Any idea on the fireworks today? What has changed suddenly so as to spark such an interest in this stock?

Disc- Invested from last 6 months, @ 199. No new buying

Any idea on the fireworks today? What has changed suddenly so as to spark such an interest in this stock?

Disc- Invested from last 6 months, @ 199. No new buying

Some random newsletter has recommended the stock.

The recommendation from a newsletter is here to see.

Is it some insider information or a random talk ??

Is this newsletter available in public domain? I couldn’t find it!

This is a paid weekly newsletter by the name of “Smart Investment” and it only contained the short note for KTIL.

Any info on the q4 earnings?

link to results here:

As expected company has declared a loss at the consolidated level because of the loans taken for the Kesar Multimodal Logistics project. Income from operations for KMML has been at a modest Rs 4 cr (extrapolated from the consolidated results) as the company faced a number of problems like labour issues, delay in customs personnel being posted at at the bonded ware-house etc. It is still not clear at what capacity KMML is operating at present though scuttlebutt is that the warehousing business is getting good response.

We still need to know for how many quarters in FY16 the company had run full operations to get the full picture.

Company has borrowed around Rs 100 cr for the KMML business and the interest outgo is Rs 11.20 cr. (Interest rates are lower for loans to

agri-related warehouses). The company has valued its plant, property and assets at Rs 188 cr of which the value of KMML is around Rs 158 cr.

At the consolidated level, company has shown a small operating profit.

Implementation of GST from July 1 is expected to be a big boost for the KMML business because of its central location.

Dividend of 50 paise per share has been declared.

disclosure: holding in core portfolio.

Hello!

Other Current Liabilities is more than the total current assets. What would come under Other current liability then? Did you find out what it is?

Regards

Kesar Multimodal commences operation of ICD and Rail Transportation of Containers

we will need more clarity from the management on how much this facility can

earn in the next few quarters.

shiv kumar

I have taken full exit from Kesar Terminals and Infrastructure.

Interacting with the management of the company during the AGM really shook my confidence on the company remaining a going concern in future.

KTIL is deep in debt because of the loans taken for the Kesar Multimodal Logistics project. Everything hinged on how much and how quickly this facility could add to the top and bottomline of the company.

Chairman AS Ruia admitted at the AGM that he was unable to make any projection as to how much the company could earn during the current financial year. The project mainly depends on revenues from handling the goods rakes rather than the warehousing business. One of the speakers pointed out that KMML would earn around Rs 6 lakh per rake handled by it. Last year 90 rakes were handled by this facility.

Management could not forecast how much this would go up. Mr Ruia said the situation is very fluid at Pawarkheda. Business scenario has changed after soyabean which was produced in large quantities in MP was not moving by train. However the ban on quarrying in different parts of India has resulted in demand for sand from MP which was being sent by train. IMHO the big risk here is that environmental concerns could result in sand quarrying being halted in MP as well which would be a major setback for KMML.

Despite, the facilities being constructed more than a year ago, the management is still trying to convince customers to use the facilities at Pawarkheda. Trident was spoken of as a customer which was using the rail transport facilities. Other companies are being wooed but most are still resistant to shifting from their present arrangements.

Ruia said management rejected an offer by an international cargo carrier to turn KMML into a sole service provider for itself.

Management has shelved plans to set up a food processing park at Pawarkheda and will use this for warehousing instead. I think this is another big setback because loans are available for food processing park at lower interest rates.

Second phase of KMML has been postponed. No further progress in setting up new liquid terminal facilities in Kandla.

Meanwhile interest on debt is ballooning and the revenues and profits from the core liquid terminal business is under severe pressure due to competition. In the chairman’s speech Mr Ruia said existing clients at the liquid terminal facility were resisting price increases and were asking for price to be reduced.

This was reflected in the first quarter results announced shortly after the AGM.

Unlike in the past, the management released the results after the AGM as apparently it wanted to do control the damage. I was told by officials that the board meeting was extended and would continue post the AGM.

Meanwhile the Kilachands, the company promoters, have moved backstage leaving the management to the board of directors led by chairman A S Ruia. He admitted as much at the AGM that he was holding the fort because of his close ties with the Kilachand family. He is the oldest surviving director of Kesar Enterprises and KTIL which was demerged from the former some years ago.

None from the Kilachand family were on the dais at the AGM though Mrs Kilachand is on the board of directors. Rohan Kilachand was among the audience. He had quit as Executive Director to pursue higher studies. He is a non-executive director now.

Some of the share-holders who attended the meeting wondered whether the profits from the terminal business would suffice to pay the interest incurred on the loans to set up KMML. Some even felt that KMML may have to go in for debt restructuring.

With uncertainties mounting, I have chosen to play defensive and protect my capital. Hence the exit.

shiv kumar

Thanks for your effort in interacting with the management and detailed write-up.

To me, this is a classic story of an excellent business going wrong - in a grand way - actually.

The core KTIL business was just short of annuity business with less variables - except little bit effect of crude prices etc. Having liquid storage tanks bang on the strategical right locations (biggest port terminal) in itself is a prized trophy. In numbers, they had consistent ~25%ish ROE and tempting ~40% ROIC. Also, reasonable management with regular devidend payouts, even on bad years.

This subsidiary - Kesar Multi model - was meant to to be just another KTPL. Having composite muti model logistic hub + warehousing+ agri processing zone at the strategically positioned Powerkheda - arm length away from India’s busiest and centrally located Itharasi railway station.

What really saved me from take a leap on this company despite all those positive was a look at the books of Kesar Enterprises - parent company of KTIL and by extension of KMLL.

They had negative reserves since 2013 i.e more liability than assets. also, year on year increasing intrest burdon:

![]()

Also, reading through Aegis AR helped understand the nuance of liquid storage business.

Disc: No investment ever in either Kesar Enterprises or KTPL

Tarun

Adding to the list of things going wrong in a grand way- the management was hoping that when Powerkheda was up and running, Railways would shut down the use of Itarsi for cargo purposes atleast. They were hoping to have achieved this 12 months ago. However the Railways have not even begun tapering off the traffic via Itarsi let alone shut it down. That is another reason why the 400 rakes that they should achieve for break-even seems like a daunting task now.

Hi Shivkumar… Tks to your note… I was watching this counter for a long

time, but hesitant to invest. Ur note sealed my decision

Very interesting points being mentioned / covered by fellow members (after reading it, my first thought was, I also should have sold my holdings), though I have a slightly different point of view (I would love, to be wrong here) :

Just a flashback, bought in 2012 at a price of approx. Rs 34 after split.

It was a one of the most risky investment for me at that time, with a very small business history after the demerger from the parent company.

My thought process was :

a) The tank division is doing good & hopefully should do good. A cash cow kind of situation.

b) KMML might be a drag on the business (this is happening), as Govt backed projects (with both MP Govt & Railways involved) take their own sweet time to perform. Only thing I liked about it was a the location, which is still one of the best (my opinion).

Current situation (only taking the points mentioned by respected members):

a) Debt : Yes the situation is not good or favourable. Can the company clear off debts with current cash flows, I think so but this would have impact on profitability.

b) Increasing business : Management agrees customers are resistant (good thing is management is acknowledging the problem & am sure they are working on it). Am not sure why the mgmt. decided to reject the offer by an Intl Cargo carrier (may be the payout was not good, or the terms & conditions were not favourable). This also means mgmt. is still confident on the business & the visibility to get it on track may be longer.

c) Expansion : With these kind of situation mentioned in earlier points, any sensible mgmt. would postpone the second phase.

d) Price inc. for tanking business : This is definitely a concern. But, I think KTIL still enjoys a upper hand here.

e) Management : One of the fellow member questioned on the quality of the mgmt., I think the business segment of Kesar Enterprise is, a lousy business in itself, even the best of mgmt. would have found it hard to manage it.

My present take : I agree there are headwinds in the business. My original thought process was to offload my stake after 240, as the price started to reach there in last few weeks, I did a recheck on my investment thesis & I personally think there is still steam left in it. From the current level I can still generate 1 or 1.5 times on my investment. I just tried to have a different point of view.

Would like to have thoughts of the fellow members.

Disc - Invested & holding (would increase, at a bargain).

Here is my thought process on KTIL on investing at the current price.

At current price of 170s KTIL is trading at 11X the stand-alone earnings which is a reasonable valuation for a company without any expansion and only nominal increase in revenue due to nominal price hikes due to inflation

Campany can earn cash profit of anywhere between 17 to 20cr per year. 18Cr is a reasonable number to assume.

Time investment and opportunity in the new business is not reflecting in the current price.

Now the question has been, How good is the new business?

As per the FY17 Account, KMLL did revenue of 4.2Cr

All the expenses except Finance cost and Depreciation is 8Cr. That means it had a cash loss of 3.8Cr without finance cost

With finance cost of 11.15Cr on debt of around 95cr ( back calculated interest rate is 11.7%) total cash loss was 14.95

Total net loss including the depreciation (7.9cr) is 22.8cr

As depreciation is only asset loss, not a cash loss, KMLL cash loss of 14.95cr can be easily compensated from cash profits of Standalone KTIL.

All this is the story of FY17 numbers. 4Cr revenue is only the few months business of FY17.

Even if KMLL did a revenue of 12 to 15cr its cash loss can come down

So we can easily conclude that Consolidated KTIL is not going to sink in debt burden due to Strong biz from the Standalone KTIL.

Questions:

Disclosure:

Not invested.

Cash flows need to be strong enough to support Principal + Interest payments. One cannot ignore principal and look at interest cost alone. Debt is not for perpetuity (unless it is ! ).

Also, you need to have a reasonable estimate for maintenance capex before ignoring depreciation. If no estimate is available, you have to retain depreciation too in the calculation.

(Disc: No exposure)

you have to look at the consolidated figures. company has taken huge loans

for the KMML business at Pawarkheda, MP and it is not able to get enough

business to even cover its costs.

now even the standalone terminal business is facing degrowth, so the

company would be in real trouble.

disclosure: I have taken full exit after the last AGM where the management

indicated that things are really bad.

Above is an extract of Ashish Chugh interview to a magazine.

When I read this, the stock got into my mind is “KTIL”

It’s true that every business have to be self-sustainable with its own cash generation, its also true that business needs some time to break even.

In case of KMLL Break even looks difficult only because of debt cost. Suppose if it is built with own capital it could have broke-even easily.

Also, it is easy to broke even for the business like KMLL as they have very low operating cost so have high EBITA margins.

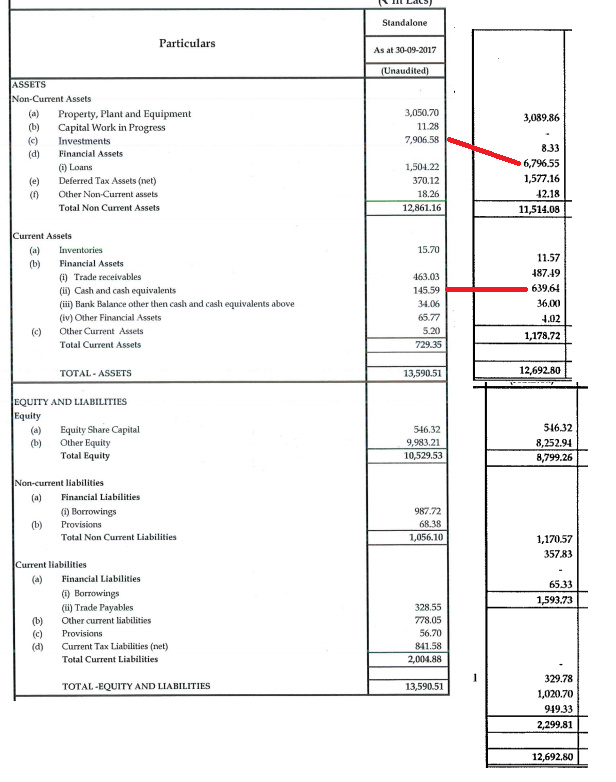

Though KMLL struggles in short term, it will have support from Standalone business of KTLL and it is evident if you compare stand-alone balance sheets for March17 and September17

KTIL is shifting its profits and existing cash to Investments (probably to KMLL)

Disc: Not Invested

you are right. but the core liquid terminal business is facing tough competition from other operators at Kandla and the company has been forced to reduce prices. more over the profits from the terminal business is not sufficient to cover payment of interest for KMML as well.