my bad - checked bse site (screener is not updated yet) - there is one on 4th december 11 am. Will surely attend.

Con call:

Due sharp rise in intl coal prices, bottom line of the power unit has been hit. Performance of the unit continues to do well. It is input cost that is the issue and that is out of mgmts control.

38cr dividend is from vietnam sugar unit. there is capex needed of around 70cr to move from 8k-10k tons over the next one year.

Peak debt will be around 500cr for the company, post which it will begin to taper off.

Demand situation continues to be strong.

Impact of any slowdown in amaravati wont affect new capacity utilisation as there are unexplored areas and markets for the company anyway. Amaravati will increase inflow of certain govt orders thats it.

No plans to demerge/exit hotel business. Engineering business to break even at 85cr. Current order book is around 100cr. These two businesses continue to be a drag on the company.

My understanding is that the company should grow earnings rapidly if there is no unforseen macro event.

Demand in vietnam seems strong. Demand for cement seems adequate. Mgmt seems strong. All in all a good story. We will have to wait and watch as execution plays out.

5 Likes

Construction activity in Hyderabad has picked up a very good pace. The entire road between Kphb to Biodiversity park (where the road passes through Hi-Tech city) has seen a sudden spurt of construction activity. That is lot of prime real-estate left untouched for at least a decade after Hitech city came up. All of a sudden heavy construction is happening there.

With several under-ground passes and flyovers under construction, I noticed a lot of activity in the areas I commute.

While Amaravati might take time, a city is going to come up and that is lot of construction. The high real-estate prices and construction activity will only continue and go up.

Disclosure: Invested based on https://dolly-bestpicks.blogspot.in/2017/06/kcp-limited-old-is-gold.html

1 Like

Dear 1.5cr

I found your analysis interesting, though I dont know how it will reach 300 cr Pat in 3 years. Assuming 10% nett profit after taxes (which is high anyways) the topline has to grow to 3000 cr. Tall claim for this company.

Disclaimer - KCP is the largest component of my portolio, holding since 2001.

Not sure if that is the real dolly khanna behind the blog.

Thanks for the input, naruto! I don’t mean to discard your thoughts but if the construction activity has picked up and it can be seen on the grounds then we should be seeing some strong growth coming in from KCP. As I understand, the company is not projecting/expecting such a high demand coming in from government sector which is surprising because if the situations are the way we are perceiving them to be then company would give really strong projections and expectations for the growth in demand which is not the case. Please correct me if I am wrong.

One strong point in favor of the bullish story of this stock is that FII/MFs/Institutional investment has increased significantly in this stock.

Disc : Invested heavily

I had asked mgmt. regarding the dependancy on amarvati for new capacity. They said they have many unexplored channels and their capacity will be well utilised. They arent too bothered about amaravti. If construction picks up they will get a few govt. orders. This is wonderful because naturally margins are higher on the retail side than govt contracts. Market will also assume that demand is coming from govt. and this will further boost the interest in the company, when in reality majority of sales will come via other channels. I was hesitant to increase holding due to this amaravati and govt issue. But now that that has been clarified this is a further buy for me and will form 20-25% of my portfolio going forward.

1 Like

My 2 cents on new capital…

Regarding the new Capital “AMARAVATI” - it may take years if not couple of decades to built a brand new greenfield city. Presently things r moving/going since the last 4 years after the state is devided and will go on, only the Govt and it’s burocracy needs new buildings and setup, anyhow people also struggle but keeps moving on…

In between, if the Govt changes after 5 years then things changes dramatically with new ideas and as usual everything starts …once again

I am sure the companies and their strategies r not depending on the new city for their sales if it comes they take it with both hands.

Hi @rbhutoria

With regards to the valuation of cement business,I don’t understand the 70$ /ton & 1900 crores you have mentioned

EV per ton…Its a valuation metric for cement companies based on capacity…

1 Like

This suggests that for at least 2years or so we can not expect Amravati demand to rise.

Thanks for the clarification. Yes, you are right in that the company seems

to be a good buy even without the Amravati story being realized. Overall, I

like cement sector and KCP seems to be a good buy in it.

Disc : I am heavily invested in KCP with long term persepective

For the people who has doubts on @ Amaravathi, Please watch the video. Amaravathi is at an inflection point…

During my recent visit to AP, I have seen G+3 houses… these are being developed in large scale and look very good… unable to take pics… shall post them next time.

1 Like

Correct - so this is in line with what was discussed on con calls of sagar and dalmia as well…major push is coming from low cost housing.I am hoping others will start soon…

Being an investor in the company, this is definitely good to know! The only

reason why I have doubts is that if so much construction has been going on

then why aren’t we seeing extra jump in revenue? In other case, if

construction is about to start on large scale then why isn’t company not

talking about it in the conferences and reports. Generally, company would

give guidance and would happily mention such potential growths in revenue!

I think being conservative isnt unfortunate.It is difficult to find such companies.This is one of the biggest reason for my investment.Ideally companies should work on making their business strong and not worried too much about marketing.However, I do believe they need not market themselves but be more vocal about what they are doing - to bring more transparency to share holders.If we see cement business overshadowing others - there is a high probability of demerger and hence value unlocking - but again thats on a long run.

Here are the latest pics of Polavaram project. One of the largest irrigation project of India. Though the Central Govt. is doing its level best to stop the project for political reasons… the work is going on at a brisk pace. Concrete work is going on… This project alone requires huge quantity of Cement.

1 Like

It’s nice that you have shared this pics

But can we say that KCP will be benefitted next of this development

We aren’t sure who is the supplier

Good price movement today

Any positive news impacting cement business ?

The whole point is… if overall cement utilisation/demand in the region goes up, the industry benefits from it. This augurs well while capacity is being expanded. KCP is one of the cement providers for polavaram project. Don’t really know what is its share though.

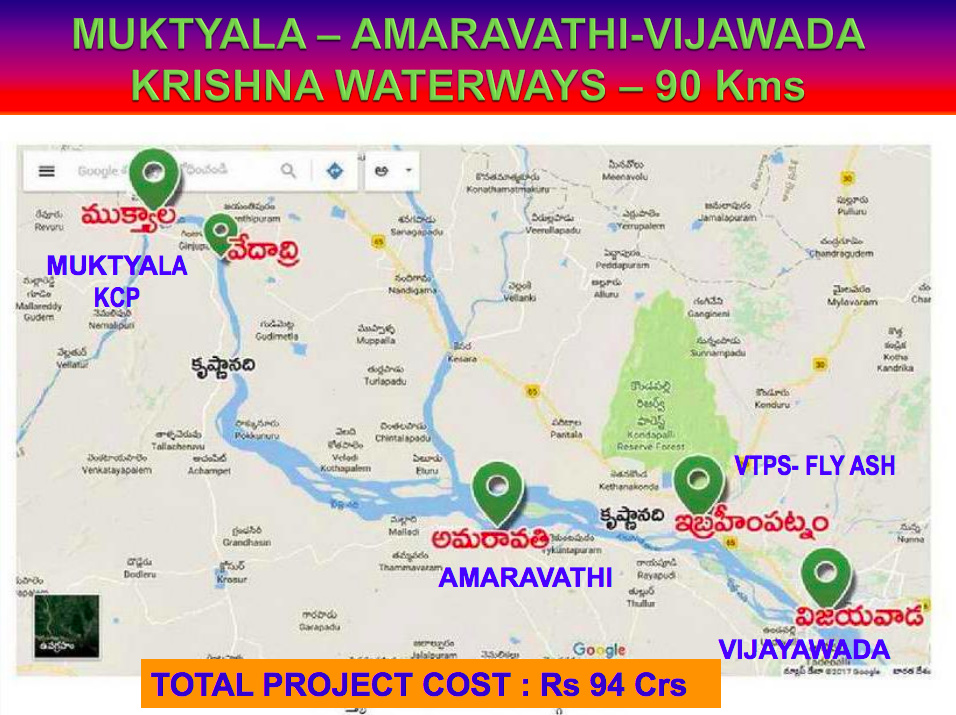

Also, KCP Limited has signed a MoU with Govt. of AP to supply cement through water ways to the capital construction as the Muktyala plant and Amaravathi are located on the banks of Krishna River …The total distance from the plant to Amaravathi is reduced to 70 kms by water from 140 kms by road.

Most of the dams in AP region are built with KCP Cement… Polavaram is included.

11 Likes