Ok the stock is tanking day by day. Now, what is the worst case scenario, what if the ED does charge the distributor who did fraud. What are the charges that will be slapped on the company. And if the company or Balsharaf get a judgment that indicts them, what will be the consequences? Will they appeal the decision and do they get the opportunity to do that. What am trying to sense is how long this case can be in doldrums. It definitely affects the management bandwidth to focus on business.

Meanwhile the auditor change of name is really dubious thing.

Discl: Invested, wait and watch approach up til now

KRBL Company 2018 profit is 430cr agasta fraud is 110cr then 110/430+25% loss. if ED file a suit against KRBL then KRBL pay 25% of his profit (if it is materialized).

but the share of KRBL fall 50% plus from the peak, so the damage is already reflected in share price 2 times the fraud rate.

Well, if we see, when the faith is lost, the premium a company commands will go away.

The doubt itself is sufficient to kill the liquidity in flow. What more is left to be unearthed? Who knows.

Secondly KRBL has commanded far higher premium(P/E) for a few years almost in line of a FMCG minor.

Now even after the fall one can see it is available above it’s historic average P/E.

So, one who conparing the stock with it’s ATH stock price could be proved wrong.

However, if the business shows a good growth in future, sentiments can change so would the price.

Hence instead of seeing a price comfort, one would look at business and or earning growth comfort, which doesnot looks very forseeable.

It’s about weighing pros and cons, and keeping an investment logic very simple.

More so on facts than hope.

My views at current state, for whatever it is worth.

From middle of last year till about Pabrai purchase it went to stratospheric levels. There must have been some amount of stock price manipulation pushing it up, for somebody to get out at the top.

But, current price to me seems fair valued, ignoring all the ‘stories’.

Lets try to see from here on.

Is there any drastic movement of RM prices? No.

Assuming the AW accusations and money laundering to be true, will it impact their sales? Don’t think so.

Will any average buyer think of the accusations before buying their product? No.

Is the average buyer aware of these accusations? Don’t think so.

Will these accusations make KRBL to reduce their product pricing or cause margin reductions? No.

Will any loyalist change their brand after hearing the stories? Poor chance.

Is the stock fair valued? Seems so.

Their could be many other questions scenarios that we can analyse.

But what I feel is their brand and pricing remains intact. So we may be in a sweet spot to move in. Of course it may not be galloping multibagger, But steady returns can be safely expected.

While doing some basic search of the auditors of KRBL M/s. Vinod Kumar Bindal and Co. CHartered Accountants.

I found a very disturbing news article on them.

Here’s a link:

A quote from the article reads - " Brothers Sanjeev Kumar Bindal and Vinod Kumar Bindal are chartered accountants and have been in CBI’s UCM (undesirable contact men) for years"

They are currently under investigation of ICAI.

And I understand they have been auditors of KRBL also for a long time. Did the management not know about these investigations?

Please forgive me if this has been covered earlier in this forum as I have not had a chance to go through all the posts.

great point … These are the reasons why KRBL used to trade dirt cheap before MODI won the elections then on Fancy of bull markets people ignored all these risks.

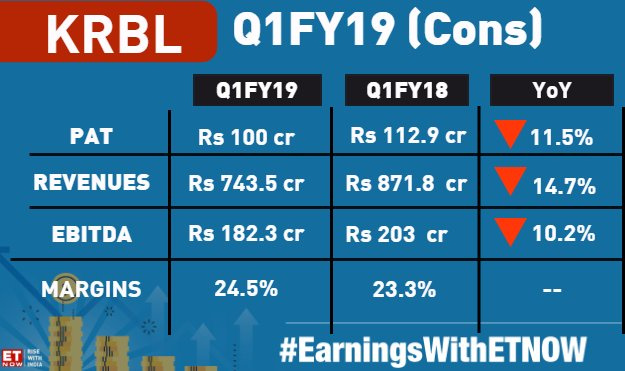

Company is not able to increase revenues for last 3-4 years (Flat/negative growth) and this quarter there is a decline in revenues by 15% & profit declined by 12 percent. Stock is trading at around 19 TTM PE with no growth in sales. Not a good performance…

Resignation of Whole Time Director Mr. Ashok Chand. Reason given: Personal reasons

Change of Auditor: To Walker Chandiok co & LLP

Brief google suggests nothing great about The Auditing firm.

Seems they are auditing Delta corp, NRB bearings, ICICI (recently appointed), Eros, RIL, Amber Enterprises, Capital First etc

As far as the results are concerned, I expected domestic sales to go down due to restaurant’s being exempt from Input tax credit, 5% GST on basmati making it less competitive w.r.to unorganized would bring down domestic sales. Surprisingly, domestic sales grew & Exports were hit.

My wild guess is, it could be due to Iran’s imports being hit due to US sanctions?

First KRBL’s auditors renamed themselves, people raised concerns w.r.t to the auditor credibility, for a “possible” manipulation and then now the auditors has been changed. Isn’t something fishy in this ?

See at the first, even we say KRBL is better placed among the Basmati rice selling companies, yet the valuations are very steep. Even after correction it is quoting higher of its average historical P/E. P/E growth generally is on account of growth in earnings( topline) and margins sustainable over a longer time. As margins have a limited scope of growth hence the revenue growth is better metric.

KRBL loading up so much on inventory and as someone mentioned it played on gross margin to show better profits

Even if one see the results of this quarter there is clear mark down of inventory and hence a higher COGS and lesser margin.

Such things cannot sustain much.

Moreover with recent controversy surrounding it, it realy hurts the sentiment.

Disc: Not invested and find valuations steep. But a potential long term business.