Did some study on Kajaria and found to be interesting.Many things have been written already and what I am adding may not be new.

Total Indian tile industry size is around Rs.19,500 crores,but compared to China and Brazil tile consumption in India is just 1/6th and 1/7th respectively which clearly shows huge growth potential lies ahead for this industry to grow in the future.This is a very competitive space to operate with so many unorganized players manufacturing at low cost,low quality tiles and pretty much fragmented.Most of the tile production in India happens at Morbi Gujarat which is a hub for unorganized tile companies.

There are few tailwinds for the organized tiles industry in India in near-future:

1.New governmentâs push for housing for everyone.

2.Gujarat PCB's directive to close the tile units utilizing coal fired furnaces brings a level playing field for organised players in terms of energy costs.

3.Per capita consumption of tiles in India is 6 times less than china and 7 times less than Brazil which shows huge potential for growth.

4.As per census 2011,number of cities have grown 3x in 10 years which shows huge urbanization happening in India.

5.People migrating from rural to urban will cross 40% from 33%; Young generationâs brand aspiration,affordability.Tiles expenses as a % of housing cost less than 10%.

Organized sector has 50% of market share in the Indian tiles industry and growing faster by gaining market share from the unorganized sector.Tiles industry grows at 10% to 13% in India every year,but Kajaria grows at 15% to 20% at the cost of unorganized sector.This is attributed to the brand aspiration,asthetics,various designs and sizes in its offering,growing disposable income among young Indians,strong distribution network,branding,marketing.

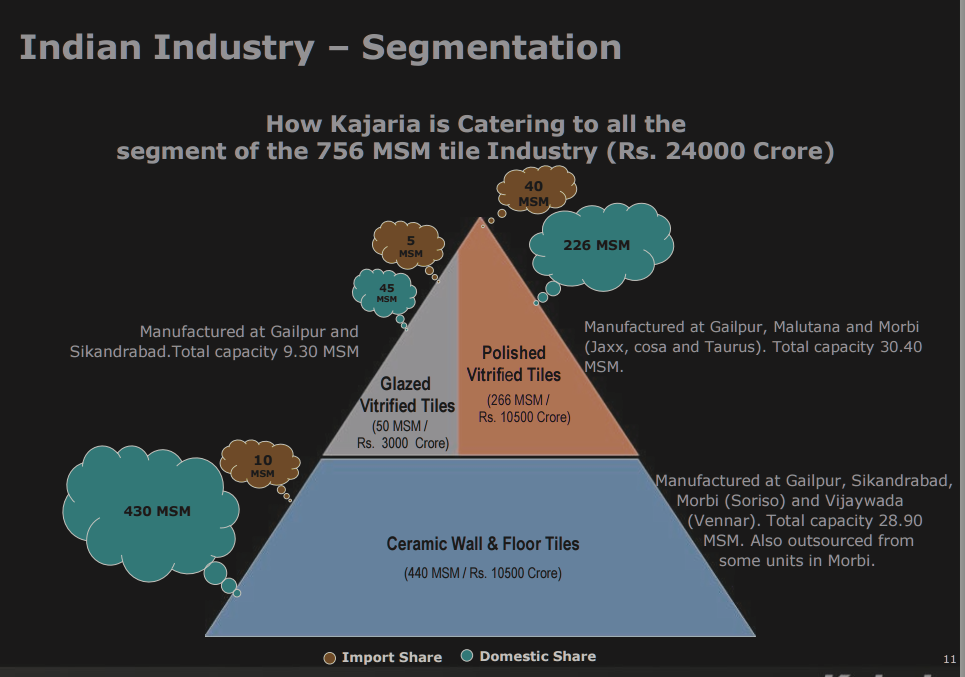

Total capacity of tile production in India is about 700 MSM in 2013.Kajaria has a capacity of 47 MSM which translates into a market share of ~ 7%.

Kajaria sells three types of tiles:

Ceramic tiles: Mot commonly used tiles in households for flooring and wall.Lot of competition in this space as this is the low-end in the value chain of tiles.

Total size is 415 MSM; Kajaria has a share of 26 MSM gets 44% of revenues are from this segment.

Polished Vitrified tiles(PVT): There is a structural shift towards vitrified tiles due to its high-quality,less porosity,less water absorption,highly durable and its strength.Expensive than ceramic tiles.

Total size is 236 MSM;Kajaria has a share of 11.40 MSM.Kajaria gets 38% revenue from this segment;higher operating margins of 16-17% compared with 14-15% for ceramic tiles.kajaria is increasing its market share in this segment and consumers are also preferring these tiles due to the reasons mentioned above.Kajaria used to import before;but it has it is consciously investing in adding PVT capacities due to its high margin and strong growth.

Glazed Vitrified tiles(GVT): Total size is 30 MSM; Kajaria has a share of 9.30 MSM,contributes to 17% of its revenue in 2013-14.It is alternative to the expensive Italian marbles and the time to install is lot quicker and cost-wise a lot cheaper.

This is even more expensive than PVT and it is gaining acceptance from the consumer on the upper end.

Accessiblity:

Just like cement industry,Tiles industry suffer from logistics cost if the manufacturing plants are not located close to the customers selling points,margins will take a hit owing to the huge logistics cost involved in transportation across India.

Kajaria has strong presence in North mainly due to its plants are located in Gailpur (Rajathan),Sikandarabad (UP).It did not have strong presence in south before.

In order to get access to the southern markets,it made a joint venture by acquiring 51% stake in local tile companies; one in Vennar Andhra Pradesh for 2.30 MSM for southern markets. And 3 other in Gujarat Soriso Gujarat 51% stake 4.60 MSM;Jaxx Vitrified 51% stake 3.10 MSM; Cosa Gujarat 51% stake 2.70 MSM.

Instead of setting up capacities from scratch,Kajaria went through this asset-light JV route to reduce the time to start production and by acquiring 51% so that it can dictate the tile baking process to its quality standard. Thus it focusses on branding,marketing when the local player takes care of production.

Why does someone go to Kajaria than any other company?

This is the question comes to our mind when there are umpteen number of players in this low entry barrier business.Kajaria has been operating for the last 25 years started with 1 MSM in 1988 and has touched 45 MSM now.This growth has been possible due its acceptance of its products,wide dealership network,strong brand recall in the market.Kajaria enjoys market leadership and has achieved super brand status for a number of years.Above all,there is a price difference of 50% between Kajaria and unorganized player,still customers go for Kajaria simply because of its varied designs,size and superior quality of its products.

Does it have any Moat like low cost producer/ brand recall/pricing power?

It does.This is evident from the superior return ratios that the company has been cranking out for the last 5 years.Return on Equity 25% to 30%;RoCE ~ 30%,compounded sales growth more than 20%;compounded profit growth of 40% for the last 5 years.This clearly shows how fast the company is gaining from market share from the competitiors both from organized and unorganized players.The company also aims to reduce costs through several measures by introducing technologies like automation using robots in their plants,reducing gas prices by waste heat absorption systems to optimize the gas eliminations, Having manufacturing plants close to the customers to reduce logistics cost, cutting down on imports to in-house manufacturing.

Moreover, its working capital days and inventory days are continuously declining year after year which shows the demand for its products and the quick payment it receives from its dealers.

What are the future growth drivers?

Still more than 60% of the houses in India have been constructed with flooring materials like mud,sand,cement,mosaic which provides an idea of how much more this industry has to grow to reach its saturation.Today tiles have become an indispensable part of the new houses in Tier-II and smaller towns just like big cities since the cost of tiles are less than 10% of the total house cost.Huge migration from the small villages to towns in search of better oppurtunites which leads to faster urbanization,replacement of old flooring with tiles(currently 15% share of the tiles industry),hospitality sector growth,Organized retail,real estate growth are various avenues of future growth.

Kajaria is in a sweet spot to grow exponentially in its industry due to its dominant leadership.

Competition:

Top 3 players accounts for half of the organized sales of Rs.10,000 crores.

Kajaria Rs.2000 crores

H&R Johnson Rs.1900 crores

Somany : Rs.1400 crores

|

Operating margins |

||||||

|

2014 2013 2012 2011 2010 |

||||||

|

Kajaria |

12.41 13.95 15.27 15.58 15.71 |

|||||

|

Somany |

6.49 8.12 8.40 9.64 10.78 |

|||||

|

Orient |

8.0 10.00 9.10 8.84 12.91 |

|||||

|

Net margins |

||||||

|

2014 2013 2012 2011 2010 |

||||||

|

Kajaria |

6.2 6.3 6.14 6.2 |

|||||

|

Somany |

2.22 3.00 2.83 3.28 3.79 |

|||||

|

Orient |

0.35 1.71 2.46 - 4.47 |

|||||

|

Other competitor Nitco tile is making losses for the last 3 years. |

||||||

|

Look at the difference between Kajaria and its listed competitors in terms on margins.They are not even close to its OPM and NP.What is more important is kajaria is less leveraged than its peers. |

||||||

|

Pricing realizations for Kajaria: Realisation per sqm (Rs.) 2008-09 294 2009-10 292 2010-11 321 2011-12 330 2012-13 348 2013-14 354 It took 5 years to increase the prices 20% so the future growth should come from volume only and not value.It cannot raise prices vis--vis inflation. Region-wise revenue split: Today, it has a strong presence in the north, which contributes 42% to revenues; the south contributes 29% and the balance comes from the west and east zones.Currently, tier 2 and 3 cities contribute 25-30% to the companyâs topline. Key risks: |

||||||

|

Growth comes at capacity additions only and not through price realizations because tiles industry does not have pricing power owing to its excessive competition.So,far Kajaria steered through its journey very well through low cost asse-light joint Venture model and its own capacity additions.So,future growth should come from more JVs and its own capacity additions.Its debt to equity ratio of 0.4 provides an opportunity to further leverage its balance sheet.So far it has not diluted equity but recently it has diluted 7% of its equity to West Bridge Capital for further capacity additions.It is looking for capacity additions to the tune of Rs.450 crores. Another risk is entry of foreign companies(Italy,Spain) in the Vitrified tiles segment.Right now imports from other countries are facing margin pressures due to Ruppee depreciation.So,not sure how long the foreign companies sustain their presence with low margin business.Logistics also play a spoilsport since not all the states are not located close to the port. Chinese import risk: Government of India has imposed anti-dumping duty on Chinese imported tiles.Also, cost of manufacturing has increased in China which has naturally reduced the Chinese imports. Southern presence needs to be increases mainly because Tamil Nadu and Maharastra are the biggest mortgage markets where a lot of construction activities are going on.So,new plant additions should be done on the southern side to reduce logistics cost. Now let us look at the valuations: Current valuations are bit stretched but no one can time the market nor the PE ratings. At CMP of Rs. 600,it trades at PE of 30 assuming forward EPS of Rs.20 in March 2015. PE of its competitiors: Orient 73 Somany 35.55 So,the future growth has to come from EPS growth. Historically the EPS has grown at 30% and if the similar growth is mainted,stock will perform better.

|

||||||