Hoping for a good result tomorrow and that should pump some steam into the stock price. However, am curious to know the rationale as to why company choose to do an investor presentation (later submitted to bse) to large number of DIIs before result, why not do after the results… are the results not good or ?? - though there are other companies that have done this as well.

Good results posted . looking better ahead

I found the below on one of the site which said they would make their capacity fungible for diff SKUs but unable to find it in company AR. Can anyone throw light on this if they have any info.

New Capex : As outlined by management, they are facing a double problem – on one side they are still underutilized on total capacity and on the other hand this capacity is not fungible hence they cannot take up multiple SKUs from clients. The retrofitting on new equipment on existing plants and new capacity coming on stream should solve both problem

Good turnaround Q3 results

Sales & profits are almost doubled YOY at standalone level.

http://www.bseindia.com/xml-data/corpfiling/AttachLive/4c901fa8-039f-46ba-9e19-7dcb790e7de2.pdf

What is your view on the qualification quoted by Auditors in the results ?

Sorry, i dont have much details on this but i would like to wait for concall for more clarity on the growth prospects and other info.

What is this obsession of the management to issue Pref shares\warrant and make quick money … This happens often when company has some positive business developments. Does the management think that they deserve bigger pie of the fortune which makes them behave this way. Fail to understand the logic of issuing Pref shares\warrants @ 11… Is management integrity a problem here

1 Like

Have they done it again in OND quarter or are you referring to the old news?

2 Likes

So a Oral care contract manufacturer now wants to open retail stores for Patanjali, quite wild idea!!!

He also wants to expand contract manufacturing to other FMCG categories (I guess its better to focus energy on oral care where they hardly have 1% market share!!). But wait a minute what does it has to with retail stores??!!

He predicts more than 30% growth in foreseeable future in current business but still wants to grow inorganically as well, I guess 30-35% growth was too small from JHS standards!!

Bottom line is JHS got some excess capital and they just want to splurge on pet projects.

I have small quantities of JHS, looking to sell based on these wild ideas.

1 Like

I also have the same feeling about Mr. Nanda. And, i think this company has lost track of what they were doing earlier. Retailing for Patanjali ? Maybe, they have other products in mind.

I think if this stock comes in 40-50 range, maybe it will not be a bad idea to buy.

I think it has a certain intrinsic value.

And, there is usually a price below which promoters step in to support the stock. So, that range could be considered safe for long term investment.

And, if everything goes as per their growth projections, the stock can offer good returns as well.

1 Like

dear members this is stock is continuously making new low what may be the reason please guide somebody

ROA will be affected in the near term due to their new investment plan hence investor are off loading. Growth prospect remain good for this company along with more assembly lines are coming up. So long term aspect remain very good if this stock gets corrected to 50 level will be a very good opportunity to buy. I am holding this one and willing to add more in dip.

2 Likes

Nikhil Vora makes some interesting point on FMCG manufacturers link

There is a plethora of options in the back-end space yet to be explored, according to Vora. It’s untapped and considered “non-glamorous and non-sexy” for people to invest capital in. These companies are set to become “large and dominant”, he said. That’s why Sixth Sense invested in oral care products maker JHS Svendgaard Laboratories Ltd. and breakfast cereal maker Hindustan Foods Ltd.—both contract manufacturers.

However, the key negatives off late, far outweigh any positives

-

Strong BJP Affiliation for Nikhil Nanda in all social media posts link

Furthermore the official JHS handle is retweeting these political tweets. link

-

Poor Capital Allocation decision in planning 100 Patanjali stores across airports link

The plan is to set up 100 stores over the next two years depending on availability at airports, Nanda said. The first such store was opened at New Delhi’s T2 terminal at Indira Gandhi International Airport.

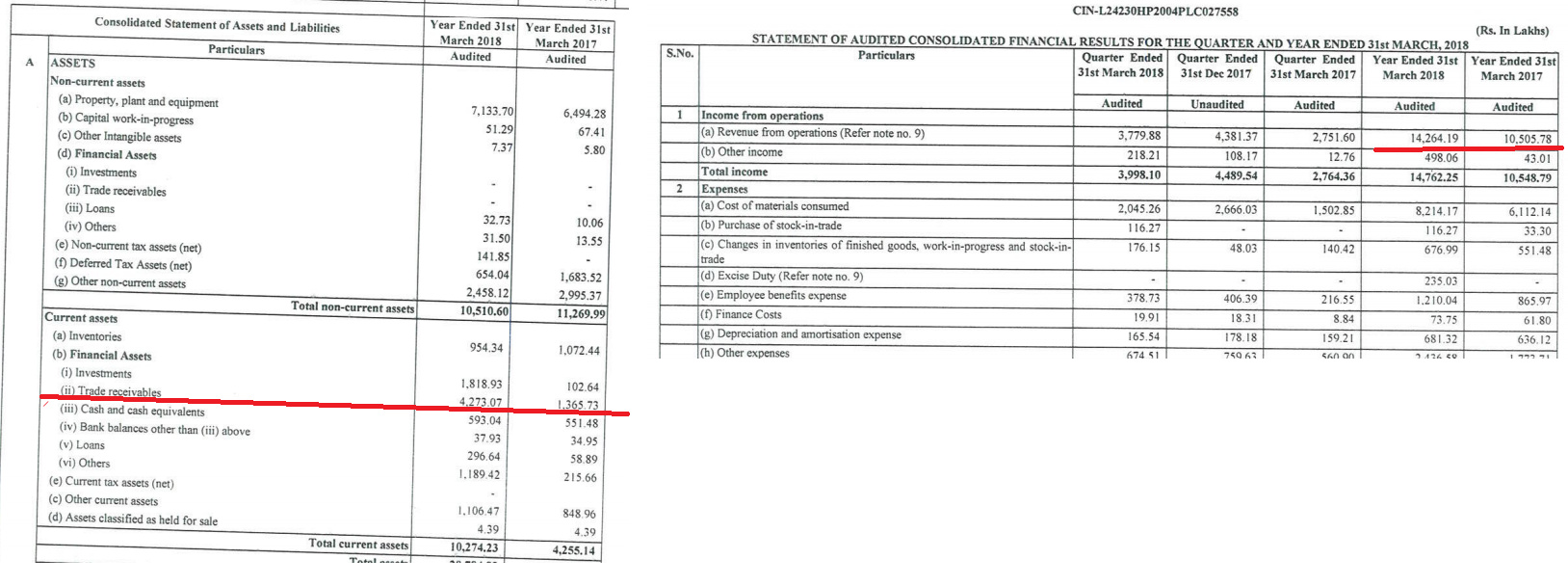

- Increasing receivables, 28% of annual sales or almost 3.4 months sales are outstanding. Huge negative

- Over optimistic projections and lofty targets in media interviews from Nikhil Nanda

3 Likes

The company is losing focus. He is setting up retail stores in airport for Patanjali, whose revenues are falling already. He is not even sharing how they are planning to share profits. He is saying it will improve the relations with Patanjali. Won’t it affect the relationship with other customers? The relationship with Patanjali might be good for his political career but that doesn’t justify him spending JHS money for setting up stores for Patanjali.

I have removed JHS from my watchlist.

2 Likes