Kitex Garments - Updates

Kitex Garments Ltd has informed BSE that 10,96,950 equity shares of Late Mr. M.C. Jacob, promoter of the Company, constituting 2.31 % of outstanding shares of the Company is being transmitted to Mr. Sabu M. Jacob, Chairman & Managing Director who is a Successor as per the Succession Certificate issued by Court of Sub Judge, Perumbavoor, Kochi and now confirmed by respective Depository Participants on October 04, 2016.

One thing from the document that got my attention:

“Although the history behind KCW

existence has some plausibility, the

owners have rightly taken the decision

to merge the two businesses, appointing

Ernst and Young as a consultant. And in

order to maintain full transparency

it has been agreed that KCW will be

listed first, before the businesses are

merged, a process we expect to take

18-24 months.”

Is this statement correct? Is there an official confirmation that KGL has appointed Ernst & Young as a consultant to decide on the KGL-KCW merger? Does anyone here have more information on that?

Thanks @kaustubhkale & @ashwinidamani . I knew that Mr. Jacob had mentioned about the merger during his earnings call many times. But I wasn’t aware about the appointment of Ernst and Young for the same purpose.

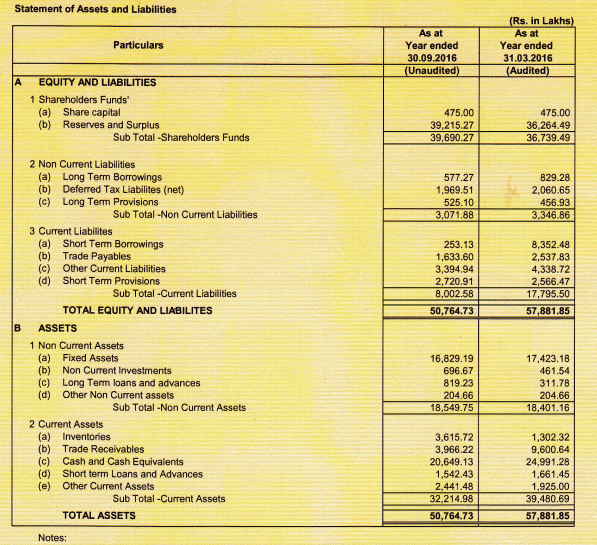

The balance sheet has become more strong. Significant reductions in Long and Short Term Borrowings. Decrease in Receivables too. Inventory is building up.

Mr. Sabu was on ET now. As per him, 35 crore of sales has been hold as inventory as 2 of clients are waiting for USA election results and have asked to hold for few weeks. As per him, he is still committing 20% growth target.

Any reason why USA clients would like to hold on to inventory due to election results ? Any long term/short term impact they see due to elections?

Note : Part of extended portfolio and still under tracking position

I did some search on web trying to understand the correlation between the US election and customers deferring infant wear. No luck sofar.

It will be interesting to hear Mr Subu in the con call.

yes, not able to understand. Long term call may be deferred but short term sales, how does it matter for them. Also, if this is the case , it should be for all the vendors and similar numbers should come from everyone else something not good about the statement

Even this was asked that it mean to grow at 30%. He said, his guidance is still intact as it is a temporary inventory issue. On jockey, he mentioned, he is out of contract where focus has shifted from cotton to synthetic and focusing more on inner brand business which he is trying to build. Good part is more clarity over debt-cash issue (until there is some accounting creativity, i am not aware if such creativity is possible). Just trying to keep eyes and mind open without any positive or negative bias.

Kitex manufactures garments for kids. Who in the US will stop buying a piece of cloth for his Kid irrespective - why would he hinge his buying decision on who is going to be elected? If the probable assumption is US clients are holding off on orders from India, why didnt this play out with other garment exporters. Please think and never take a promoter’s comments on face value.

Thats what keeping a close look on close competitors, if this is the case, not only childwear, this should be valid for other textile companies also like indo count, trident etc. Any idea, if any of these companies results are out or which one is most closer to track?