Any study v/s Somani for last few quarters? intent is to udnerstand, what is working for somani and Kajaria finding it difficult to short of extend what they have done in last few years?

Axis report raises the same issue…

Axis Direct’s research report on Kajaria Ceramics Kajaria Ceramics (KCL) reported volume growth of0.5% YoY in Q3amidst expectation of slowdown due to demonetization. Management expects volume growth to improve to 5% YoY in Q4,implying growth of 4% in FY17 (vs. earlier guidance of 7.5% YoY).While management expects revival from Q1FY18, we expect construction activity to remain slowin the mid-term due to decline in new launches by developers. Outlook We like KCL from a long-term perspective driven by government’s focus on affordable housing, sanitation and implementation of GST. However, with volume growth slowing down to 3% in 9MFY17 (vs. 13% CAGR over FY12-16), resulting in earnings growth tapering to 12% in 9MFY17 (vs. 30% CAGR over FY12-16), we believe the current valuations is rich(31x FY18E earnings). Maintain SELL. For all recommendations, click here Disclaimer: The views and investment tips expressed by investment experts/broking houses/rating agencies on moneycontrol.com are their own, and not that of the website or its management. Moneycontrol.com advises users to check with certified experts before taking any investment decisions.

Source:

sir i was analysing the business and since the distribution+brand actas a kind of moat can you please tell me more about distribution network of kajaria?

I m aware of the fact it has wide network in tier ll and lll but can a get a ball park figure of the distributors

The had released the below numbers in their results for the year FY16.

-

25 corporate offices/ Display Centers accross the country

-

Distribution Network of strong and loyal 1100 dealers all over the country

-

Above dealers cater to around 4000 associate dealers across the country

1 Like

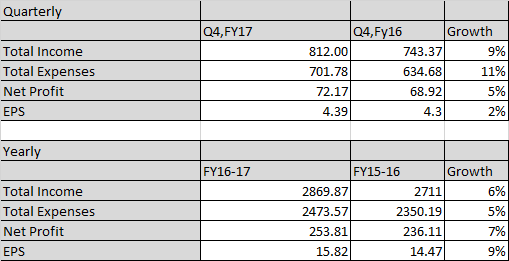

Not so good results…

Somehow I have never been convinced about the valuations these companies receive (Kajaria, Cera). Neither the growth rate nor the margins justify the high P/E. The brand name and extensive distribution network is supposed give them a moat, but what use is a moat if it doesn’t reflect in the numbers?

(Disc,: No positions)

1 Like

There has been, in my opinion, fair impact of channel clearance going on currently due to the dual effect of demon and impending gst. Add to that a slowdown in real estate which has had an impact on kajaria. Steady state numbers will likely start trickling in from Q3FY18.

1 Like

Kajaria launches exclusive range of faucet and sanitaryware

http://www.hospitalitybizindia.com/detailNews.aspx?aid=27197&sid=1

I have conflicting views going thru my mind as to such extreme valuation. Below are my thoughts, pls share your thoughts -

Bull case :

- The market for tiles has to increase , people will not go back to cement, mosaic etc. Question is how long will it continue to grow at double digit 10- 12% rate. Based on govt initiative and transparency brought in the RE more low/ mid income people will be inclined to purchase. Will every house have tiles, No, but it should be more than 10% houses ( as somewhere mentioned in AR of Kajaria). So more house and slow move towards tiles will ensure that market continues to grow.

- Market share will move from unorganized to branded company. Kajaria has spend on average ~70 cr / per year on Advt and promotion in last 3 years. To spend same amount of rupees for small unorganized player will be difficult if not impossible. So, in reality it might happen that 3-4 brands dominate the market. KCL hopefully would be continue to remain number 1 in that situation as well based on its brand+ Dist. Not sure if the company will compete on price or not.

- Time is friend of wonderful company’s, KCL is a wonderful company hopefully time will continue to favor it.

Bear case :

- Stock is richly valued, in case the performance of the company does not improve in next 2 -3 qtrs (w.r.t market) it will have a significant De- rating.

- A Big investor ( aka Jio) might decide to enter into ceramic industry purely as a marketer - do JV with unorganized partners, spend 100cr on branding, flush the market with its own product with good incentive to distributor, survive at 5% margin 15% ROE and take away market from KCL.

Now, I am not sure which of these will play out. Given the valuation Bear case 1 would be suicidal for me , as I have entered recently. But at the same time Managment execution of the past gives the trust that they would make every effort to increase the profits, CF etc. I don’t think irrespective of how great they continue to execute they would be able to justify the existing valuation.

Still, I would go with bullish case for the time being and see where it stand after Mar’18. Before deciding to sell the stock.

Disc: Invested, so views may be biased.

I am not sure if this is the right price to buy this stock but i am quite positive on the company and sector as a whole from 4-5 year perspective … bought this stock after lot of research and first hand experience of tiles being used in real estate in gurgaon, mumbai and bangalore

Note: Long On stock from past 3 years, highest holding of my portfolio (14%) with a CAGR of 32%

Cheers !

I have stayed away from businesses with a very large addressable market for this reason, there is always an incentive for a really large player to play around with the economics and make life difficult for the incumbents since there is a large profit pool that one can tap into.

However if you look at Tiles,Sanitaryware & Faucets as a combined segment where the addressable market size for organized players is in the range of 20,000 Cr per annum, at a 10% profit margin the profit pool of the entire industry is hardly 2000 Cr. This kind of number just does not excite a large player to put in the effort it takes to capture the market.

Also it is much easier to sway individual customers by giving the kind of freebies that the ecommerce players and Jio are doling out to built critical mass. It is much tougher to do this in segments where influencers are present - building products, metal fabrication where there is a service component attached to a product. In these cases one needs to do significant BTL, build credibility with the trade channel to make a dent in the market. Each trade channel partner is an entrepreneur by himself who has a reputation to defend and customers to service, it is not easy to get to somebody to stick his neck out in favor of a new entrant who is yet to prove himself in the marketplace.

Disruption scares me big time since that directly impacts the terminal value one can assign to a business, however I would say that the prospects for disruption in the current scenario for most segments is overrated. Some industries are just much easier to disrupt than others, building materials is not one of them in my opinion.

9 Likes

Btw, post the gst correction mr Kajaria sounded very optimistic of maintaining double digit growth for atleast 3 years.And said since they have cut prices others will follow. Gas price will have 30 -50bps impact on margin and ebidta margin to remain at 18-20%.

Interesting - managment usually has walked the talk but are they overconfidenet or better days are ahead?

1 Like

Hi,

Request the people who work or are aware of real estate industry to talk to the dealers, builders, realty salers, mfg etc to gather more info on managment’s claim. Getting idea on competitive insights of the company might also help us, either to stay convinced or to sell the stock.

D

Motilal Oswal MF Is constantly increasing its position in this stock.

1 Like

What will be the impact on increase in crude /gas price on kajaria’s bottomline?.

Near term challenges present an attractive opportunity to accumulate the stock. I anticipate a gradual pick up in both volumes and margins over the next few quarters. Kajaria remains a long-term investment with strong growth prospects and one of the best stocks to play the housing theme.

The next 1 year could be tough and I am assuming the not so bright days in the housing industry will have a lingering impact on Kajaria

Why sales going down? Any change in business trend?