I have been doing some digging around to get a sense of the future growth prospects of the company (given the dramatic fall in share prices there is a case of it becoming more attractive). I have collected some facts and some of them don’t match with the information put out in the 2016AR.

Of particular note is this statement in its AR16

A casual reading of it would lead you to believe that Kitex has a 70% market share in all the imports of baby garments into US which of course is not true. I think a statement this important should be worded properly otherwise it comes across as a marketing gimmick. To me it certainly does. What they probably mean is that Kitex has 70% share in all the exports of baby garments to US from India ( more on this later). Given that that is what they mean it becomes important to understand the facts

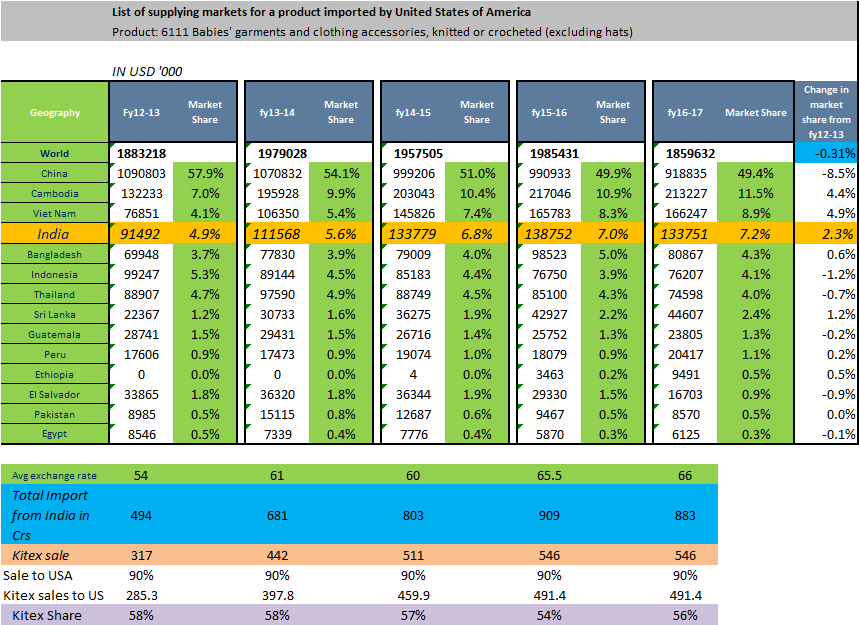

The import of baby garments into US has remained flat in the last 5 years and has reduced in the last year

Kitex report mentions that birth rates have improved but one should also realise that it is the net addition of babies that matters. Just as babies are introduced into the world babies also move out of circulation as the grow. In any case that is not translating to an increase in demand for baby garments from the US. In fact there has been a major degrowth of 6% in the total value of imports compared to the last year.

While Chinas share in total imports has reduced by 8.5% in the last 5 years it still remains a powerhouse accounting for ~50% of all imports to US.

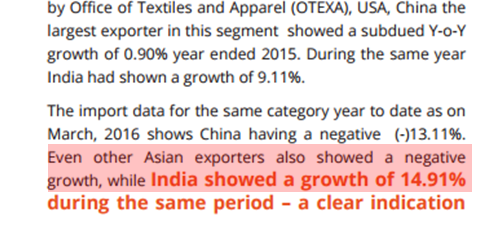

China has been losing share ( as correctly pointed out in the Kitex AR) but it still dominates the import. India has a small share of 7.2% compared to 49.4% of China. This perspective is very important. Read in this context the positive feel communicated in the AR can quickly turn negative.

Indias share in imports has grown but the share of Vietnam and Cambodia has grown the fastest in the last 5 years and their market share is more than Indias.

Cambodia accounts for 11.5% and Vietnam accounts for 8.9% compared to Indias 7.2%. Cambodia has increased its share by 4.4% and Vietnam by 4.9% compared to Indias 2.3%. The biggest beneficiary of China losing share is not India its Vietnam and Cambodia. Bangladesh just has a share of 4.3% and its share has remained stable. So viewed in this context this statement in the AR is definitely not true in my opinion.

Kitex share is not 70% and its share has remained stable since the last 5 years

As per my calculation its share is somewhere b/w 54% to 58% ( refer to pasted sheet). This of course reiterates the leadership status of Kitex but It has remained like that in the last 5 years clearly indicating that customers are sticky but are unwilling to part with a greater share of business to Kitex. China losing share and a part of it coming to India is the main reason for the growth in Kitex sales along with weakening rupee. If you look at the period between fy12-13 & fy14-15 , the indian share increased the maximum from 4.9% to 6.8% which is also the period where Kitex sales skyrocketed in the shortest time possible and the rupee went from an avg of 54 in 12-13 to 65 in 15-16. The current scenario of a strengthening rupee, China share stabilizing and Vietnam/Cambodia gaining strength doesn’t invite a growth oriented future for Kitex.

The absolute limit to market size of baby garments to US from India is 900 cr ( at the current avg exchange rate) as things stand currently

Unless there is a dramatic improvement in the US imports of baby garments OR/AND China loses even more share OR/AND other Asian countries lose share or their shares remain stable OR/AND rupee starts weakening again, the theoretical limit to the baby garment industry is ~900cr of which Kitex accounts 546 crore.

So valuation wise, at worst Kitex may enter a phase of negative growth in the future or in the most optimistic scenario growth will happen but at a very benign rate. Assigning a growth rate of more than 5% to kitex would be irrational and very optimistic in my opinion UNLESS Kitex acquires a rival/moves into a different geography/expands its product portfolio/expands domestically etc

In sum, Kitex remains a great company with super cash flows but growth prospects are not encouraging unless Kitex expands its footprint in a major way

Views Invited

Bheeshma