The one mid-cap stock that appears simply waiting to graduate to the next league is Kesar Petroproducts. The pigments company comes from a background I can only describe as “romantic”.

Loss-making and a BIFR case and acquired by a new management. Bankers place restrictions on BIFR companies; you cannot borrow afresh; you can only grow through accruals. In Kesar’s case, the result was that the problem of a loss-making environment was replaced by the challenge of low capacity utilisation (usually accompanied by losses, as companies find it difficult to cover fixed costs).

This is where the Kesar Petro story becomes compelling. The company, restricted by inadequate throughput, selected to strengthen its once-foundering business through alternative routes: A wider portfolio of value-added downstream products and disciplined accruals’ deployment into capacity expansion.

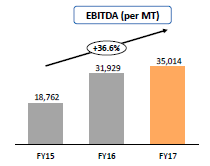

Normally, this restriction would have been limiting but Kesar Petro transformed this into a competitive advantage: Over the five quarters ended June 2017, revenue increased Rs 1.5 crore, while pre-tax profit increased a little more than Rs 3 crore; Ebitda (earnings before interest, tax, depreciation and amortisation) margin strengthened from 18 per cent to 24 per cent.

This is where the story gets interesting. Not being able to borrow afresh means the company has no debt; it reported more than Rs 10 crore in cash profit in the first quarter and after paying moderate tax (20 per cent rate), finished with a post-tax profit of Rs 8.03 crore (on only Rs 42 crore revenue, never forget).

This excitement generated from quarterly results is only a trailer of what could be coming. At Kesar Petroproducts, we believe the foundation of all enduring sustainability is essentially derived from the ability to commission additional capacity at a cost considerably lower than the prevailing capital cost per tonne. In January, Kesar commissioned a 300-tpm (tonnes per month) beta facility (engaged in value addition) in eight months, against a benchmark of 18 months.

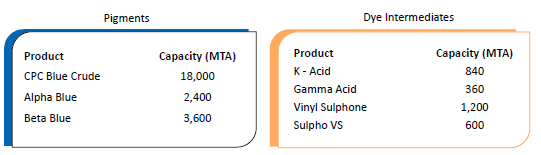

During the current year, the company debottlenecked its alpha blue capacity, from 80 tpm to 125 tpm, again through accruals. These initiatives indicate the proportion of revenue being derived from CPC (of which the company accounts for eight per cent global capacity) could decline, strengthening its margins.

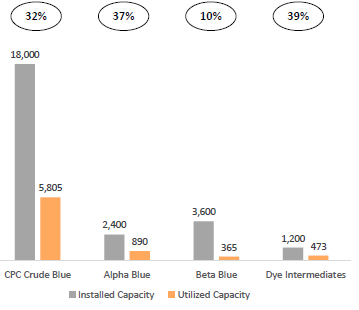

As more cash is generated, the next round of deployment could be where the company needs it most, working capital. What it has achieved in terms of manufacturing throughput until now has been on the basis of less than 40 per cent capacity utilization.

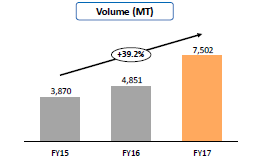

A company generating quarterly revenue of Rs 42 crore possesses the potential of rising to more than Rs 150 crore in quarterly revenues. Which means what it is doing for a full year today is what it should be doing in a single quarter in about three years (my estimate).

Kesar petrproducts is Future Ready

-

Economies of Scale:

Geared to improve utilization levels resulting in better operating leverage -

High Margin Products:

Focus on increasing the mix of high value products like Alpha Blue & Beta Blue Pigments -

Product Innovation:

Continuous Product Innovation through use of Technology and by way of Backward / Forward Integration -

High Entry Barrier Business:

Intensive Environmental Regulations, High Water Requirements, difficulty in Obtaining New Licenses and Client Stickiness -

Growing Export Opportunities:

Growth in the Pigment Industry and the continued dominance of Indian Players in Pigments such as Blue and Green

That is why I would buy into this pigment company and whistle through my morning jog from now on.

Originally authored by Mudar Patherya.

Any thoughts / feedback / suggestions ?

Disclosure: Invested recently!!