Harish

The analysis is practical and connected the dots specifically around capital allocation. Thanks for the good work and sharing

Harish

The analysis is practical and connected the dots specifically around capital allocation. Thanks for the good work and sharing

Changing macro, rupee weakening, oil rising ( gulf economy doing well ) could be a positive for this counter since majority of their revenues are realized from exports.

Thanks. Yes, the management has indicated in an interview that they don’t find the energy business attractive anymore. We will have to observe the capital allocation trend in future.

Thanks. I haven’t analysed LT Foods in detail, and therefore cannot comment upon it. Will certainly share my work if and when I analyse it.

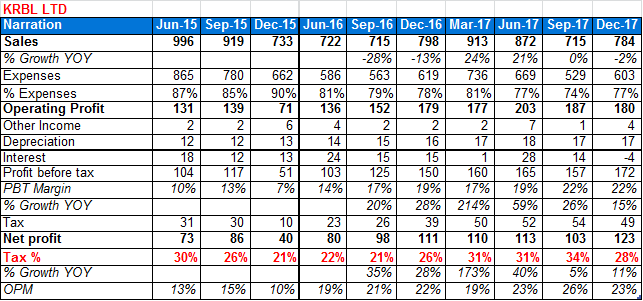

I noticed there is a considerable fluctuation in the tax % and not able to understand. Can some one please elaborate on this. Thanks

Wondering if US likely sanctions on Iran would affect basmati export volumes

Management clarification on impact of Iran deal

Essentially, there is no impact of Iran deal on KRBL as of now as Rice is an essential commodity and it is kept out of sanctions in the past.

Just as a comment, the energy business was undertaken to save taxes by utilising the 80% accelerated depreciation benefit. While I have not done the calculation, management seems rational since this benefit was reduced they have said they will not further invest.

Same issue here too.I cannot see how this can be a multibagger.There is no revenue guidance either.

Has Pabrai really bought into KRBL? As per the latest SHP, his name does not figure there. Though similar quantity of Shares seem to be stuck with CCI, but why would that be so…I guess more questions than answers.

This post above gives a possible explanation to your question, my guess is if Pabrai had bought those shares it would be reflected by now, he may have reneged in light of some new information.

This is all purely speculation of course.

Results out. Numbers are pretty flat.

It seems Year on year, finance cost (30 cr) and increased direct tax (16 cr) ate up all the higher profitability (of 36 cr; 181 cr vs 145 cr) from agri segment. The growth in agri segment profitability is about 25%, which is good. The low inventory cost would still give some cushion for 1 or 2 quarters more (not sure though). I believe, Q4 FY 2017 finance cost was artificially low because of some forex gains (If I remember right).

Please let me know, if my assessment is wrong.

Reason for higher margin may be due to better export sales (up by 25% YOY). But lower domestic sales (15% down YOY) should be cause for worry. Year end borrowing went up by 200Cr but quarterly interest cost went up by 30 Cr… It seems they may have taken bigger loan during the quarter but some of it may have paid back by 31st March.

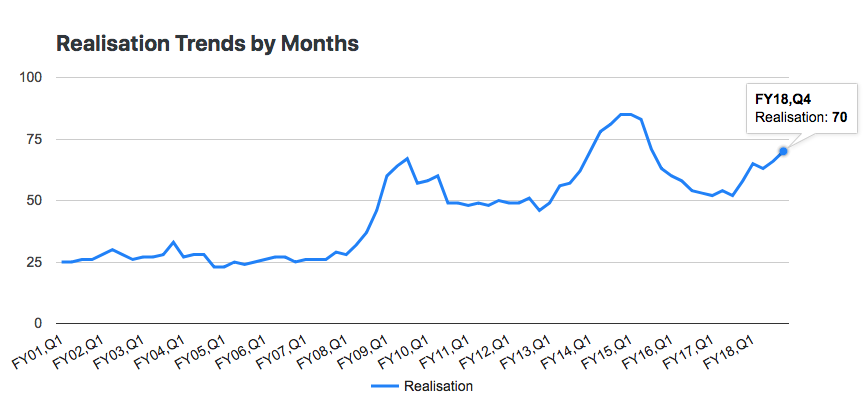

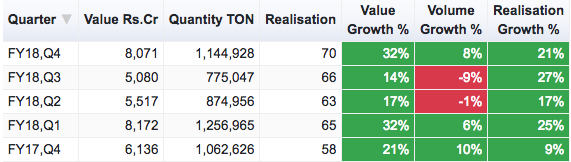

Despite the big rise in exports in Q4 - Rs.8071 Cr by value vs Rs.6136 Cr in Q4, FY17, KRBL has managed to shrink its topline from 912 Cr to 876 Cr in the same period.

The basmati rice export realisation is at a 2-year high (Rs.70 in Q4)

I think KRBL has conceded a lot of domestic market share - Otherwise I don’t see how they could have shrunk their topline when exports have grown by 32% to their target markets. My thesis was on domestic market share maintenance/growth but it looks like that this is not happening. They have still maintained good margins likely because of the export growth but lack of topline growth negates my thesis.

Disc: Exited a bulk of the position today.

Apparent slow increase in topline in domestic sales could be misleading in many companies since ,unlike past, now GST etc are not a part of topline. Key, to my mind, will always remain growth of bottom line.

I have gone through previous 4 quarters results (apart from current one). There is an interesting thing which can be observed.

Q4 FY17 was the first quarter after demonetization. The demonetization caused such a short squeeze that the organized players have taken large share from unorganized players during that quarter. The revenue from domestic agri sales jumped from 429 cr to 630 cr. If we observe the following quarters, there was no such jump. The figures are either flat or decreased by few crores. Due to high base effect, this quarter showed a huge decrease of about 100 cr. If we consider from 2 yrs perspective, there is a revenue growth of 110 cr from a base of 429 cr, which is like 10% growth per year.

Since the cash is back into economy with full force (thus unorganised gaining back market share) and GST having temporary negative effect on organised players, these results can’t be considered bad (though can’t say good either). My guess is small retailers still not willing to come under GST ambit causing problems to KRBL’s domestic growth. Probably, we will get a better clarity post concall.

Good work @harish_balani! Just a comment on your concern of inappropriate capital allocation by the management (@kv1 has in a way shared it above but I am sharing some more specifics). Mr. Anil Mittal’s rationale is available in below mentioned link (last question in the article):

DEEPANSHU: You also have a presence in energy sector. How much does it contribute to your books? What’s the outlook and update on the energy business?

Mr. Anil Mittal: As far as the energy business is concerned, the main reason for foraying into that segment was to take advantage of MAT. For the last 7-8 years we were falling under MAT and the internal rate of return (IRR) was 22-23 per cent. Now because of the current power pricing and the output, the IRR is falling below 22-23 per cent and so we are no more interested in power sector.

I believe if the IRR is below reasonable target rate, and management still continues to allocate funds to unsatisfactory IRR projects then management should be blamed for inappropriate capital allocation. I agree with you that investors need to keep a close eye on how management acts towards the energy business in the future.

Looking forward to more business analysis for other business from you. Good luck!

@GSrikan You are right. If one goes through

Q3 2017 concall when they were asked about impact of demonetisation, they had said actually they got benefitted by it because many sellers dealing in cash had a hard time and that quarter returns during demonetisation were over and above normal. That could be one reason why domestic yoy performance is subdued but let’s hear from them during concall. Was listening to their concalls last week ,so, remember this clearly

I too remember hearing it in the concall. But, I assumed that they retained the market share they gained due to demonetization. It seems it lasted only one quarter. If you observe Q1FY18 onwards the YoY domestic sales growth is either flat or marginally negative. This might be the first quarter they had shown positive revenue growth if there was no demon. We need correlate the volumes and realisations for last few quarters for coming to proper conclusion though. But I am fine with current results. Need to study LT foods and chaman Lal (if they disclose) to see if their revenue is behaving similar or not. If not it means KRBL has been losing domestic market share since some quarters (Is it Amitabh effect?  )

)