Target EBITDA margin at 16 percent, profit after tax (PAT) margins at 10-11 percent in three years.

So, this digital transformation shtick isn’t really a high margin business?

Target EBITDA margin at 16 percent, profit after tax (PAT) margins at 10-11 percent in three years.

So, this digital transformation shtick isn’t really a high margin business?

atleast in case of Kellton it isnt

Dear Members - Stable Q317 Financials make the stk at consolidated 12.61 PE vs 18 Industry.

My concern was sticky NP Margins for past 4 years. was tracking its since the overenthused management crashed the stock. but 9% uptick on Friday got me interested.

Disc:Not Invested but aiming at 3% of portfolio on Monday.

Many other small to medium software cos have <10% PAT margins. E.g. Polaris consulting, Virinchi, Datamatics Global etc. Larger players and brands can attract engineers at lower salaries. Smaller players need to pay more to attract talent. Having said that, they need to look at ways to improve margins for sure.

Received as Whatsapp forward ----

EQUITY KING VIVEK JOSHI, [17.02.17 10:10]

Kellton Tech- INFINITE POSSIBILITIES

Why KELLTON TECH MUST be in my portfolio?

Ranked 19th on Deloitte Technology Fast 50 India, a ranking of 50 fastest growing technology companies in India. ONLY, yes ONLY, LISTED Co. to be in this list.

The company furnishes top notch IT solution, consultancy & development in SMAC- Social, Mobile, Analytics & Cloud, Business Process Management, Artificial Intelligence (AI), ERP & Internet of Things (IoT) which are the next generation space, the future of mankind! The growth in above digital space will accelerate at mind boggling pace with increased technology penetration in India as well abroad, opening

major doors of business for KELLTON TECH.

Management is conservative and is systematically acquiring tech companies, leading to huge growth in top as well bottom line. In fact, in very short time frame of 3 months, KELLTON TECH has acquired not only one or two but EIGHT (8) major new clients.

The current Trailing Twelve Month(TTM) Revenues stand at ₹594 crores. The company is planning for ₹ 2000 crores revenues by 2021 with aid of many recently acquired and to be acquired subsidiary companies. Hefty 3x increase in revenues and profits can be seen on cards in near future as per management.

The company has already bagged in its portfolio, by providing world class services to, giants like PayTM,Makemytrip, Nokia, PVR, Educomp, Nielsen, Upay, Discovery and many more proving it’s mettle in the industry.

FII do hold 3.42% of total stake amounting to 16,09,645 shares in KELLTON TECH.

“Kellton Tech has been very good at letting us know what we can and cannot do and in working through changes with us.”-Deputy Director, NASSCOM. Succinctly explained business working culture. Need not comment further over service quality. 8. NET PROFITS in EVERY QUARTER, I repeat, EVERY QUARTER is greater than the previous one. In the last 13 quarters, EVERY QUARTER profits have increased indicating it has come out as winning player overpowering cut throat competition.

Quarter Profit

Dec 13- ₹1.22 crores

Mar 14- ₹1.49 crores

June 14- ₹2.52 crores

Sep 14- ₹3.13 crores

Dec 14- ₹4.85 crores

Mar 15- ₹5.50 crores

Jun 15- ₹8.59 crores

Sep 15- ₹9.57 crores

Dec 15- ₹10.12 crores

Mar 16- ₹11.28 crores

Jun 16- ₹12.20 crores

Sept 16- ₹13.28 crores

Dec 16- ₹13.96 crores

Truly a MULTIBAGGER!

Always yours,

EQUITY KING VIVEK JOSHI

---- Nice Marketing strategy…

Deloitte 50 is a joke. Start from 2006.check the list n see what happened to many of them. Can name many of them.

Stating the obvious here.

Low margins on short contracts–>Sketchy FCF & Severe dependence on Revenue Growth.

Kellton’s Inorganic Growth Strategy–>Difficult to fund them through internal accruals (again, because of low margins)—>Take on debt or dilute equity

One bad acquisition–>Story over.

Disclosure: Invested

Its all about demand-supply gap. The area in which they operate is high in demand and quality and experience players are very less. Looking at the growth of technology led value addition in various industries, I don’t see dearth of clients and new projects. It will all boil down to their marketing and sales ability. From the expertise point of view they seem to have an edge. But experts on these tech are less and hence salaries are higher. The bigger they become cost should come down. But it might take some time.

My hypothesis for holding on through severe decline in share price was it’s only a matter of time before the EBITDA margins shot up over 20%. The assumption was “in-demand niche with not many competitors = high margins till competition starts eating it away”. Now that the management says it will only be 16% in 3 years, I’m having to question my hypothesis.

I suppose Kellton’s competition is mostly from the unlisted companies and startups. Kellton has had an early mover advantage, whether that has rendered them any significant edge in expertise is debatable.

If kellton already has an edge, why hire aggressively and make acquisitions to fill the technological gaps?

On the other hand, the high profile clients they serve/have served can be held up as an indication of an expertise edge. It’s difficult to say what aspects of digital transformation of these clients were performed by Kellton. I doubt those high profile clients would let Kellton handle all the aspects of their digital transformation.

What if the aspects of digital transformation Kellton has expertise in are inherently low margin? Is the aggressive hiring to move up to high margin aspects?

I may be wrong, but it seems far too difficult for a single company to have an expertise in all of I,S,M,A,C & I’ve serious doubts whether any number of acquisitions can strategically address this difficulty.

We also have to consider people like Nilesh Shah (of Kotak AMC) saying the companies which are bound to do well are SMAC product companies, not SMAC service companies. Going forward, it’s not difficult to see different SMAC products serving different Industries because developing those products will require the domain knowledge of the Industry the product is meant for. It can’t be a one company/single product/single service-fits-all.

So which companies does Nilesh Shah suggest in SMAC product domain ?

Obviously, he didn’t mention any companies.

Focus is on companies with SMAC products rather than services & those that are streamlining operations.

The question that begs to be asked in this thread is, Which industries are Kellton good at serving?

They seem to have clients across several industries.

Q3FY17 Concall Notes:

Any impact on the wage bill due to the change in H1B Bill will be passed on to the customers.

Sales and operations staff in Ireland has been built up. Expect orders from Europe from the next quarter. Hope to achieve 20% revenue from Europe in the future to reduce dependence on US.

Pledging of shares by promoters for working capital requirements of the company. Don’t expect further pledging.

A Project is classified as digital when a minimum of 3 of the 5 technologies in the ISMAC stack are being used for project execution. If not, then it’s classified as an enterprise project. Also foraying into blockchain and AI.

Our digital txfn solutions are Industry agnostic - A vertical play, not horizontal.

80% of orders from repeat customers. Hope to partner with clients on the digital side for a long time.

Acquisitions will be funded through debt because it’s cheaper ~ 5%. Aim to keep the D/E ratio at around 0.5.

There will be a $15-20 Million QIP in the future, but the timing depends on when the headwinds for IT goes away.

The target company should have a revenue between $5-50 million. We don’t look at companies which have a revenue greater than $50 million. An acquired company is completely integrated within 180 days.

Target a conservative 20% Organic growth because of the higher base.

Margins on enterprise work is lower, but agree to those projects if there is a potential of larger digital work from the client & their industry peers.

Further implementation of mSehat depends on the UP Election results. WHO is interested in taking it to other places.

Billing rate depends on the type of work. Average billing rate is around $88/hr for onsite work. Digital transformation billing rate is $180/hr, but the expenses are also higher.

No currency hedging has been done - a significant expense in US is also in USD. Also, the debt raised in India in USD becomes a natural hedge.

New client - a large bank with presence in 23 US states: Could turn out to be a multi-million contract over the next few years. Presently, on average it tends to be a $800k-900k contract.

Globally, majority of the IT budget of companies being assigned for their digtal txfn. Digital Txfn results in significant savings for the clients. e.g, No need to spend millions to set up a data center, just put it in the cloud by using Amazon and pay as you go.

Spending by Govt & the Private Sector in India on the digital side is growing exponentially.

Dividends might be given out only in 2020-2021 because that’s when the company is expected to be in a steady state growth state.

Disclosure: Invested

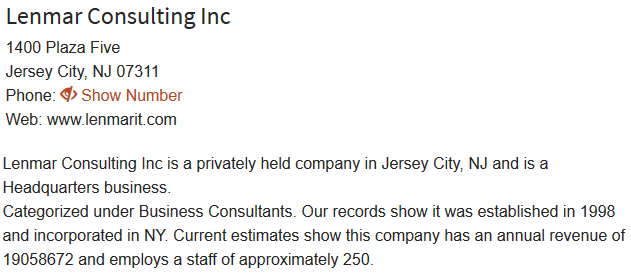

From - Kellton Tech Media Team

http://www.kelltontech.com/kellton-tech-acquires-lenmar-group-strengthens-its-position-bfsi

http://www.manta.com/c/mmsmcsy/lenmar-consulting-inc

The value of the deal has not been disclosed. Hope they have not paid too much.

With the above details if we take revenues of Lenmar at 17 million USD… which works out to be 110 crores.

Hence, Kellton annual revenues for FY17 will be around 600-650 cr.

As per the above Lenmar revenues, the acquistion will not be adding too much to the topline. Mostly, kellton expects more client addition and expect more contract renewals going forward !!!

Hope it deliveres.

The New Moats: Why Systems of Intelligence are the Next Defensible Business Model for the tech companies.

https://news.greylock.com/the-new-moats-53f61aeac2d9

(H/T Value Investing World)

Hi Rajeev, so as per the article, SMAC services providers(or companies which focus on adding intelligence via AI and analytics) stand to gain in the coming future, then Kellton is in the right space.

But the question is why the website or ARs don’t talk about its AI capability? I doubt if they are on the look out for AI companies as they rely very much on the existing infrastructure of IBM Watson. And even if they utilize analytics in a particular project, since the service is sourced from another entity(IBM) there isn’t a great value addition individually from Kellton. Probably this is the reason for margins not improving over many quarters. Invite fellow investors’ views to understand the situation better.

Disc: Invested

In the last concall, they mentioned they are foraying into AI and blockchain.

Going by what’s mentioned on their website,

Their AI services seem to be geared towards Retail/B2C Businesses. Only one of those services use IBM Watson.

For analytics, they use Hadoop MapReduce, Cloudera, HortonWorks; Hive; Tableau, Splunk.

The value addition comes from how these tools and technologies are exploited to fulfill the client’s digital transformation needs. How good kellton really is at these technologies is difficult to answer. (The IT Companies tend to show off their capabilities through their blog. Kellton’s blog is filled with numerous technical posts on Drupal modules, and mostly non-technical, generic ‘why digital transformation is good’ kind of posts. I would like to see a few ‘technical’ posts on the ISMAC stack.)

The low margins may be a function of

aggressive hiring (as argued by @vibs6615) & a dearth of talent with skills in digital technologies.

From the concall - “Margins on enterprise work is lower, but agree to those projects if there is a potential of larger digital work from the client & their industry peers.”

The actual investment risk arises from the acquisition fueled growth. The high profile clients give some bit of comfort. We just have to wait and see if the management walks the talk, and more importantly, if the pick up in the US Economy is for real.

Disclosure: Invested.

Did anyone attend the conference call? Can you please share the highlights of it?

While the P & L continues to grow, the balance sheet throws up some questions:

Debt is ~ 100 Cr used to fund acquisitions, but there is receivables of ~ 146 crores. So why go in for long term borrowings? the receivables should be good enough to help go debt free.

Very high goodwill. If the net profit margins are only 10%, is the company overpaying for its acquisitions? usually Kellton doesn’t reveal the cost of acquisitions.

If the SMAC space is so hot and in demand, the margins should be higher. 8K nets about 20%. 10% tells me that the company doesn’t have strong purchasing power.

The QIP if I remember correctly was to be for US $ 3-4 Mn. Does the company not have this level of cash?

Promoter pledge doubled. Although the overall level is still ok, it tells me that the company is cash starved.

Invite others’ thoughts.

Q4FY17 Concall Notes:

Disclosure: Invested.