? Answer is Yes. But You are missing the most important point OPM. If OPM does not increase through good product Mix , it will be hard for the company to give good results. Interest costs will be a big drag. Traditional Milk businesses does not have good margin as we all know. The Key going forward is the new products with high margins , the company can introduce and capitalize.If you check the product portfolio of its peers like Hatsun and Parag , you ll see the difference. Because of the value added products with high margins , these stocks are valued as FMCG stocks with TTM pe as high as 60-80 apart from their balance sheet. I order to command a good PE for Kwality or in order to improve , they have to walk the talk .

I am not discrediting them ,They can be a turn around as they have a niche B2C business with a very good milk collection network and the BOB scheme tells more about its relationship with cow owners, It will be interesting to see how it works for them…

@Dhruva1705 The mgmt discussed in the last con call and it’s also mentioned in their latest AR that they have taken an enabling resolution to raise 1500 Cr via a QIP. Although timing is not decided and mgmt mentioned in the coral that they will wait for favourable valuations before going for this QIP, when they do go for it, imagine the kind of dilution that will happen. ESOP’s are fine to an extent, but other than ESOP’s they have also given Equity to HT and TOI last year, as well as one of the directors has exercised warrants. So all in all about 5-6% dilution last year but more in the offing via this massive QIP.

The mgmt claims some of the proceeds will go towards optimising their capital structure, i.e. retire high cost debt and replace with equity, which they believe will ‘unlock’ value for the shareholders in the long run, by reducing interest cost…

However, if you track their performance over last 3 years till last quarter, OPM is indeed increasing, and their B2C business is growing rapidly. it is now 42% as of Q1FY18 compared to literally 0 many years back when they started as a pure B2B business and built their scale. Mgmt has repeatedly said that top line will probably remain stable or grow marginally, but bottom line will grow due to higher margin B2C products. They are targeting 9% EBITDA in 2020 compared to 6.9 now. This was 4-5% when they were pure B2B many years back.

Margins wise other than Hatsun, both Heritage as well as Parag are (much) worse off than Kwality.

1 Like

Thats a good point, Raising equity i believe is always better than Debt provided they make good use of it. So far the ROEs and ROCEs has been great. So if they use it to generate a better return then as management said it should unlock the value for shareholders.

Also, I think they have raised Rs 300 Cr from KKR already and will further raise 200 Cr from them ?

Its good if company see lots of growth potential and can deploy this much capital, in businesses sometimes these things back fire too … we have to think about can this happen ?

IF its a Steel or Power company for Example raising this much money to setup a new plant , I’ll run away as quickly as possible. Because there exists lot many variables that can back fire as we have seen in past .

By the time plant finishes - (you have no return on invested capital + interest cost ticking from day one) and below can happen -

- price of raw material coal / iron ore could go heywire .

- demand of steel / power could go heywire.

- Regulatory Crap.

Etc

Here what could go wrong ?

This is a business which require lots of Opex not Capex , Demand is solid, From day 1 you can make that capital work for you.

I am not saying nothing can go wrong but my point always been we should not worry too much about DEBT , Pledging 44% crap , Raising Equity too much -> as long as they are able to make great use of it.

So, Lets be watchful of ROE and ROCE. If both are intact i.e, they are raising debt at 8.5% and generating return of 15-20% on it. which great for shareholders.

I think you have to go for DEBT/ Equity funded growth in todays world of very low cost of capital , Its the best time if you can raise money and make best use of it.

Thanks,

Dhruva