Being fourth largest supplier of ethanol to OMCs(Source: Q1 Concall)

, I hope they have good chance of netting big chunk with this price hike…also future of ethanol blending looks sustainable.

Anyone attending the AGM on 26 Sept.?Pls. inform…have some q’s…

Disc. : Invested.

Latest SHP shows RJ added 5,00,000 shares this quarter.

1 Like

JUBILANT REPORTS STRONG PERFORMANCE IN Q2’FY19

Revenue at Rs. 2,269 Crore, up 38% YoY; EBITDA at Rs. 454 Crore, up 45% YoY

PAT at Rs. 210 Crore, up 64% YoY with EPS of Rs. 13.5 per share

Detail Result & Presentation:

Q3 CONCALL HIGHLIGHTS:

H2 will be better than H1…both volume and margin wise.

Vast opportunity within Venom based Allergy

Therapy Products…only competitor left the segment in Apr 2018 leaving space open for Jubilant in North America…also big opportunity outside of North America i.e. in Europe etc.Expecting US FDA permission for hiking capacity in this segment.

Jubilant Pharma IPO on track and expect to go through before Mar 2019(Depending on Market condition).

RUBY FILL installation going on as per plan though nos. not shared.

Overall good result and great outlook.

Disc.: Invested.

1 Like

Dec, 2018 result is out and it is not looking good.

EPS is 2.3 vs 6.15 YoY.

Revenue 859 vs 933 Cr.

Also, It has announced two acquisitions which were its own subsidiaries.

One is loss making. Biosys has given loss of 26 Cr.

and ChemSys has given profit of just 1 cr.

BioSys has huge PaidUp share capital of 187 Cr. So, I think, company need to pay this to acquire loss making company.

Disc: not invested.

Look at consolidated nos for jubilant life.

Nos are good.

q3 fy 19 sales 2353 crores vs 2041 crores for q3 fy 18

NP for q3 fy 19 267 crores vs 212 crores for q3 fy 18.

q3 fy 19 eps 16.74 and 9m FY 19 eps 43.24

Thanks @hitesh2710

Even BSE’s website is broken. The link I had shared was broken so updated with PDF link.

Any comment about acquisitions! They are tougher to understand. Jubilant Life was in my Watchlist but after this acquisitions I have ignored it.

Is this acquisitions good?

Growth is high tough now, it has stabilized. Last four quarters including this quarter profit are high. Still, it is a good growth. If those acquisitions are not a problem then it is worth watching. Debt is not very high.

Acquisitions : It seems these are obligatory corporate actions only…they have only redeemed preferential shares of the subsidiaries at par.All preference shares issued by a company in India must be redeemable and should be redeemed within a period of 20 years from the date of its issue.Jubilant Biosys Limited was incorporated on 10 Feb. 1998 and Jubilant Chemsys Limited was in 2004, hence I think deadline must be approaching…any ways its not an acquisition…both are already subsidiaries.I think corporate governance standard is good for the Jubilant group.

Debt : Net debt 3118 as on 31st Dec.2018 down 113 Cr from 3231 Cr as on 31Mar2018. This figure includes mandatory convertible amount of

US$62.7 mn borrowed from IFC Washington with the conversion option at IPO of Jubilant Pharma which the management saying any time due, waiting for the right market conditions.Management during yesterdays concall alleged they are generating enough cash to fund capex and reduce debt also. Capex for the current year was 500Cr +.Finance costs at Rs 68 Crore vs. Rs 77 Crore in Q3’FY18, including Stock Settlement

Charge of Rs 15 Crore as against Rs 20 Crore in Q3’FY18.Hence I think debt is not much an issue here.

Some Concall highlights:

They have plan on track to commission new Acetic Anhydride plant in Q4’FY19, with annual revenues potential of over Rs 400 Crore. They have started operating one line 24X7 in Spokane during Q3FY19.Also,new Lyo line to increase capacity by 25% to be commercialized by H1’FY20.New capacity at Roorkee under commissioning for commercial production.

USFDA : Submitted reply to US FDA’s OAI on Roorkee plant; awaiting response…products affected from this plant is 1% of the turnover.

Bagged new annual contract with higher volumes and prices in the Ethanol Blending Program of the Govt. of India.

Pharmaceuticals Segment Highlights: up 29% YoY, contributing 60% to revenues with good margin of 27.7%

Specialty Pharma:Higher volumes & realisations in Radiopharmaceuticals.

Venom sales normalizing post unloading of inventory by competitor in H1’CY18, they are sole player left now in North America.

CDMO: Volume growth 27% and margin up from 21.7% to 33%.(YoY).

GENERICS: Volume growth 52% with margin 19.6% from -0.4% last year.

Disclosure: Invested and wish to hike allocation depending upon coming quarter performance.

The Board of Directors of the Company has approved the payment of a corporate brand royalty to Jubilant Enpro Pvt. Ltd. (a promoter group company), which owns the corporate brand name Jubilant. The royalty payment will enable the group to help protect, nurture and enhance the corporate brand name Jubilant and the group’s image globally. It has been decided to pay 0.25% of the consolidated revenue of the Company effective FY 20 as royalty.

Though media (CNBC Etc.) covering this negatively I’ll like to point out that even Tata Sons , owner of the Tata brand and promoter of Tata companies , has capped the royalty payment from group entities using the Tata name at Rs 75 crore. … Those companies which use the name indirectly pay 0.15% of the turnover. If companies incur losses, they do not pay any royalty.

At least promoters not fleecing but transparent enough…

Dis. Invested.

The royalty notice statnds withdrawn…

Jubilant Biosys expands collaboration with Sanofi in CNS therapeutic area:

http://www.jubl.com/media-press-details.aspx?mpgid=73&pgid=74&pressid=375

Jubilant Pharma proposes to issue unsecured bond outside India…though bond rate and amount tobe raised and purpose thereof is not mentioned, is it to replace the costly debt or in lieu of ipo or for any other purpose?

http://www.jubl.com/Uploads/files/47phfile_JPL-SGXIntimation-25.02.2019.pdf

Detailed business overview:

http://www.jubl.com/Uploads/files/48phfile_JPLAdditionalInformation-25.02.2019.pdf

Jubilant Pharma to raise US$ 200 mn through 6% rated unsecured bonds mainly to replace high cost debt :

http://www.jubl.com/Uploads/image/1076imguf_StockExchangedisclosure-JPLBondPricing.pdf

Looks like Jubilant Life is getting into troubled waters again. Few years back it had suffered due to its foreign currency borrowings and was hit hard due to currency swings. It seems with the weakened rupee against the dollar the lure of cheap debt is too much for some corporates.

Ideal thing would be to focus on reducing debt from cash flows even if it means reducing capex for some time.

2 Likes

Yes, totally agree with you…debt reduction must be first priority for Jubilant…They are saying purpose of this fund raising is to replace high cost debt,we’ll see…I think they wont increase debt level before impending ipo. Though management repeatedly talking about reducing debt ,pace of debt reduction in absolute term is slow though ratio improving with rise in ebitda over last few years…

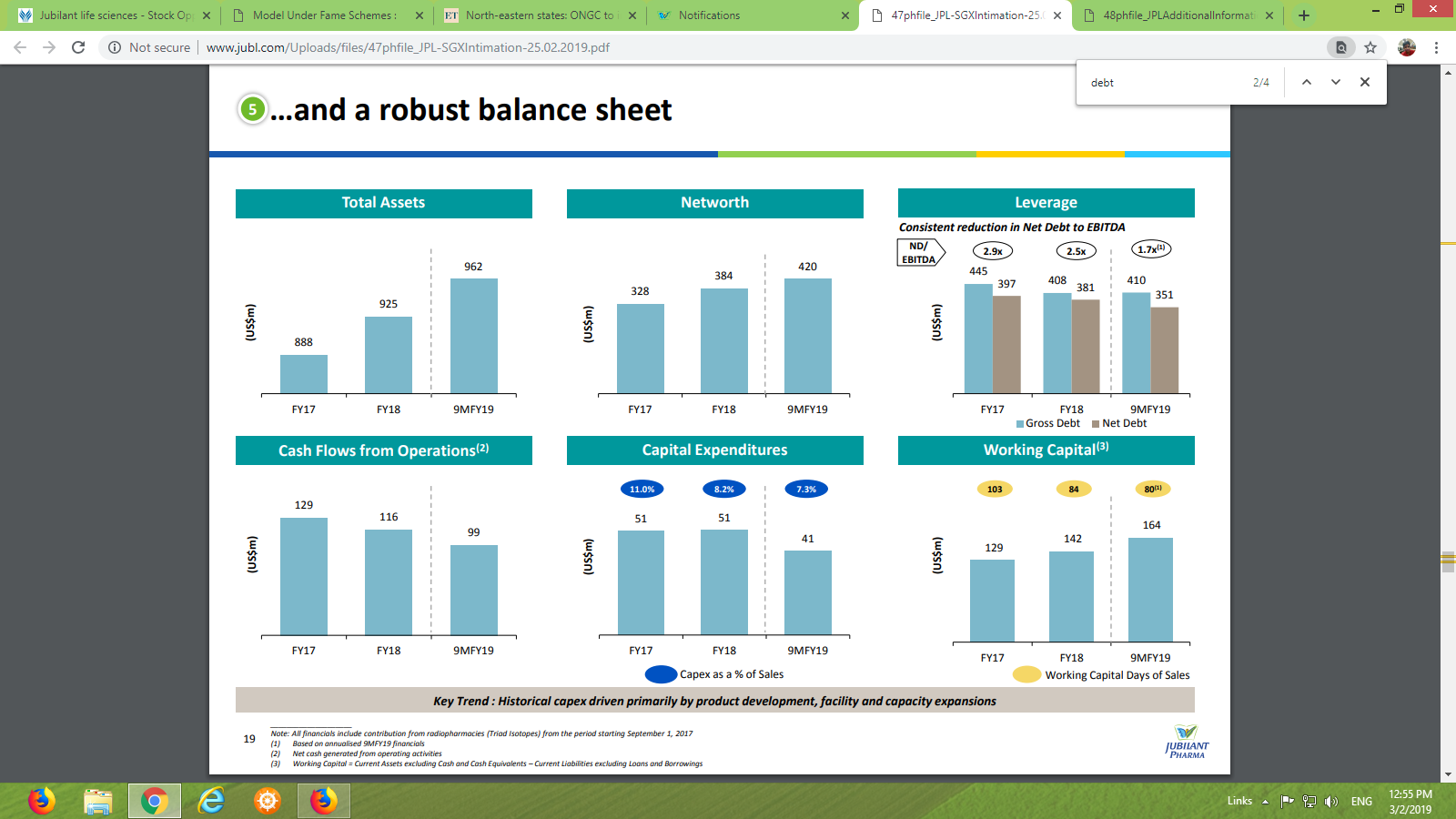

Leverage graph showing net debt to ebitda ratio improved to 1.7x from 2.9x for FY17 & 2.5X for FY 18.Also, 72% of the revenue is now $ denominated…providing hedge against currency headwinds… I think Jubilant Pharma IPO will be game changer in term of debt reduction but why management is delaying it not known…

I agree few years back they borrowed heavily to acquire businesses in North America but they have handsomely turned around the businesses they have acquired and now they have good cash flow from them…like USD $255Mn DRAXIS Health Inc. acquisition in radiopharma space…its proving to be cash cow for them.Also USD $ 122Mn acquisition of Hollister-Stier Laboratories LLC in CMO space…Again last year they acquired Triad isotopes which has second largest radiopharmacy network is USA, through internal accruals with no increse in debt. This network strategically fit for Jubilant to distribute their products…I think next few quarters are interesting for the company…especially radio/nuclear and CMO part of there business…If they maintain growth and manage debt we’ll have altogther new Jubilant.

Discl. Invested…hence views maybe biased.

3 Likes

US FDA Issues warning letter to Roorkee plant

JUBILANT EMPLOYEES WELFARE TRUST sold 3484229 shares of Jubilant life worth Rs.272.46/- Cr through bulk deal on NSE…Will senior members of the valuepicker throw some light why trust raise so much of amount?

Also, though there is name of seller on bulk deal data on nse website, buyers details are missing…isn’t it mandatory to disclose name of buyer in such a large deal?

Disc. Invested.