http://www.bseindia.com/xml-data/corpfiling/AttachLive/c071e0e8-4d95-4d5a-80dc-e4c33610066f.pdf

3 Likes

Excellent results QoQ, but flattish YoY (I guess we already knew this).

It looks like the leverage is finally paying off. A few more quarters (Probably like a year) and we can figure out the Economics behind the Medical College.

Rs. 3 / Share Dividend

1 Like

for the quarterly results, it’s not right to see QnQ results as there are seasonal variations. The better way to see is YoY. Hence, largely flat results

Agree completely that these are rock solid results considering that the eco systems has been so full of head winds for the hospital sector.

YoY profits are not comparable due to a huge Dep charges last year due to the Ind-AS adjustment.

If you compare EBITA then they are almost the same around 21% give or take a few basis points.

It has declared the highest ever annual profits 60.14 crs!! Profits have almost tripled over the past 6 years without any increase in Paid up Capital showing good cash generation and deployment. I consider this as a very prudent and steady growth in the hospital sector.

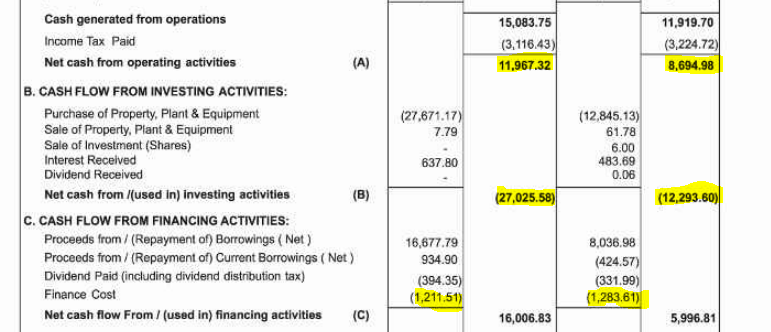

Borrowings have doubled and interest cost continue to be capitalised sparing the P&L of pain.

Trade receivables are down 20% despite an increase in revenues, which is really good. No of days in receivables is amazingly low at less than a week!! One may argue that hospital business is largely a cash cow but then don’t forget that collection of revenues from Govt. schemes and corporate business can and have been difficult for many hospitals. I suppose TN has always had a very efficient Govt.healthcare system compared to other states.

All this is great but what about valutaion?? That’s what the minority shareholders are concerned about.

Kovai is languishing at sub par valutions despite performing excellently quarter after quarter. But like they say, without a jockey even the best horse is of no use!! Mera number kab aayega??

Avg. hospital valuations are around 35-40 times earnings /13-16 times EBITA /2.5-3 times revenues Against this Kovai trades at a PE of less than 15, 6.25 times EBITA and 1.4 times revenues

God knows what more they need to do to get re-rated, that too in a sector where lousy 3rd rate hospitals are quoting at sky high valuations without showing any performance year after year!!

4 Likes

We already knew that the first two Quarters were bad. I think it’s great news that the leverage (Both financial and operational) is finally paying off. The Medical College should start contributing more from next year too.

On a side note, KMCH should seriously stop this bad practice of capitalizing interest expenses.

1 Like

I was so wrong or outdated…to say that hospital valutaions are between 13-16 times EBITA

Medanta is being bought by Manipal Hospitals at a whopping valuation of 24 times EBITA!! That too a for a hospital sinking under debt and making losses!!

At this valutaion Kovai should be just over Rs 3,000 per share. I am willing to accept even half :)))

Thematic-PE Deals-May 2019.pdf (456.3 KB)

This has been going on for some time now. PE investments in hospital sector increased by 155%.

2 Likes

Quick notes from AR

Medical College ETA

“A couple of years” seems dire. But I suppose the college will start contributing something from next year.

Idhayam Merger

Idhayam merger has gone through completely. We already knew this earlier.

Flat DPR

DPR is more or less the same (~5.60%).

Decrease in Promoter Holding

Marginal decrease in Promoter Holding, largely due to one Dr. P. R. Perumalswami offloading a small stake.

Investment by ChrysCapital

ChrysCapital Investment Advisors India have invested a LOT in KMCH this year via Auburn Limited. Stake has more than doubled from 1.06% to 2.44%

Industry Developments in 2018

I had discussed some of these things in my own PF thread:

Otherwise, pages 51-54 in the AR is a good read too.

Visibility on Medical College

Some more visibility of the Medical College.

Increase in ARPU

ARPU has increase by a decent amount (~8%).

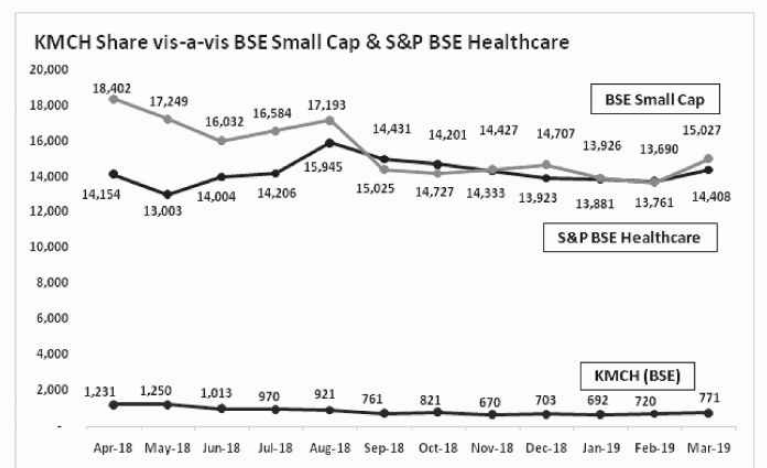

Funny Representation of the Share Price

Somebody doesn’t know how to use an Excel in KMCH. ![]() At a quick glance, you’d believe that the share was largely flat during the year.

At a quick glance, you’d believe that the share was largely flat during the year.

Decrease in FCFE

Stark decrease in FCFE, thanks to the Medical College I suppose.

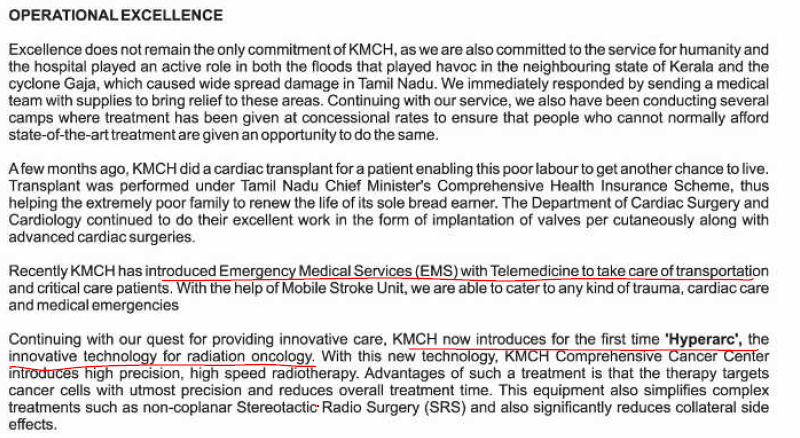

New Technology for Radiation Oncology

On limited Google research, it looks like the first patient to be treated on this technology in the US was in 2017. Also, the first patient ever to be treated with this technology was also in 2017. So considering this, I’d say KMCH adopting it shows a nimble attitude. Some other healthcare groups in Australia and Korea have also adopted it in 2018.

8 Likes

It was actually good to go through this year annual report - it is much more detailed and has lots of insights. Dinesh has already covered a lot of things…just adding a few more that might have been missed

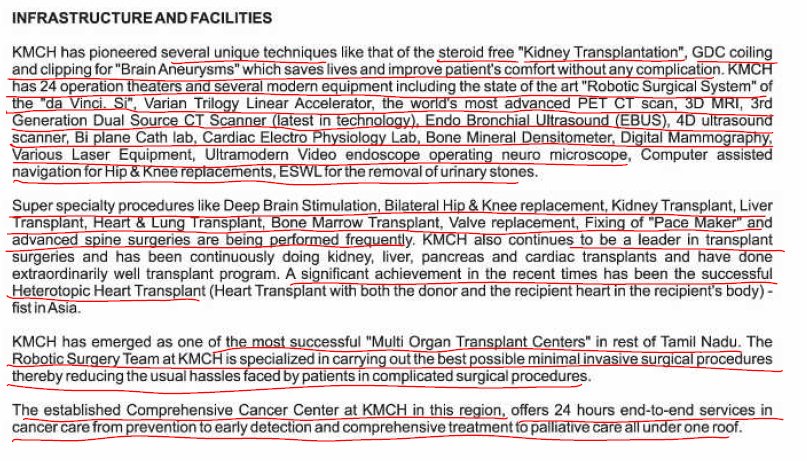

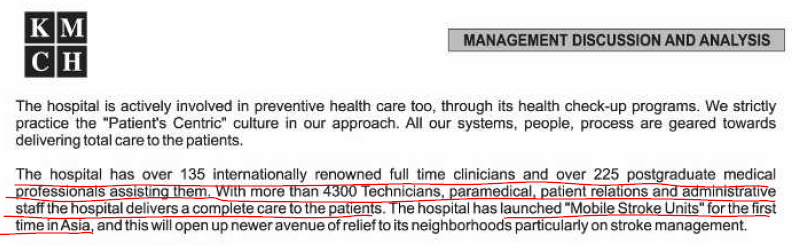

I have always felt that this hospital has focussed on technology and tries to be the first to do some of the new things in the industry. Here is a good extract from annual report:

10 Likes

3 Likes

Good news comes at the right time ![]()

https://www.bseindia.com/xml-data/corpfiling/AttachLive/5e5f3995-e12b-4728-b8dd-78d25de1234a.pdf

6 Likes

The NMC bill is good news for private medical colleges in general. since last few years private medical colleges have been struggling ( there may be differences between north and south ones and i am talking about ones in MP, Rajasthan and gujarat) and many private colleges have resorted to delayed salary payments ( till 6 months in some cases), which is the current scene now.

-

The yearly MCI inspection used to be a torrid affair with MCI inspectors demanding huge bribes for the college to be passed, which will now become easier as in NMC it doesnt need routine yealy inspections

-

The admission criteria till now has been NEET excluding NRI seats. so there was a capital crunch in these colleges. Some college were still demanding donations under the table but many were stuck on to increasing the tutions fees for which there is a ceiling as far as MP goes. no that 50% of seats will be filled by the management ( as per NMC), that shud ease out ( the qualilty of doctors pouring out is another controversial topic)

-

It will be interesting to see how kovai manages the donation part if they take at all. For the ones who take donation its almost equal to the whole MBBS 5years tutions fees. the donation part is black…not easy to show into accounts.

disc: not invested

5 Likes

The last part is my concern too. Even if the management tries their best, the Medical College business is rife with hand-outs to authorities. Will it be different for KMCH, since they are a listed entity, answerable to the common public? We’ll have to wait and see.

1 Like

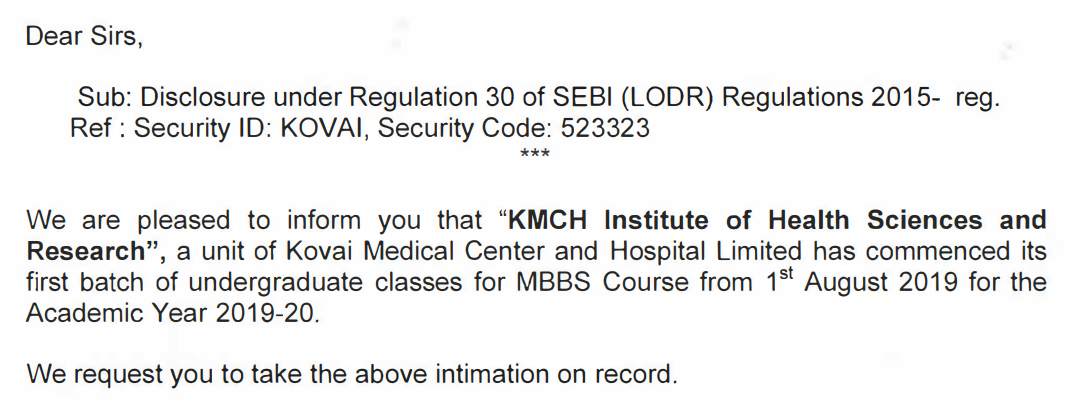

Q1 FY 20 results are out

Excellent result on all fronts.

1 Like

Good results. Love it amidst all the mess around.

But am not sure if it is excellent, unless it means slow and steady progress with monotonous increase (definitely would prefer this to other kind)

Disc: KMCH is my third largest holding.

I get where you are coming from, but if my assumptions are correct, Sales and Profits will see big leaps for at least the next 2 or so years The last two years have been brutal in terms of reinvestment (i.e. Massively negative Free Cash Flows) and a big reason why the share dropped almost by half. If you’d like it explained via the P&L, essentially the Sales were growing nominally, while Depreciation spiked due to more Assets (Read: Building/Structures) and construction WIP on the books. This is standard for any company coming out of a big Capex.

Read this short note by @varadharajanr to know more:

1 Like

Margins have dipped… Y-o-Y… On sales of Rs 165 cr (vs Rs 151 cr) operating profit is Rs 36 cr (vs Rs 35 cr). Increase in EPS is mainly due to low taxes. IMO the result are okay-ish… Even if this tax rate is permanent thing, this line item can’t be squeezed/reduced further percentage wise…

So, if next year, the tax is paid at previous %age, there will be a negative impact otherwise PAT may show growth in line with top-line.

Disc: Invested

While the results are commendable considering the ecosystem hospitals are operating under I would not be euphoric about the NP of almost 20 crs. Mind you this is close to the annual profit of 23.73 crs in FY 13-14. What makes this creditworthy is the fact that there has been absolutely no dilution of equity during this growth phase.

Going forward I would be hopeful but brace for hits from Dep and Fin charges from Aug 1 when the College started functioning. The annual report says that a part of increase in Employee costs also relates the college faculty (Pg59). The fee allocation in the coming quarters could slightly ease staff cost expense ratios.

Current Tax provision at just 26% compared the annual average of 35% over the past few years certainly raises eyebrows. This is likely to be compensated in the coming quarters.

Hospital has reiterated about entering the low cost segment when the new beds get operational. This is likely to drag overall margins down unless there a quantum leap in the ARPOB of existing beds (if they get more transplant and high cost surgery patients and shift the regular patients to the new beds).

The biggest positive right now is the EBITA margin performance. At almost 27% it has been the best so far and indicates operational efficiency. If this trend is maintained then there is every chance that the earnings trajectory will accelerate in the coming years.

A mixed kind of quarter …am happy but wondering about what’s coming next!!

Valuations continue to be depressed as usual and the only thing left for them to do is to list on NSE and hope some jockey notices this thoroughbred

All good points.

Even if you artificially apply a Tax Rate of 30-33%, that would still mean a NP growth of ~6-9% or change. That’s still better than the flat results I was expecting until the Medical College started pitching in.

Also, I don’t see why we should expect more Depreciation and Finance Costs. They have been high for the last two years, but have recently started flatlining. In other words, there would be no need for a new Capex and so in turn, Debt.

I would expect them to stay on the same levels, while the increased Sales from the Medical College will make up for the “lost” Profits since the last 2 years.

Hi, interest and depreciation expenses which were earlier being capitalised are now likely to be routed through P/L account from Aug 1, post commercial operations of the medical college. To put things in perspective, total borrowings of company was ~Rs. 380 cr. as on March 31, 2019, however, interest expenses in P/L was only ~Rs. 12 cr for FY 2019. Even if I assume 9% cost of borrowings, the annual interest outgo will be over Rs. 30 cr, most of which I believe will now start appearing in P/L account. Same holds true for depreciation as well.

Thanks and Regards,

1 Like