The business is dumb enough even for an idiot to run it. Having said that, I would love the market to misprice Kesar in the coming days on the downside.

S.I

The business is dumb enough even for an idiot to run it. Having said that, I would love the market to misprice Kesar in the coming days on the downside.

S.I

A S Ruia resigned as director of Kesar Enterprises - from which Kesar Terminals was spun off some years ago - wef April 29, 2016 citing work pressures. He simultaneously took over as chairman Kesar Terminals and KMML. Disclosures by Kesar Enterprises show that A S Ruia has been on its board since 1985 Appears to be some kind of restructuring among promoters is going on.

Talking about management I had raised a question few months back Could anyone clear that doubt

I have been trying to find the background of the promoters and the nameKilachand is also associated with the infamous group which are promoters of companyâs like Polychem,Synthetics and Chemicals andGujarat Poly AVX Electronics. The office of this Kilachand is just one floor below the office given by Kesar EnterprisesOriental House, 5th Floor, 7 Jamshedji Tata Road,Churchgate Reclamation,Mumbai, Maharashtra - 400020 is for polychem Kilachand while the Kesar groups address is Oriental House, 6th Floor, 7 Jamshedji Tata Road,Churchgate Reclamation,Mumbai, Maharashtra â 400020.

I am not able to connect the dots how are these two related? My guess are they are brothers

Also has anyone done some calculation on impact of KMLL on profitability because debt will also increase drastically. My estimated guess is return ratios will fall rather than rise for next few years.

Besides aren’t people worried about core business slowing down drastically?

Besides the 1st doubt, I believe rest is already discussed.

Core business is running near optimum capacity. So its numbers are steady more or less. And most people have based their investment thesis on KMLL’s expected earnings.

Most of the interest payment is expected to be covered by earnings from PFT, so we get much of the earnings from warehousing project for free.

Ratios may suffer shortly but in the longer run they probably will maintain them.

The Kilachands were promoters of Polychem Synthetics and Chemicals which was totally wiped out when Reliance Industries entered the market.

From the 2014-15 Annual Report: Is this something of concern? What if they cannot renew the lease for Kandla Port land?

Pursuant to Scheme of Demerger, the Company has requested Kandla Port Trust (KPT) for transfer of leasehold land situated at Kandla in its name which is presently in the name of Kesar Enterprises Ltd. However, KPT has raised a demand of `208,354,295/- on account of such transfer/ upfront fee for change in the name. The Company has filed a writ petition in High Court of Ahmedabad, against the demand raised by the KPT. The Company is of the view that the demand raised is likely to be deleted or substantially reduced and hence no provision made. The Depreciation on Assets constructed at lease hold land of KPT has been charged as per the rates prescribed in Schedule II of the Companies Act 2013. However for certain portion of leasehold land, where the lease period has been expired, the same is pending for renewal, although the Company has filed an application for the renewal of the said lease. The Company is of the view that Lease shall be renewed on the outcome of the writ petition filed in High Court of Ahmedabad

There are two issues you mentioned in your post. My understanding of these is as follows.

First issue being the huge charges for lease name change. In worst case scenario, court will order against the company and the company has the option to continue the lease in the name of KEL.

Second issue where renewal has not happened for a certain part of land. I couldn’t see any impact on company financials in FY 2016. So either it is not that significant or the case has been resolved.

Need to get updates from management about the case though.

Will be interesting to see what KTIL is able to post in Q4.

They would have had about 1 month of initial KMLL earnings in Q4.

I believe KMLL operations started in April. So not expecting any improvements in earnings. Shall be clear on 30th May.

KTIL has announced its results.

Officially, Kesar Multimodal Logistics ops have begun wef April 16 this year. So interest liability will kick in from Q1FY 17.

Tax write back has helped shore up standalone results though the liquid terminal business remains strong.

Company to hold another board meeting to discuss issue of bonus shares.

disclosure: holding in core portfolio.

I believe most things are as expected in the results. Predictability of this kind gives a lot of comfort.

Also I’m not too sure what to feel about the bonus shares. I would have probably kept it less liquid until KMLL earnings started to kick in.

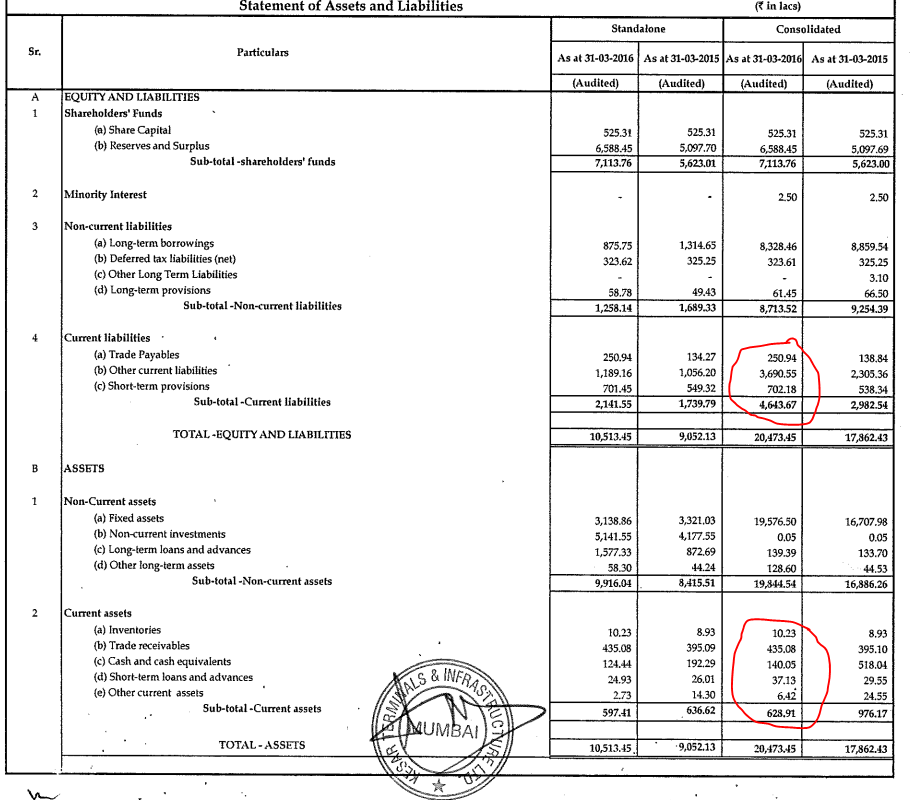

Query on Balance sheet - current assets and liabilities for FY15-16

How do the company survive or meet the current liabilities (4644 Lakhs) which are very high than the current assests (629Lakhs). This is also same for FY14-15 (2983 Lakhs vs 976 Lakhs).

How do v have to see/analyse this situation:

Regards

Hello senior boarders, Is there any way to track how KMML is doing ? who are their customers presently and how is the revamp happening ?

http://www.bseindia.com/corporates/anndet_new.aspx?newsid=d7c1577b-fd46-44c5-9eef-73d954854e8d

Markets seem to love any possibility of a bonus issue!

Yaaahh!! Finally !! This is not a fundamental news, though I feel now the stock will have momentum. Liquidity will increase and might interest MF/DII/FII to invest in the story. Lets see and hope positive.

Bonus is to the tune of 1 share for 25 shares held.

I think the next trigger is left on Q1 results as bonus news is disappointing.

Board of directors to now consider a stock split on July 1

http://www.bseindia.com/corporates/anndet_new.aspx?newsid=74fb5960-34c7-4334-8edf-a64268e4d7d9

A bonus announcement followed by a potential stock split in less than a week. Even though the bonus issue will not lead to much equity expansion (although % ownership remains the same), the objective of these moves just seems to be increasing the market cap on the stock exchange by playing to the retail investors.

Is it just me or the promoter actions should actually worry the minority investors?

Is it a wrong thing…???

He is not doing anything even bordering on unethical. It’s a common knowledge that bonuses and splits only increase liquidity, and have no effect on any valuations of the company. And to an extent an argument can be made, the liquidity of shares is an issue in Kesar. If there actions decreases volatility in the future, then why not.

Disc. Invested. Less than 3% of pf

I didn’t mention it but anyway agree with you - nothing unethical about it.

Just wanted to raise any potential concerns because of this - guess not