Heard export is new weapon to bypass GST. Not sure how true it is but anything is possible in a jugaad econony

2 Likes

Since I am doing a lot of reading on population trends , population ageing and related aspects - I have a suspicion that baby births follow some sort of cycle. The birth cycle has been falling in the US for sometime now and it would be interesting to understand the birth cycle in further detail. The kitex story is directly linked to the birth cycle and it would be great if someone took this up. This thread needs to move towards shedding more and more insights on the root causes of understanding a business. Too much time is spent on other things tangential to this. The implication of this is that if a birth cycle exists then kitex becomes a cyclical stock and could behave like all cyclical stocks. My personal views!

6 Likes

1 Like

For a Chapter 11 proceeding, the creditor has to file a claim for it to appear in the docket. It is not an automatic listing of all due amounts. Kitex still has time to file - it is 90 days from the date of first creditors meeting.

Also as discussed before LC export does not necessarily mean that Kitex may escape write offs. The bankruptcy court can recall the payment made if they determine that a wrong priority was given.

Disclosure: I don’t hold any position in the shares of Kitex Garments and don’t intend to take a position in the next 7 days.

1 Like

Decent results by Kitex. No visible signs of Toys R Us impact.

http://www.bseindia.com/xml-data/corpfiling/AttachLive/dcf10e7d-18cc-412a-8a37-db0fe463cd99.pdf

Increase in CWIP. Is this for the automation?

Short term borrowing of 53Crs.

Disc: Invested long time back(3+ years)

1 Like

Kitex Fantastic Q2 Results. ![]()

![]()

![]()

Revenue up 47%, Net Profit 85%,

Revenue from Operations at 148.6 cr vs 106.9 cr (YoY), Profit at 24.1 cr vs 13cr (YoY)

so six months: Total Income 282 cr vs 229 cr.

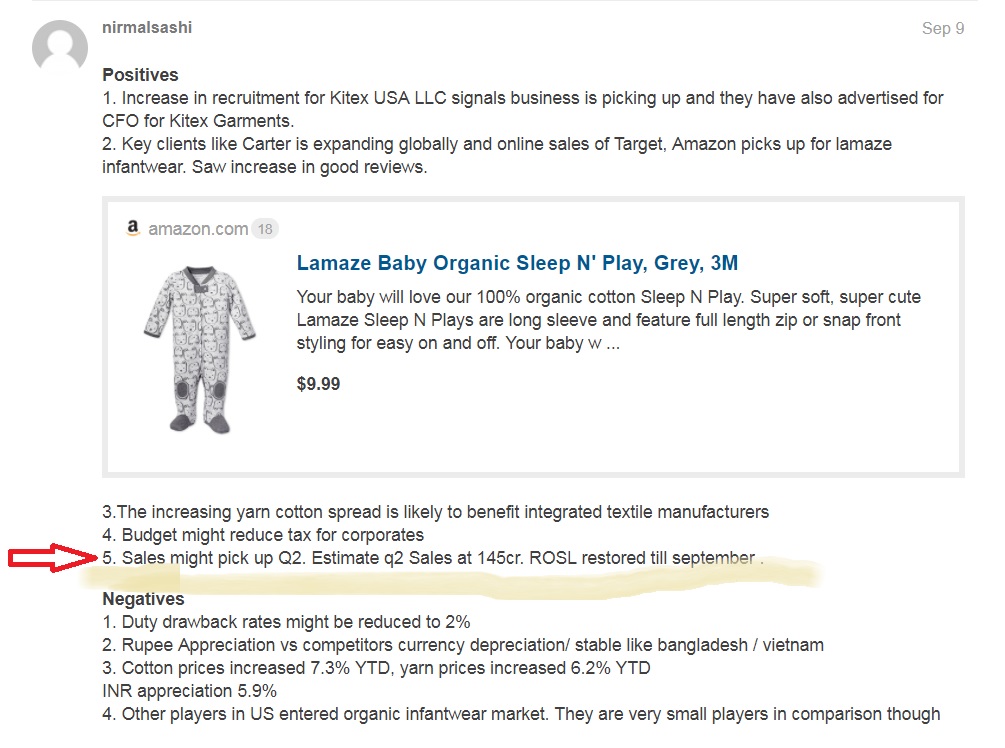

Met my expectations in all parameters in Q2. On Sep 9, 2017- I did mention in valupickr forum above that I expected Kitex q2 to be around 145 cr and duty drawback to be around 2%![]()

Guess apart from ROSL restoration last quarter, INR depreciation, lower yarn prices helped along with the core direct operations with own brands - Little Star and Lamaze

Other Decisions:

-

Dividend: Interim Dividend of 75% ( Paisa Seventyfive per equity shares of Re. 1/- face value). Dividends will paid to the shareholders on or before 30th November.

-

Further investment of USD 1.00 Mn in Kitex USA LLC during the year 2017-18

1 Like

Hi Bheeshma,

I think we should look at market demand once Kitex is major supplier like number 1 to 3 (US market size US 2 billion ). They are not at this stage. If there is cycle it should affect first Carter. Plus they are supplying to companies like Carter which are now growing global. So right now lot of room for kitex to cover before getting worried on population trends etc.

1 Like

Q2FY18 Earnings discussion on CNBC TV18

- Good revenue increase because we are trying to increase the revenue in Q1,Q2,Q3 similar to Q4 levels. These are due to internal improvements we have done. We will see the effect of these improvements in the coming quarters.

- GST paid in Q2. We claimed duty drawback so we cannot claim GST input credit for Q2. Further clarity on how the duty drawback and other tax credits related to GST will be in Q3, Q4 are awaited. This impacted our profit margins slightly too.

- Short term loan taken to tide over the GST related problems. Debtor days and inventory gone up. We could have used our surplus but we feel the dollar account would do better. So temporarily borrowed.

Unfortunately no details about customers were discussed - I expected someone would raise Toys R Us issue, details about new customer acquisition etc. Also, no details about Lamaze, private label brand related details were discussed.

Disc: Invested long time back(3+ years). I have tried to summarize as per what I heard. Will try and post the video link when available.

3 Likes

Kitex Garments: CNBC Interview Link: http://www.moneycontrol.com/news/business/earnings-business/trying-to-balance-all-quarters-gst-impacted-profits-kitex-garments-2430227.html

ICRA: Kitex Garments https://www.icra.in/Rationale/ShowRationaleReport/?Id=63079

ICRA: Kitex Childrenwear (Promoter Entity)

https://www.icra.in/Rationale/ShowRationaleReport/?Id=63080

3 Likes

Any inputs

- Capex : 240 cr, can increase to 500cr ?

- US custom: big positive

- I liked the interview of sabu mentioned by team valuepickr. Can some one from team valuepickr contact md sabu and get another round of discussion. Motilal oswal is not hosting conference call and the team could give better insights. my experience with media quarterly discussions is that they are too focussed on bottomline and miss the bigger questions

A. New customers

B. Automation plan, capex

C. Plans for future cash utilization

D. Present status of doubling turnover by 2020: challenges and current plan

E. Toys r us receivables and other receivables status

F. CFO and merger plans

G. Status of pending claims for tax, pf, drawback.

H. Current market opportunity for infantwear. Effect rosl and duty drawback

I. Plans for india sales

J. Plans for own brand, current sales and next year for little star

K.Lamaze !

L. Other promoter related entities

kitex now launched travel bags

also undergarments …

kitex stocks have been falling down since they entered politics …

there political party is named 20 twenty … n they r doing many good work spending money for local kizhakkambalam panjayat people for winning election and last election they surprisingly did won !

they hav opened a supermarket for local people to shop good stuff way cheaper than market rates …

Dear fellow investors/experts,

This is my first post in the forum, though i have been reading the forum. This is a wonderful platform for novices like me and a great learning source.

Coming to Kitex Garments, I know that there has been quite a big amount of analysis and discussion about KGL-KCL issue, which is my main concern as well. I was baffled with the questions like how will they divide the orders, cant they just put more orders in KGL kitty especially since KGL the public entity is not doing well of recently, how do they divide the balance sheet between KGL and KCL etc. However from this thread i got answers for them.

However, when i compare the figures of KGL and KCL, and again those of KGL and the combined entity KGL+KCL, and plot the graphs (attached)), I am getting more baffled than ever. KGL vs KCL and KGL vs KGL+KCL trace eerily similar lines in the graph (except for sales and profit in the former case).

Any thoughts on how to make sense of these? The comparison may corroborate what the MD claims - that he is trying to grow both companies, with more preference to KGL. However, there are these haunting questions still - How can they divide in such a way? How can they both be nurtured in such a correlation?

Look forward to more insight.

Best Regards,

Johns George

4 Likes

An update on the actual consolidated revenues in Cr 511, 546 & 546 for years 2015, 2016 & 2017.

1 Like

I decided to visit Toys R Us which was opened couple of months back in Bangalore - mainly to check if Kitex manufactured garments were present. There were racks of baby garments present from various vendors like - First Step Baby Wear (Bangalore based), GM garments(Mumbai based) and a couple of other manufacturers(forgot their names).

Then I found a whole rack of baby garments under the brand name Koala baby…All the garments under the brand name were manufactured by Kitex Garments. The quality of clothes were certainly a notch or 2 higher than all other baby garments I checked in the store. Please find couple of pics I took at the store.

Disc: Invested for a long time. Views could be biased. The above info may not have any material impact on the revenue of the company in the immediate future. Just a datapoint to show that there are opportunities like this which may arise for the company in other geographies. But as Mr Sabu has said in the conf calls in the past, US is the largest market and other geographies are not his priorities at the moment.

12 Likes