15147efc-7543-4cfe-a9dc-9317a497e28d.pdf (1.2 MB)

Auditors resign. There were corporate governance issues like bad reporting of related party transactions including their purchase of medicines from pharmacy subsidiary in erode, canteen operations and parking lot issues with local farmers.

They reported a sudden decrease in revenue and profits and immediately auditor resigns.

Curious. Where were these Corporate Governance issues discussed/mentioned? Auditor’s rotation is a normal practice, if I’m not wrong. It looks like KMCH asked the Auditors permission to rotate early and they agreed. It doesn’t look like the Auditors resigned voluntarily.

Auditors hv been appointed until 2019-20 and what is the sudden urgency to request auditors to resign. Prima facie, the RPT issue raises apprehension whether this has anything to do with the resignation of auditors. Hope all is well.

As far as I heard, the signing partner is going to remain the same. It looks from the signing partner wanted to switch from Haribakthi to some other audit firm (Which will probably be chosen as the auditors). So the terms of the audit hasn’t virtually changed.

It’s all guess work until June 23, when they’ve planned a Board Meeting to fill the vacancy.

Yes, we all hope there is nothing to worry about here…also the sudden increase in depreciation is something I have noticed in many companies which switched to Ind AS for the first time. It could be the same here as well.

Also, to put things into perspective this is a 1000+ bed hospital complex situated on a prime property of 27 acres close to the airport and it generates close Rs 100 per share in cash every year. Promoters added over 1.2% last quarter and are willing to buy block as and when available.

Being in the hot sector this hospital is worth way more than the current price.

However, it is also true that when sentiment takes a hit and panic prevails it takes time for valuations to recover. Some deep pockets needs to come in with conviction to take it up. When that happens you can see multiple upper circuits. Until then just stay with fingers crossed and see what happens on June 23rd :))

All cos face problems at one time or the other and what ultimately matters is how management responds and rectifies things. Hope this works as a wake up call for the promoters to engage the media more and be transparent and set things right if something has gone awry.

It has had a great run from 100 to 1,400 and its time for earnings and corporate governance to catch up.

Just for information…Haribhakti and co have also resigned from PRICOL citing the same reasons (internal restructuring) they gave for resigning from Kovai. Make what you will of it :))

FROM THE ANNUAL REPORT JUST ISSUED

Medical College proposed to be established for an annual student intake of 150 undergraduate

students. Construction of 700 Bedded Medical College Teaching Hospital is underway and is

slated to complete by end of March 2019. Other infrastructure like Students’ Hostel, Staff

Quarters are also under construction. The total cost of the Project is put at ` 600 Crores and is

proposed to be part financed by way of a long term Debt. It is expected that the first intake of

students will commence from academic year 2019-20. The Medical College will allow your

Company to enter into low cost segment thus making KMCH into a comprehensive healthcare

institution and also have an education foray.

KMCH has about 110 Cr in Cash and Investments. Their yearly Accrual is around 60 Cr. So that means the Long Term Debt will be around 440 Cr, on top of the already existing 85 Cr. I hope they can get this Debt at a low cost and quickly pay it off with the revenues from the college. Otherwise, this is going to be a drag on their profits.

PS. They have already taken in about 100+ Cr of long term debt this year itself. The details of the new loan are mentioned in Page 192-193 of the latest Annual Report. Looks like they’ve given pretty much everything they own as security. This is high risk venture. I hope they do it right.

Going purely by their past track record when they took over 250 crs loan for the major expansion of almost 750 beds one can be fairly confident that they know what they are doing. But it surely is a case of short term pain for long term gain in this capital hungry sector.

I would still prefer a major portion to come from some PE investor or Venture Capitalist or even a low cost loan from Institutions like IFC or the like since it is for building a college… Even a low priced rights issue would be good since interest rates are likely to rise in the coming years.

They haven’t disclosed the Cost of Debt, but going by BSE’s Corporate Debt Trading data, I would put it around 9.5% for KMCH. Cost of Equity, going by CAPM, is somewhere around 12.5% or so.

Debt is still the better option, speaking from the vantage point of Corporate Finance. A PE investment and the subsequent equity dilution would actually prove to be costlier for individual investors in the long run.

AR 2017-18. Page 109

What is this >> ‘During the year, the company has capitalized

`108.61 Lakhs (Previous year - Nil) as borrowing cost as per provision of Ind AS 23 - Borrowing Cost’. What it means? Kindly educate me.

Disc : invested.

A company can capitalise borrowing cost if it meets criteria as per Accounting Standards. It means part of borrowing cost (Rs 1.09cr) is reduced from Finance cost and added to CWIP as the borrowing was specific to the project which is under progress.

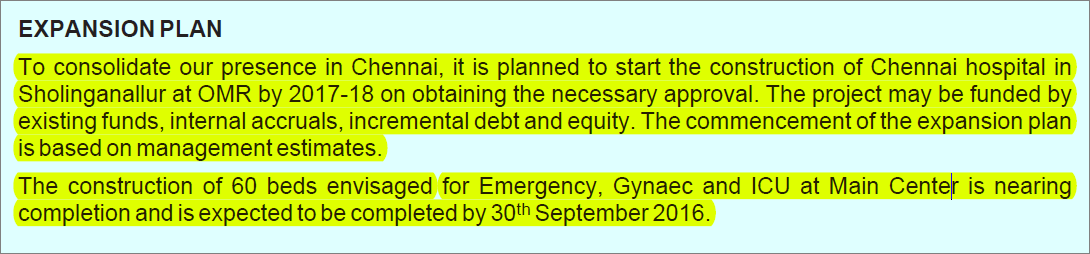

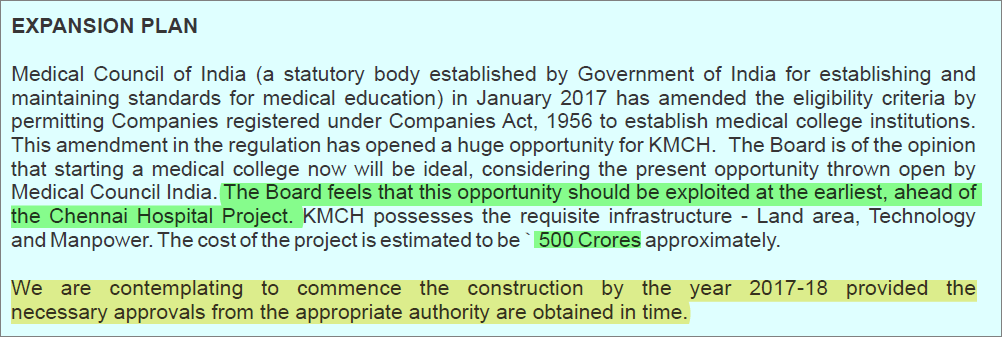

So glad that they have dropped the Chennai hospital project planned in an already saturated market!

I suppose the WIP is in respect to the ongoing college and other expansion projects going on. On an average they tend to add approx. 100 beds annually as per the hub and spoke model they are currently pursuing.

June 18 shareholding pattern is due to be out anytime now.

Auburn Limited an arm of ChrysCapital was holding over 1% as of March and based on aggressive buying seen before the IND as led muted March results I won’t be surprised if they have increased their stake even more.

Current developments seems to have spooked this buyer who has suddenly turned quiet and probably planning its next move. Also, waiting to see if Sundaram MF has stayed put or changed their near term outlook.

Another imp thing to look out for is if they have dematerialised the remaining two promoter holdings. Once this is done it can move out of T2T and could even list on NSE ,if promoters so desire.

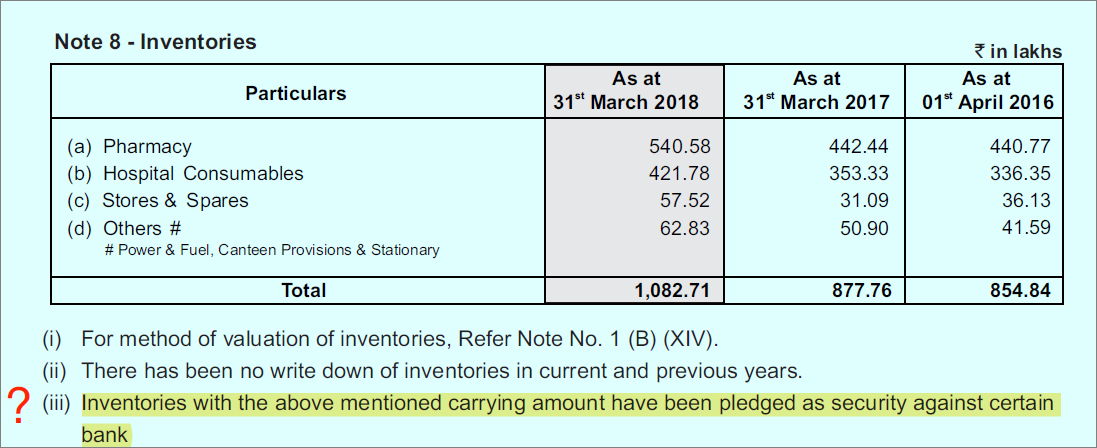

“Inventories with the above mentioned carrying amount have been pledged as security against certain bank” Bank is providing loan against ‘non-fixed’ asset, is it possible?

Banks don’t discriminate between fixed and non fixed assets. They just need a tangible security to hedge their credit risk against.