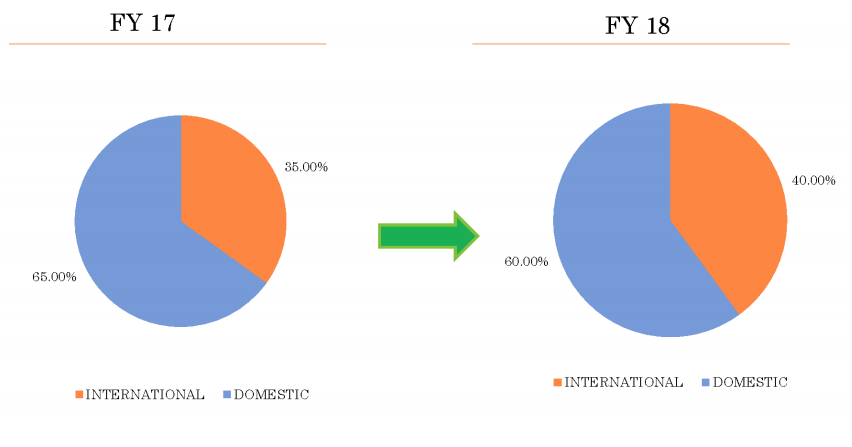

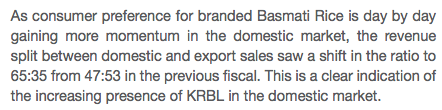

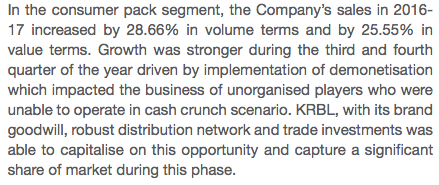

If you see these two section from FY17 AR, they did gain significant domestic market share in Q3 and Q4 FY17 due to demonetisation. Domestic:Exports ratio in revenue contribution changed to 65:35 from 47:53.

They had over 25% in domestic growth in FY17

My gut feel after going through all numbers remains that they have lost a significant portion of the market share they gained during demonetisation. They have posted a flat topline only because exports must have compensated for the loss in domestic market share back to unorganised.

CLSE actually lost domestic market share during demonetisation. FY16 domestic revenues were 94 Cr and in FY17 it dropped to 89 Cr.

CLSE’s export contribution in FY16 was 81% and in FY17 it was 82%. I guess the “Exports” in their name makes sense. Now another way to look at this whole thing is through CLSE’s revenues in FY18 (so far).

By quarters - Revenue has grown QoQ and YoY every quarter.

Q1 revenue growth - 33%

Q2 revenue growth - 56%

Q3 revenue growth - 69%

Overall 9 month growth is 53%. Overall Indian Basmati rice exports have grown 22% in the period which means CLSE has performed really well and provided they don’t lose their 20% domestic contribution drastically, they may do well in Q4 and grow their topline because of their 80% export contribution. It looks to me like if domestic market doesn’t play nice to organised basmati players, it might be better to look at almost pure export players.

This is all based on numbers am seeing. I might be interpreting things wrong so its better to hear things coming out in the concall tomorrow at 3pm.

UPDATE: After posting this, I noticed that they have uploaded a Investor Presentation for Q4. It does confirm that they have lost domestic market share.

Now since I am editing this, might as well add about LT Foods.

This is how their domestic:international revenues look

In short, their export contribution was 39% in FY17 and used to be 44% in FY16 - So they did capture unorganised market during demonetisation (since topline grew 10% during the period). I suspect they may befall the same fate as KRBL in Q4 i.e loss of domestic market share back to unorganised.

If you look at the table above, exports have started grow by value and also realisations in FY18 after a 3 year lull with Q4 showing the strongest growth, I believe whoever has favourable export contribution in the overall revenue mix is bound to do well. It may not be KRBL or LT Foods but I suspect CLSE could do really well with their over 80% export contribution and since they are a small player and growing off a small base.

Disc: No holdings in CLSE (yet)