The list u put up extends to some more pharma companies like etc., Housing finance companies etc, manufacturing/consulting companies like newspaper companies etc. Kitex is under my watchlist. I would want to watch it for any improvement in business fundamentals.

India “not scared” if Monsanto leaves, as GM cotton row escalates -

U.S. seed company Monsanto is welcome to leave India if it does not want to lower prices of genetically modified cotton seeds as directed by the government, a minister said on Wednesday, in a sign the rift between New Delhi and the firm is widening.

In case if monsanto leaves india…what could be the potential effect on Kaveri seeds…Does that mean they will loose all the cotton seed business…which makes around 70% of the total revenues…Please some one answer this if I am interpreting this wrong

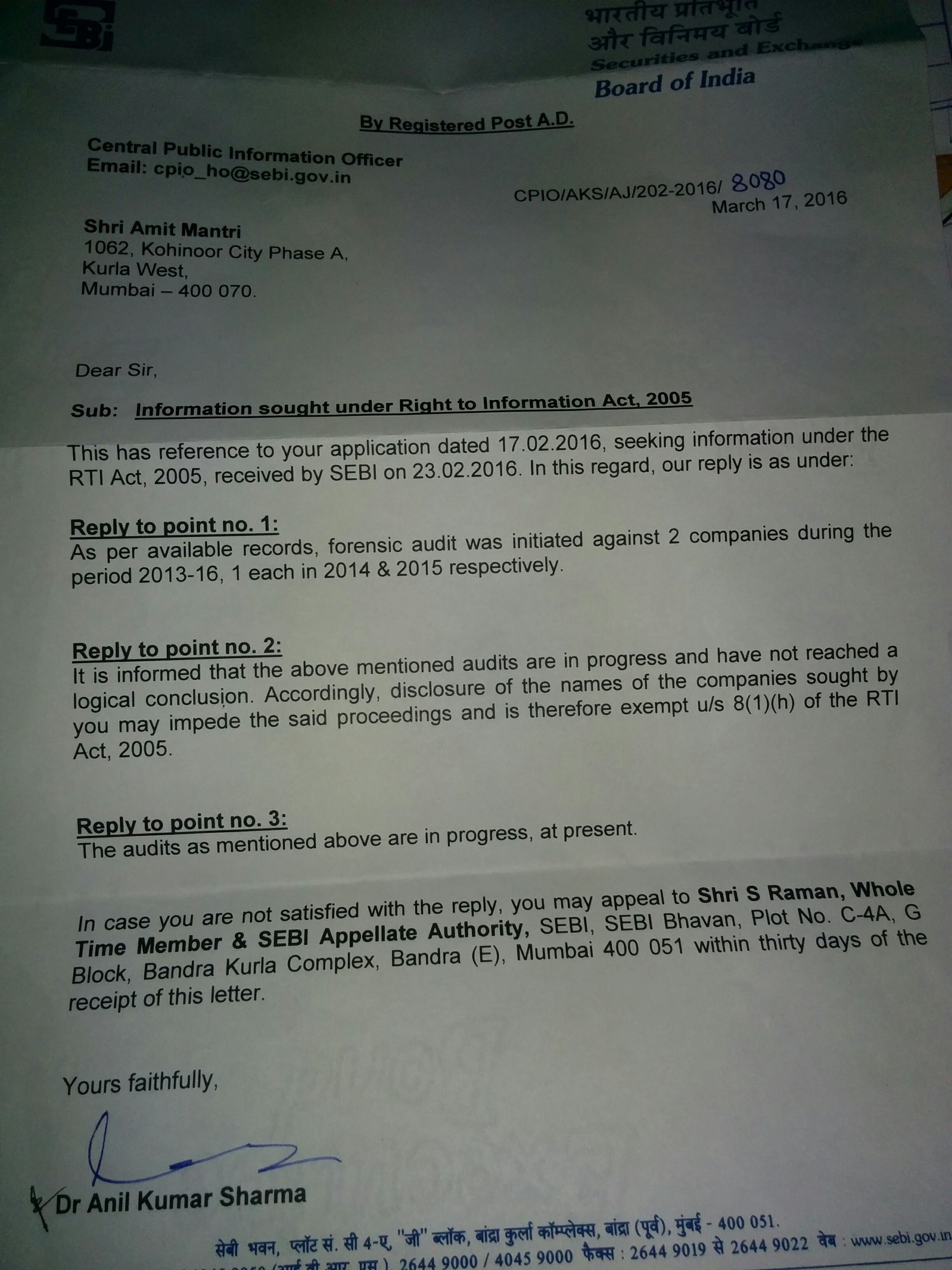

KSCL management had said in the concall that the forensic audit initiated by SEBI was a routine matter. SEBI response to RTI request - Has initiated only 2 forensic audits over the last 3 years (including KSCL). Seems like SEBI rarely takes such a step.

But the reply from SEBI and KSCL is contradicting.

KSCL is saying it is a “routine matter” but SEBI’s reply implies it is a “rare event”. Now I understand it is upto us to seperate the “Chaff”, but I am concluding that the doubt on KSCL is still unresolved.

AP and telangana state govt discouraging farmers to go for cotton. Hence acreage may drop in FY17

FY17 guidance - cotton 6.5 to 7 million packets

FY17 guidance - non cotton 23-25% growth over FY16

Maize acreage may go up…… Due to good expected monsoon

EBIDTA - non cotton = 28-30%

Cotton seeds market size 5.3 cr 14-15

4.3 cr 15-16

4.2 cr 16-17 E

EBIDTA per packet - cotton seeds - Rs 200

KSCL expects 20% volume growth in FY17 over FY16 resulting in market share gains

Strategy for market share gains

extending credit (mainly in telangana)

Wont compromise on margins

of the 20% volume growth targeted…10% (about 5.5 lacs incremental pkts growth from maharashtra)

employee costs….9 cr per quarter - standalone. 11cr per quarter - consolidated

Decision for utilisation of around 500 cr towards dividend or buy back in Q1FY17 con call

Forensic audit is under process. May take about 1 year to complete

New plant in karim nagar…… near main paddy growing area

Capacity = 10mt per hour

Production cost - cotton seeds FY16 340 per pkt

Production cost - cotton seeds FY17E 380 per pkt

The incremental cost would be passed to dealers (reduction in discount) and farmers

Mithun Chand interview - 11/May…CNBC

Impact of changes in MRP and Royalty

Particulars Earlier Current

MRP of cotton seeds 930 800

Royalty (incl of service tax) 185 49

Net 745 751

So there is no impact on margins due to reduction in MRP as royalties have been reduced correspondingly

However, the production cost is likely to increase in FY17 (refer concall notes above)

Area under sowing for kharif cotton crop is down by 20% while it is up for almost everything else as of July 15 2016 (Source ministry of agriculture). However, total sowing area is up by 4% this year compared to same period last year. Looks like farmers have switched from cotton to pulses and other cash crops. Monsoon is also delayed this year. that will push some seed sales to July from June. This will impact June qtr sales which is a major qtr for Kaveri.

If June qtr results are bad stock will take a beating. No news on SEBI audit yet. So that’s another overhang.

Thought of sharing this article in todays ET (20/Aug/16). The landscape for GM seeds appears to be very large…it covers maize, soyabean, cotton, potato, canola, papaya, alfalfa and squash. And there would be many more to come.

From the article one can deduce that Nuziveedu seeds equation with Monsanto has soured significantly. Wondering whether - Once the Monsanto - government issue is resolved…would it be a significant advantage for Kaveri Seeds?

This is not a good news for Kaveri. 70% of their sales come from BT cotton and they and other seed companies depend on Monsanto for developing new varieties of seeds to protect against pests that develop resistance to existing seeds.

Earlier this year, govt put price controls on private royalty price arrangement between Monsanto and seed companies. Monsanto had threatened to pull out of India. Govt has since withdrawn the order but Monsanto is still pulling out.

If not from Kaveri and other Indian seed companies in similar position, then from where will the farmers buy cotton seeds? So this should be bad for all Indian seed companies. The farmers might shift to other crops and that should be a big push for cotton prices.

Going by the tough stance taken by the government, hoping that they have the indigeneous solution for this around the corner.

They have not even mentioned the SEBI ordered forensic report anywhere in the report despite the audit being ordered in Dec-15 which is during the financial year. Even the secretarial auditor has not mentioned it, which draws a question on the company’s willingness to disclose

The COO appointed in May-15 is a veteran of 2 decades in the agro chem industry, last working with BASF. The remuneration is decent ~1.1crores. However, not on the board of directors.

3)The MD&A does not even talk about market share (or movement therein), competition activity (other than being dismissive that farmer will go for quality) or industry specific concerns such as Bollgard-2. I did not learn anything from this.

4)they pay negligible VAT or service tax being an agriculture industry. The possible GST impact is not even alluded to in the report http://finmin.nic.in/reports/modelgstlaw_draft.pdf the draft GST law specially excludes seeds from the definition of agriculture via Section 2(7) which states that

2(7) “agriculture" with all its grammatical variations and cognate expressions,

includes floriculture, horticulture, sericulture, the raising of crops, grass or garden

produce and also grazing, but does not include dairy farming, poultry farming, stock breeding, the mere cutting of wood or grass, gathering of fruit, raising of man-made forest or rearing of seedlings or plants;(emphasis added)

5)the industry appears pivoting towards an integrated approach involving seeds, pesticides and biologics. There seems a real risk of disruption due to this and competition from integrated players like Bayer Crop sciences.

While one must appreciate their double digit CAGR across revenue, profit, assets, the disclosures are far from adequate in my view,. This is a case where an investor will not get a balanced view from the annual report.

1) Revenue : at Rs. 493.97cr v/s 539.36cr for Q1FY15 (down 8.41% on Q-on-Q basis ) 2) Net profit after tax : Rs. 160cr v/s 222.28cr for Q1FY 15 (down 27.89% on Q-on-Q basis )

( Yet Employee benefit expense see a 72% increase from 6.22cr to 10.74cr ).