Thanks for sharing. Ever since i came across you’re thread i have been tracking this stock as the TCAS story seems very interesting and nothing is priced in yet which gives the margin of safety. I had a couple of questions and was wondering if you may have the answers:

1.) FY17-18 sales was expected to be around 25cr if i am not mistaken. 9M sales is ~9cr. was wondering if you expect the remainder in 4Q ?

2.) Have you found out when will its Safety Certification and other necessary certifications which are required to begin execution of orders begin ?

Could someone share information about other participants in the train safety business?

In Europe, Siemens has an extensive portfolio of train safety systems. Isn’t it possible some of these foreign companies will receive orders? Is the technology possessed by Kernex its intellectual property?

In the year ending March 2013, on a sales turnover of around 28 chores they had an employee expense of 7.81 crores, which is around 28 percent.

However, in 2017 employee expense has jumped to nearly 45 percent of sales turnover. Despite anemic growth in sales their employee expense has grown significantly.

Could someone please explain why this could be happening?

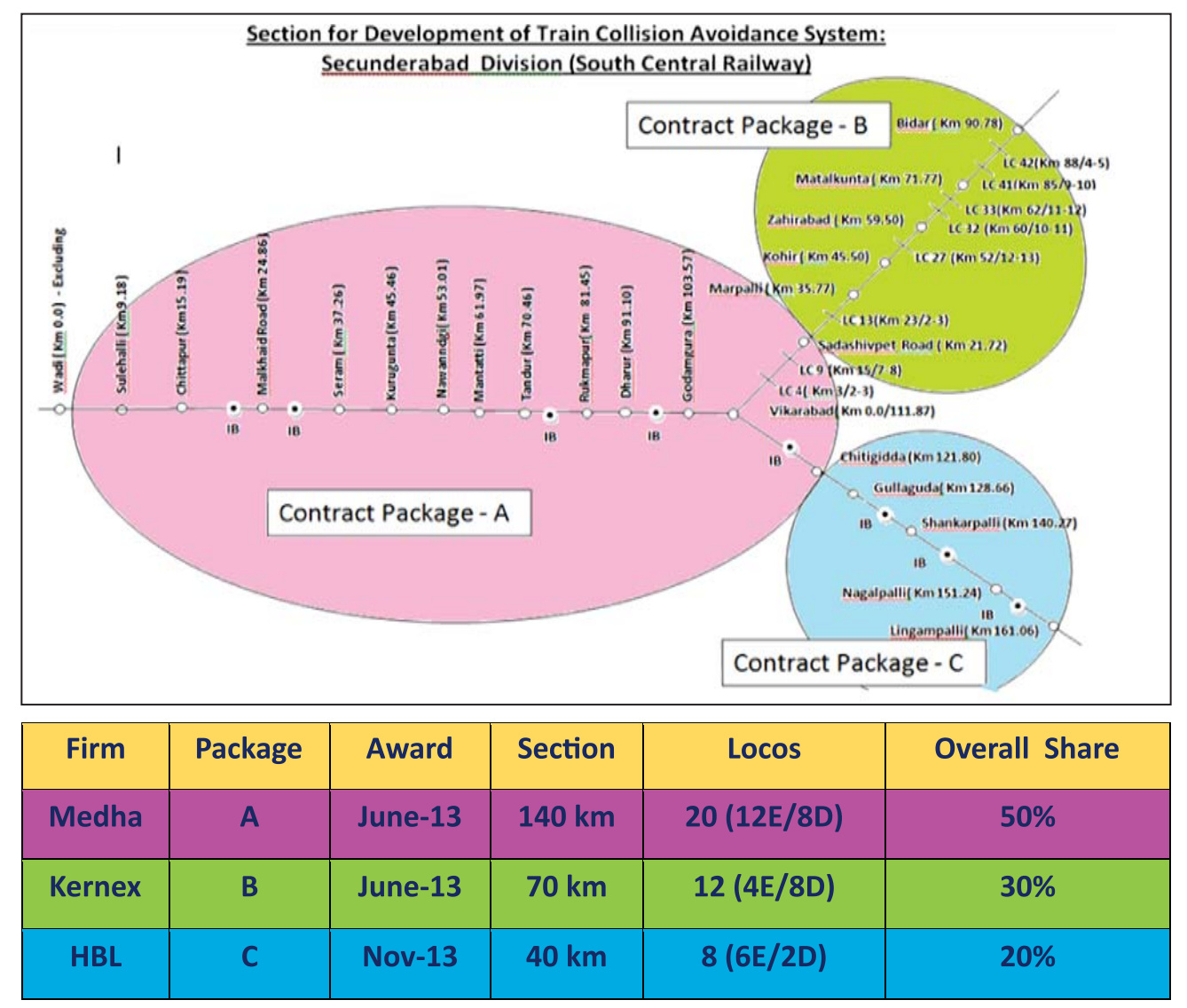

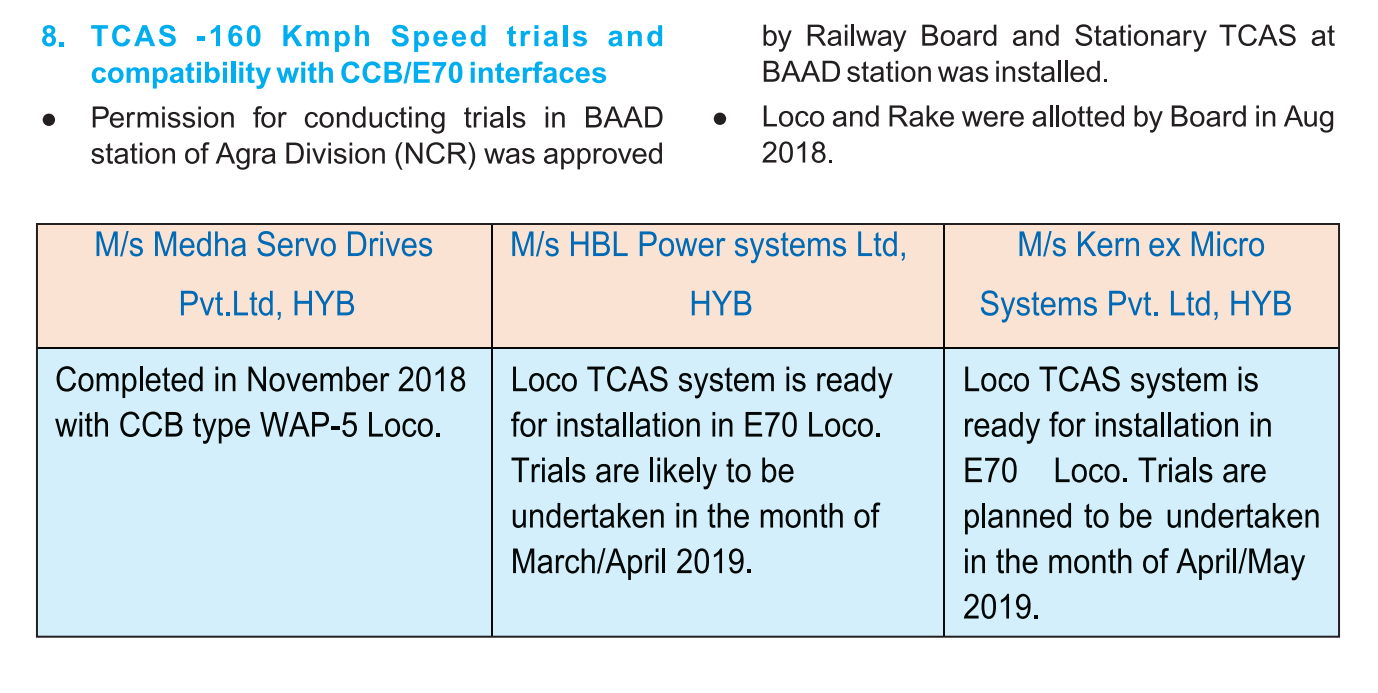

Medha Servo, Kernex and HBL are selected for the TCAS project out of multiple contenders. You can go through the entire thread to find out. Employee expense has risen most likely due to the need, development and extensive trials of TCAS.

This means orders should start flowing in post 2019 and pick up quick pace post that? I think a prudent time to take a starter position would be post the approvals (SEP 18 end as stated by mgmt)

Thoughts on the way forward from senior members tracking the story please?

Hearing few buyers interested in their Yadagiriutta Land Parcel of more than 250 acres which can fetch them roughly 25 crs .

They executed very small defense order of 1.5 crs.

As per my interaction with RDSO people Kernex will be getting SIL-4 Certification by Dec end & main game changer for them is TCAS only

So Kernex in only for investors who can wait patiently as these government orders do take time .

SIL-4 certification they will definitely get as there is no question of rejection & company just have to incorporate necessary changes/suggestions suggested by Italian agency granting SIL-4 certificates.

Previously, very few TCAS (train collision advance system) and TMS (train management system) solutions were being implemented by Indian Railways, and they were majorly imported. Now, the government has decided to encourage domestic industries

Margins in TCAS and TMS businesses are lucrative and the company is not going to bid for any orders with less than 20% Ebidta.

The company is expecting Rs 150-200 crore turnover from TCAS and TMS solutions in FY20 with 20 per cent Ebidta margins on a conservative basis (which forms almost 70% of entire net profit of FY18).

The TCAS and TMS turnover is likely to touch Rs 200 crore in FY20. The company is confident that there is huge potential in that vertical and double that revenue from that division for every year for next 2 to 3 years. The problem is that delivery should be faster

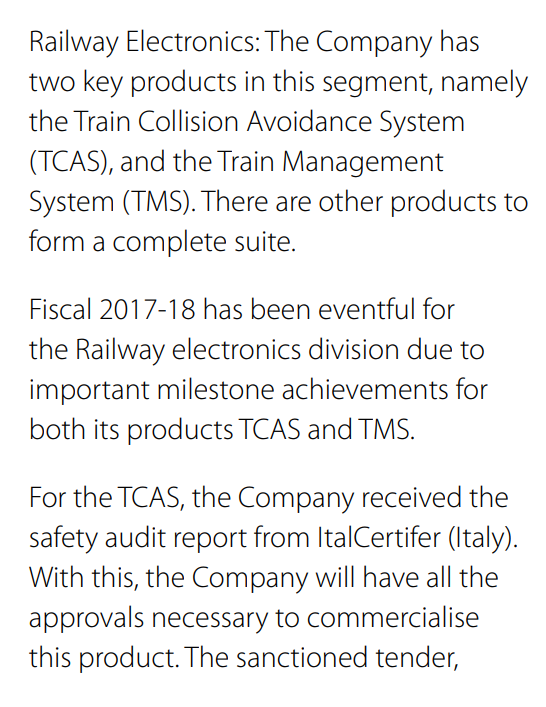

For the TCAS, the company received the safety audit report from ItalCertifer (Italy). With this, the company will have all the approvals necessary to commercialise this product there. Promoter said this certification adds credibility though the market in Italy is very small compared to India and is very confident in capturing Indian market.

Q3 FY19 results are out! Exceptional item of 9.4cr as sale of land. Only profit is shown in PnL, so actual amount of land sold would be its book value (BS) + 9.4cr