Major investment for Hospital is land and buildings. The land in which the Coimbatore hospital constructed was acquired many years back and its cost in books is nothing compared to its present value.

2 Likes

Thank you Gentleman for answering my questions.

I believe that this company is good, and it would keep growing top line by 10 - 15 % YOY, and higher when a new hospital or college comes online. The PAT will keep growing 15 - 20 % YOY, except when margins are hit due to high depreciation or other events.

It would not become multi-bagger anytime soon, but it could continue to give decent returns. The hospital business is asset heavy, and one would need big private equity infusion or lot of debt to make it big scale.

Disclosure : Not invested.

2 Likes

You had posted wrong screenshot.

You are right. Sorry about this.

Presenting some interesting data points.

Kovai population = 20 lakhs (Source: IndiaPopulation2018.in)

Kovai hospital beds = 5000 (Source: 2-2-83.pdf (351.8 KB))

Residents per bed = 20 lakhs / 5000 = 400

Hyderabad population (2013) = 72 lakhs (Extrapolated from 2011 census)

Hyderabad hospital beds = 12000 (Source: Wiki)

Residents per bed = 72 lakhs / 12000 = 600

Initial thought would be “I think the hospitals in Kovai have lower pricing power and this might explain why revenue per bed is lower compared to hospitals which are distributed across India. Does this mean hospitals in Coimbatore have lower pricing power?”

However, patients revenue (don’t include pharmacy) is 45 lakhs per bed in both Kovai and Apollo (as per 2018 financials). Is KMCH special? Or do all the hospitals in Coimbatore have relatively higher pricing power even though we have lower population count per bed in Coimbatore?

Assumed that we have 1000 beds in Kovai vs. 10000 in Apollo in above calculation.

Open to comments and suggestions please.

Questions on costs:

How is the cost of medicines derived? From whom does the hospital buy them? How competitive are the dynamics between the suppliers? Can we get higher discounts as our orders increase in size?

Disclosure: Not invested. Researching as current valuations look attractive.

1 Like

hardly, the crowd catered at the institutions would be totally diffferent.

setting up of proper hospital would take 8-10 years.

2 Likes

KOVAI REDEMPTION

I would call Q3 FY19 the Kovai redemption quarter. Commendable all round performance.

Revenues up 10% but NP up 18% suggests benefits of scale finally getting realised. Despite increase in most expenses revenues have outpaced them resulting in better operating performance.

A pleasant surprise was the reduction in finance charges. As loans had gone up this is possible only if interest rates have decreased (unlikely) or some of the costs wrongly charged to P&L instead of being capitalised now corrected (likely).

Since depreciation has not gone up QoQ I don’t think new facilities/ beds have come on stream. Most likely that either occupancy levels have gone up or they have moved up the value chain (higher realisations due to transplants / more ICU revenues etc) both are positive trends going forward.

One can probably look forward to a good Q4 as well, capitalising on this positive trend and the fact that Q4 last year was an exceptionally bad quarter due to a massive IndAs adjustment to Depreciation.

On balance, fiscal 18-19 is likely to end with an EPS same as that of last year around Rs 53 which is pretty good considering the tough environment, govt mandated salary arrears and the expansion effect.

3 Likes

Clearly, the good result is owed largely to the increase in Sales. The expenses have remained more or less the same. I’m not sure if the new beds have already been put to use. If that’s the case, then that’s commendable work.

2 Likes

Yes! Operating leverages have started to kick in. Doubt if there is any significant addition to beds as:

- Nothing has been reported to the exchanges regarding this.

- There no news of any soft launch of the expansion facility.

EBITA margin over the past 5 years has been:

FY 14-15 25.14%

FY 15-16 21.37%

FY 16-17 24.84%

FY 17-18 23.34%

FY 18-19 22.80% (estimated)

5 Year Avg: 23.50%

Consistently good EBITA margins, despite the many sector headwinds in recent times, will show their sweet impact once revenue growth gathers pace.

The only chink in the armour will be the elevated debt levels.

3 Likes

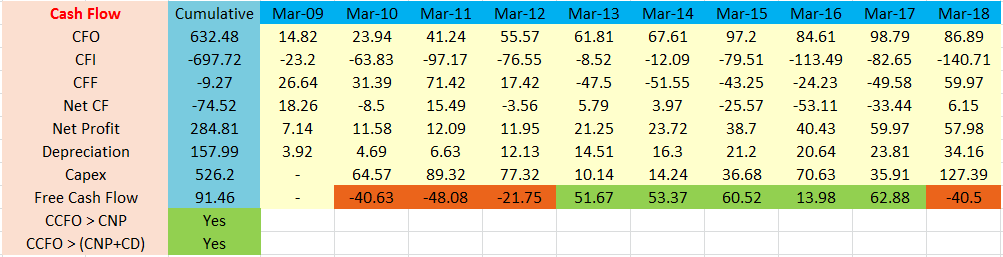

In the past 8 years, KMCH made arnd 445 cr Operating Cash Flow. Out of this, It spent arnd 470 cr CAPEX for the past 8 years. So, Free Cash Flow is negative 25 cr. All these CAPEX helped the Co to improve its sales and profits. But in the past 3 years, net profit remains constant (considering Dec’18 results). Either KMCH should improve its profitability or generate free cash flow that could be used to reduce its Debt.

Disclosure: Not invested. In the watchlist.

1 Like

Sorry sir this is not correct…total operating cash flow for last 8 years are 695 crs and CAPEX of 470 Crs.

Disclosure: Not Invested. In the watchlist

1 Like

Can you please tell me where the 225 cr Free cash flow (according to your calculation) was deployed?? To reduce debt, pay dividend, increase Cash/Investments??

1 Like

Sorry, not a correct calculation bro.

Let me explain how FCF is negative 25 cr.

Past 8 years FCF = -25 cr

KMCH increased its Cash & Cash Equivalents by arnd 79 cr = -79 cr

Co paid 17 cr as dividend = -17

In total, KMCH need 121 cr (25+79+17). So, from where did it get this 121 cr.

KMCH had borrowed arnd 89 cr (including current-maturities of long term debt) in the last 8 year period (FY11 to FY18) = +89 cr.

Co paid Income Tax of 110 cr (In cash flow statements) against 142 cr given under P/L = difference of +32 cr.

So, 89+32 =121 cr.

According to your calculation, FCF is +132 cr in the past 8 years. If it made 132 cr FCF, why did KMCH borrowed 89 cr and where did all these money go?? Just think about it.

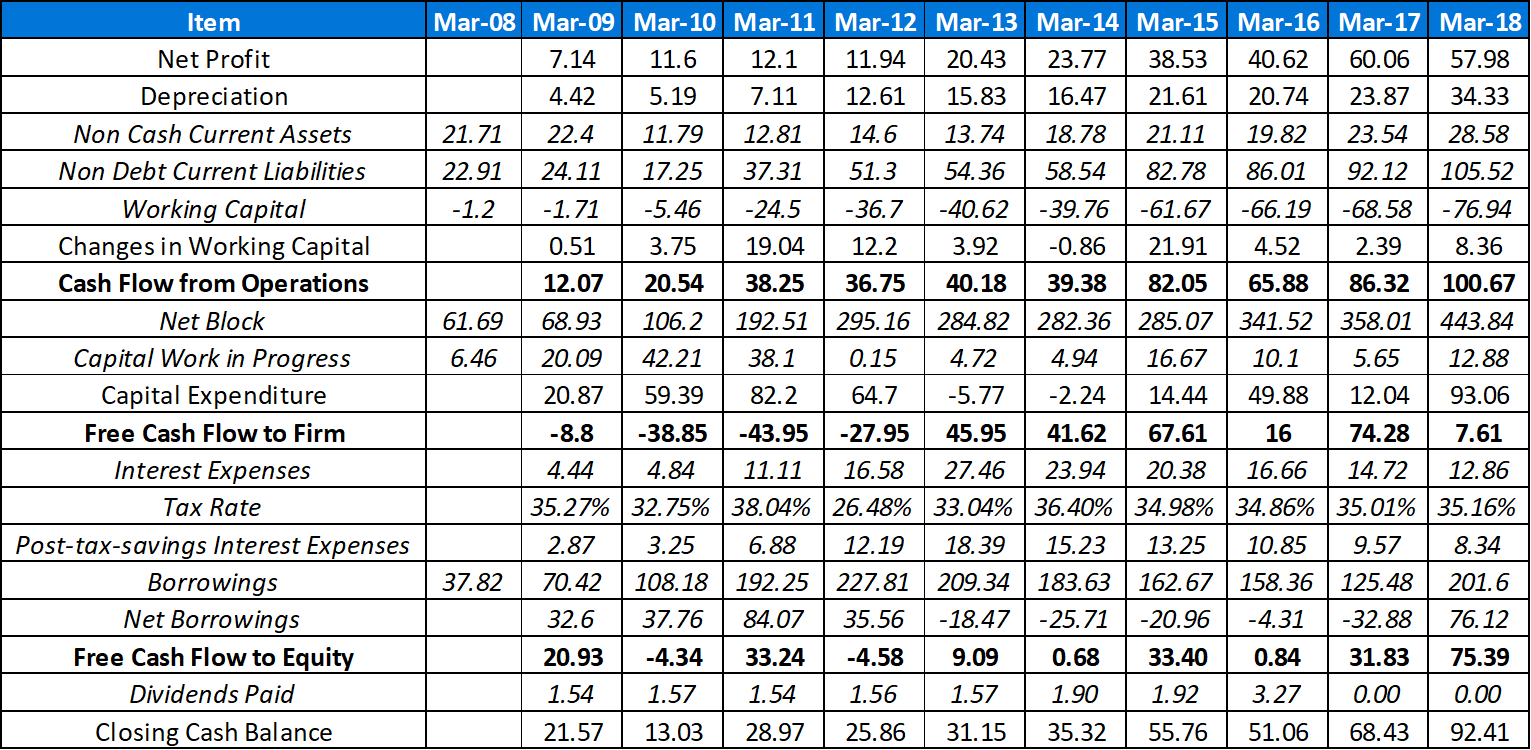

I am not much of an accountant, but this is how it should ideally look like. Do correct me if I’m wrong.

KMCH FCFE.xlsx (14.4 KB)

KMCH has borrowed a lot in the past 1-2 years to build the Medical College. The profits are yet to come in completely. Once those profits start flowing, I am quite sure KMCH will be Cash Flow Positive again. That is pretty much what every investor in KMCH is looking forward to.

Hi Dinesh,

According to your calculation, FCF (Free cash flow to Firm) in the past 8 years (FY11-FY18) is arnd 181 cr. Whenever you finish calculating FCF calculation, check how the Co had deployed those FCF for the period that you calculated.

From FY11-FY18, KMCH had borrowed arnd 89 cr (including current-maturities of long term debt) - It came arnd 93 cr when I rechecked all the ARs. Co increased its Cash & Cash Equivalents by arnd 79 cr and paid 17 cr as dividend. So, where did the FCF of 181 cr go??

I checked your calculations. OCF seems to be overstated. Also CAPEX is arnd 470 cr but in your calculation, it is just arnd 308 cr. Hope it helps.

IMO cash from from debt cannot be added to free cash flow to equity. Money raised from debt is never free to distribute and carries some charge over the assets.

Also consider, if this was true, any company with high debt will report positive cash flow to equity, even Suzlon, JPAss etc types.

I personally calculate free cash as Cash from operations, less (net) amount invested in fixed assets. One can reduce interest payments from this, if he wants.

I won’t reduce dividends as they are free cash and actually distributed.

If this free cash is positive, the company shows sustainable growth as it can fund its capex from internal business sources. I do not reduce interest payments from here, but I do check interest service ratios and debt levels before investing. A check on gross debt is also important. It should not rise much.

True, from a legal point of view I guess. But when you take Debt, you pay interest and get the right to keep it for the time you pay the interest. So, it’s like that money is owned by the company. Also, companies do borrow to pay dividends once in a while, not that it is a good practice.

And if I agree with you that Debt should not form part of FCFE, what should I do with interest expenses? Ignore it from FCFE calculation? If not, why the discrepancy where you consider interest expense as an outflow for the company, but Net Debt not an inflow for the company?

I have not reduced Dividends. I just showed it alongside FCFE and Cash.

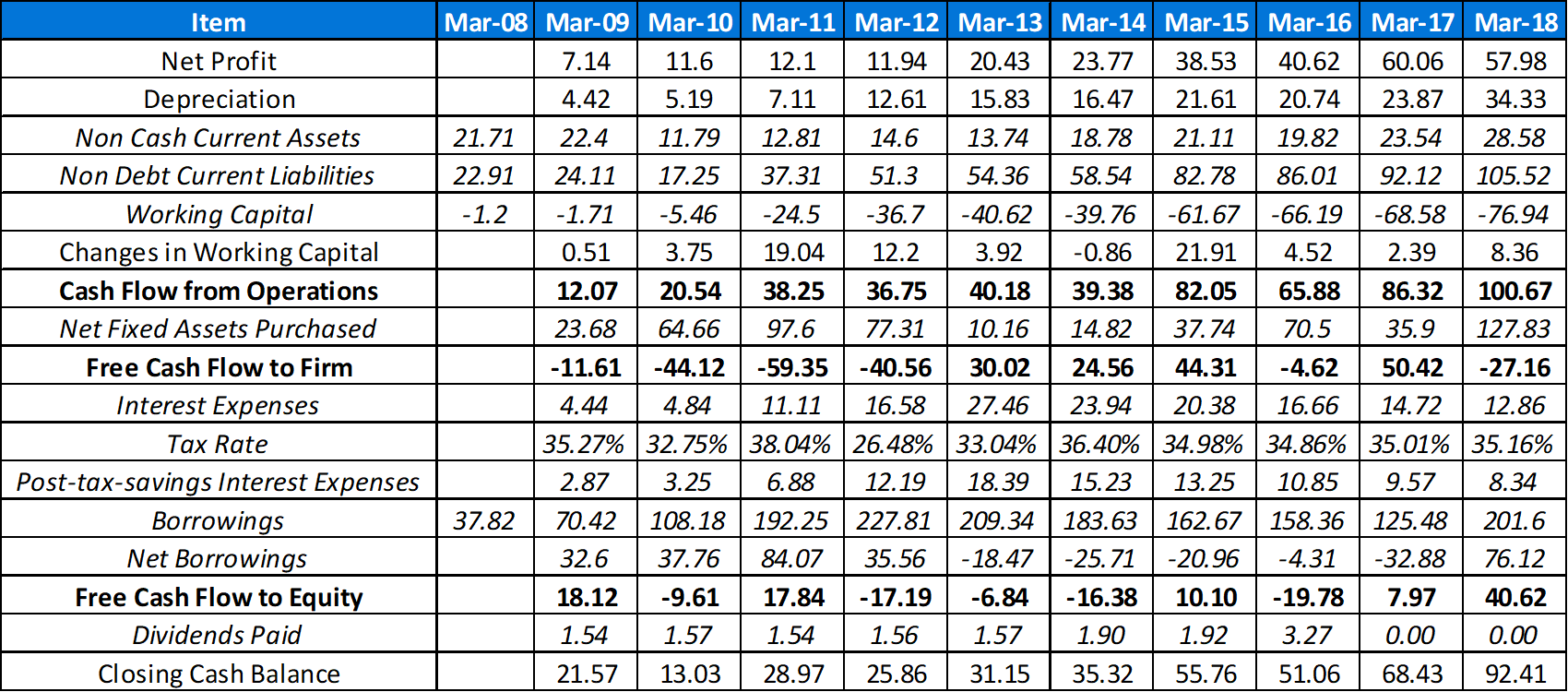

KMCH FCFE.xlsx (14.2 KB)

I tried to calculate Capex indirectly, and I guess some numbers may have been over/understanted there (Took data from Screener). This time, I took the numbers of ‘Fixed Assets Purchased/Sold’ directly. I think this is a better representation.

FY2011 - FY2018

Cumulative FCFF = Rs. 17.62 Cr

Borrowings = Rs. 89 Cr

Dividends Paid = (Rs. 17 Cr)

Cash and Bank Balance = (Rs. 79 Cr)

Interest Paid = (Rs. 8.02)

Balance = Rs. 2.60 Cr (Probably some rounding error somewhere).

But if you notice last year alone, Borrowings have increased by ~Rs. 80 Cr, a significant jump. But this additional capital hasn’t started producing any cash flows yet. That’s the point I was trying to make.

Personally, I do not reduce interest payments. People may argue and want to reduce as it is a definitive outflow.

The reason I do not reduce interest payments is that, if the company is generating enough cash flow, the debt will be repaid sometime in future and hence, reduce interest payments overall in coming years. So, the cash flow net of interest, may lead to underestimation of company’s potential.

Debt that comes in, has to go out. If you see the cash flow over the years say 5-10 years, the debt will come it and get paid not affecting the cumulative cash flow which I think matters most. But adding it first and reducing it later impacts the assessment in short run.