is there somefamily issue out here…rumours floating around of a possible split…wait and watch for some

time

where did you hear this?

@Kajaria Investors,

Ashok kajaria in an interview mentioned Industry growth was poor during Jul-Aug (-ve). Then how come somnay ceramics and cera made decent profits ? Does anyone have an idea ?

1 Like

I also have same question. though Cera has comparatively small revenue from tiles, but Somany is largely in tiles. Kajaria claims having increased market share though in absolute terms they could not get desired growth, than how come Somany could do it? Any insight from other members?

1 Like

These questions lead us to credibility of promoters, we need to have an answer else better reduce the holdings till we get the facts corrected / reflected in books. I saw it declining for almost 25%, which we never saw in recent times. I am still holding this as average price is much lower but seriously thinking of riding other boat in same river before this starts sinking or giving less than expected returns.

1 Like

Recent correction in Kajaria gave a chance to those who were having a left-out feeling.

Off late I have been looking for Purchasing an Apartment & hence have been roaming around these days & seeing closely different Projects from Builders.

The key differentiator for me from ground zero is the is ample amount of growth opportunity for Kajaria from even here, with just a Market Size of roughly Rs 7000 Cr.

Demonetization (Demand Revival in future due to immense liquidity available in the system) coupled with GST Roll-out with parentage of the promoters, which it enjoys for now nearly 25 Years & Product-Mix, along with presence of reputed FII’s such as WESTBRIDGE & JWALAMUKHI, definitely gives a reason to cheer at least to me for the coming years.

Disclosure Invested & holding for 1+ year now.

Are you referring to growth opportunities for sanitary ware products in general or Kajaria in particular? One of my key concerns with this industry is products are commoditized and there is virtually no difference between Kajaria and other brands so it all comes down to distribution. There is no denying that sanitaryware industry will grow not just from new construction but from conversion (Indian models to Western) and replacement but will competition kill the margins in the business?

Yogesh thanks for bringing out your point of view.

Coming to my reference, I was specifically talking about the tiles, as most of the builders compromise may be on Sanitaryware but as far as tiles are concerned, almost 70-80% in my visits I could find Kajaria Vitrified Floor & Wall ties, & hence it justifies the faith & command it enjoys & premium it deserves.

On the other hand Cera fittings or for that matter Jaquar fittings, I could see only with builders of league & not everywhere.

Obviously natural gas which acts as a key raw material can be considered as a commodity, but IMHO ,brands like Kajaria, even in that case have that liberty to pass the increase in Raw Material Prices to customers, even at times with lag.

GST Rolling out will totally kill dry down the business for large un-organized players operating out of Morbi & hence will also help Kajaria in Volume increase & Margin Expansion in the future & Anti-Dumping duty on the Chinese tiles too gives an opportunity to Housing for all & Make in India Campaign too.

Views may be biased but open to counterfeit & logical criticism.

Regards,

Bharat

2 Likes

Competitive advantage can come not only from a differentiated product but also from a very strong distribution network. Kajaria scores in this segment over others. They can reach more customers - both retail and builders than others. Also, they have been able to build a brand name with good recall value, which also helps them. Since, for most people home building is a once-in-a-lifetime thing, they would try to get the best they can afford.

4 Likes

Rogger that Abhishek.

Distribution channel is a platform for carrying out business which is built over a period of time, with rigorous efforts, understanding the pulse of the consumer/targeted market, alongwith designing a product-mix which caters effectively & efficiently to that targeted market.

Promotes have been bang on this, with widespread experience in the field, for over 2.5 decades now.

What I was referring to, was meant for the brand it carries & the premium it deserves, as to even in such lackluster period of economic growth & nearly subdued demand in RE, for quite a significant time now, it has been maintaining a comparative good top-line, but accompanied with a commendable Bottom-line.

It has been increasing its distribution channel continuously & becoming the renowned name in household, which cannot be dented in a year or so. That is what is the moat along with Promoter integrity & knowledge of Market Pulse.

Regards,

Bharat

I have realised over time that one must not be in hurry to sell a stock with a brand recall and huge opportunity size. I have been guilty of selling a legacy stock like Asian Paints in early years out of ignorance and do not want to repeat the mistake. Although I did feel the temptation to sell Kajaria @ 700 couple of months back when it was trading at around 40 p/e but decided to stay put for reason mentioned above.

Reproducing the extract from my portfolio topic posted in Sep’16

I don’t think you can build a sustainable competitive advantage out of tiles, ceramics and sanitary ware products. Such advantage is usually a result of R&D which I don’t think exists in this business. This is already a mature product. Maybe few years ago not many people could handle the manufacturing process but this is not rocket science so over the years there will be more competition that will bring the ROE to a more reasonable levels of 15-20% from current 30%. Entry barriers are also low.

This stock is trading at a sky high valuation. All the bullish arguments are already factored in. At current valuations, long term investors will make money only if actual performance exceeds what is already priced in. My back of the envelope reverse DCF model shows that 20% growth over the next 10 years followed by a steady growth of 8% in perpetuity is already priced in. Where is the value?

4 Likes

yogesh, what did you use as discounting factor? thanks butun

Discount rate used is 13%.

Compapred to Somani, result once again in this quarter is subdued.

some how no logic convinces on why they should perform any inferior to Somani in terms of profitability.

any insignt?

Agree on the valuation bit but not on the moat part.

This business has a tremendous moat, the very fact that the company has been winning market share and expanding product portfolio in spite of having a huge unorganized segment that can undercut prices implies that there is a moat. The moat here emerges from a combination of a well known brand that ensures channel stickiness, relative scale advantages compared to marginal players and the strength of the distribution network.

I am a distributor in my profession, each distributor tends to bring in his own ecosystem of a catchment area, strong relationships and repeat business. A distributor eventually tends to consolidate with 4-5 OEM’s since that reduces complexity and makes operations easier. As a distributor it is very easy for me to push a well known brand which comes with credibility than to push a new product where the effort involved in selling is high (even if the margins are better here). For a new entrant to enter the tiles & sanitaryware business and build the kind of distributor network that a Kajaria or Cera has created will take ages and the distributor needs to be given disproportionately large incentives to build a market in the first place.

In fact I am tending towards the view that a brand + distribution combination in a market with unorganized players is one of the strongest moats one can find. It looks very simple and innocuous on paper but it beats the hell out of most other combinations.

14 Likes

Branding only works if there is something genuinely unique about your products ( e.g. Page products while expensive are of much better quality and design compared to other Brands) . Plastering one of the Bollywood Khans on your product and charging 5X the price of the so called unorganised sector does not make a brand or give it any durable moat.

Incidentally, cera, Kajaria, somany etc are mostly marketing companies that actually get the bulk of their products manufactured by the same unorganised sector through JV arrangements, it is only a matter of time before their partners wisen up and start their own Brands at much lower price points.

Distribution- yes it is a barrier initially but can be surmounted if your product clicks with the customer, just ask Patanjali.

3 Likes

Distribution is moat no doubt about that. However, it is more valuable in FMCG type products where you have to make sure that your product reaches to over a million outlets from the smallest paan shop to biggest supermarket. Availability drives consumption.

Home improvement retailers are generally clustered in a small block in a neighborhood an push brands that give them biggest margins and offer consignment sales options where the retailer dos not have to tie up his capital in inventory. Since these products are purchased occasionally, customers are likely to shop around in the market before making a decision unlike FMCG. I have visited some of these and Kajara, Cera products are just like any other products and only differentiation is on price and availability. My rough estimate is tiles and ceramic products are carried by about 5,000 to 10,000 retailers around the country compared to FMCG products that are carried by over a million retailers. With that perspective the distribution network of a FMCG is far more valuable than home improvement.

Looking at the past performance, there is no doubt that Kajaria has the best fundamentals however I think these may not continue as competition will catch up. There is enough room for everyone to grow as the industry itself will grow but profitability will come down to more reasonable levels. I wanted to seek opinions of others who own this stock to see where do they see the value.

4 Likes

There are 3 phases in the buying process, at a psychological level this is how they work when you have the question of branded/unbranded

-

Credibility based shortlist - Happens based on references, brand and associations the brand has been able to generate. Here a Kajaria/Somany will easily score high and make the shortlist for most customers

-

Objective analysis - Customers go “Ok brand is known, I have 3-4 shortlisted but which one of these objectively makes a good fit for me based on the parameters?”. Now comes in the price vs value comparison, after sales service etc

-

The decision - After weighing the objective analysis of step 2 the final decision has a definite emotional component as well. XYZ may look functionally better/5% cheaper than a well known brand but is that worth the try? Most cases customer goes with a known brand even if it is marginally inferior on a couple of parameters

Interesting thing is the more similar the options are in a segment, greater the influence of brand and intangible associations in the decision making process. If the product features are distinct from one another chances are the decision will be weighted more in favor of step 2. Which is why you see relatively unknown companies sometimes win the race in enterprise software/information based economies where the points of difference are many and the customers are very discerning.

In segments where the product/service across players are more or less similar to each another, the better known brand has a better chance of winning the race. The strongest moats are found in businesses where the points of difference aren’t high - classic example being Coke.

@ Ricky76 - Hence I beg to differ. Uniqueness of a product isn’t really a big factor in most segments which is what makes business analysis so challenging. Else product managers would have made the best stock pickers. Retail customers aren’t very discerning about product features, hence the brand recall + influencers play a very important role. I was selling enterprise software in my previous stint, even there where the buyers are knowledgeable and discerning the actual product/solution mattered for only 50-60% of the weightage in the eventual buying decision

@ Yogesh - Also do consider competition in a relative sense. I may not have the best R&D/Marketing dept in an absolute sense but if the gap between me and my next competitor in my segment is large, that makes me a very good business (think the APL Apollo example where the competitive advantage comes from lack of serious competition than from anything else)

5 Likes

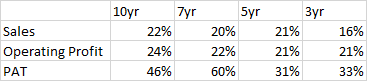

Lets look at some numbers to understand how Kajaria has been doing over the years. This sufficiently shows how well the management has been running the company.

Sales, OP, PAT CAGR over the years

OPM, NPM maintained over the years…this cannot be possible without a good brand recall for its products given the number of unorganized players

Free Cash FLow generating company…

Efficient use of capital…

Even in this industry of huge competition from lower margin unorganized players, this remains a debt free company…

Always paying dividends…

I think all this clearly indicates management has been running the company quite well over the last 10 years… this would not be possible without having a moat when you consider the number of small players in this industry…

Going forward with government push like Digital, GST, demonitization… will enable the next phase of growth for such a well run company…

I am not saying valuations are cheap now and it is a buy now…My only point is it is a good long term story and will be a decent compounder… already a multibagger for me and i intend to continue holding it.

Disclaimer : I am invested in this company for some years now and views might be biased. This is not a buy recommendation but just to show how well the company has executed over the years.Please do your own research before investing.

5 Likes