This is a know problem with almost all listed companies - minority shareholders get the “lemon”

Almost all the companies go for one to one discussions with large investors and inform the sock exchange about it. However the information provided to them is not disseminated through the stock exchange for the benefit of all the shareholders. These large investors are thus privy to the certain confidential information and make their investment decisions based there on. It is a clear case of INSIDER TRADING but surprisingly it is officially recognised.

Let us hope that the regulatory authority wakes up…

While there is no denying that these kind of lofty projections do create a sort of optimism in the investment community, we would be better off if we take such projections with a pinch of salt. I am in no way arguing that they won’t be able to achieve those targets but past experience (e.g. in Kelton Tech) has taught me it is always prudent to first let the management walk the talk and then act upon even if it means buying at a little higher price. If one is lucky one may even get the corrections in between to act upon post judging the results of actions of Management.

Discl: Invested (small proportion), no transaction in scrip in last 3 months

3 Likes

This is turning into a good story.

Has any one tried their products?

Can we have a scuttlebutt response about the products?

Slowly this is turning out to be good one.

Criticism is invited.

Prasad.

1 Like

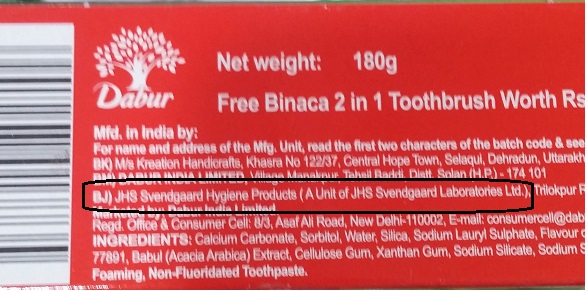

Some of the Dabur toothpaste is being manufactured by JHS

1 Like

I am still looking for what is the opportunity size in oral business and market size of JHS.

Is client like dabur, patanali getting the paste/brush from only JHS or there are others as well?

The company has revenue of (approx) 100 cr and operating profit of approx. 5 cr. Their net profit was boosted by tax incentive (16 cr), some of them are about to expire in FY18 and most of them will expire by Fy20. I think their effective tax was also lower in F17, due to accumulated losses. However, this should revert to normal in a year or two.

Their private portfolio is 14 cr last year, which has grown from 6.5cr (Fy 15) to 14 cr in FY 17. In next two/three year, they want the private label to contribute more than 50%, which is great. As per the latest annual report, they provide private label against cash and managed to grow it at a handsome rate, which shows product strength.

It seems Nikhil Vohara is dressing up a company in a way investors, in general, want to hear. As a result, the stock is on fire and has gained more than 6/7 times in last two years.

While the company has good future, the stock is running ahead of time in my view. It is 3 times sales, and 50+ times operating profit (if I take out the tax benefits), after all, it is still a contract manufactures and will likely to be so in near to medium term.

3 Likes

sixth sense india oppurtunities sold approx 2.2 lakh shares yesterday

Nikhil Vora is on the board of JHS - wonder why he sold?

sixth sense has 30lacs shares…and most of them at 11rs… a bit of profit booking as always prudent…not sure why they sold only 2 lacs though…

market cap to sales is 3 times agree but it will be going down qrtr on qrtr. Revenue wise they are speeding up very rapidly.Even after the GST hickups last quarter they we able to clock a 15 % rev growth. The management have already given a guidance of 20-30% rev growth this year. I think they can easily achieve that given a strong order flow from patanjali . 2 new clients have been added as per the management in the latest disclosure. I think going forward we need to see the margins which it is able to achieve through its own products and contract product mix.

30 lakh shares owned by sixth sense and 35 lakh shares owned by VORA CHAITALI NIKHIL

1 Like

If you are following Safir Anand on twitter: he did tweet a picture of himself at their Ambala Factory (albeit there was no factory picture). I understand it was a Factory visit. Safir is quite respected investor, has on multiple forms talked abt JHS.

Discl: Invested

Hi All,

Anybody can comment on the share capital increase in the company, they have almost doubled the share capital in 2 years?

1 Like

I am quite keen to understand your comment regards “…it is still a contract manufacturer…” From various interviews of Mr. Nanda MD - JHS I infer that they control the design aspect of the toothbrush and it tends to become JHS’s copyright. It is therefore quite a few steps ahead of being a converter. IMHO this value addition is something market should be willing to give a multiple.

Seems it has come to the wrong Parag

The NP declared has some 25 odd crores of one time other income… Deducting

that, is the current price not too over exuberant ??

I personally think it is unlikely that an MNC will involve an Indian company- and that too contract manufacturer- to design their product.

However, JHS may have helped Indian companies like Patanjali in designing the toothbrush.

The critical point – in my view is not only design- it is marketing and reach. MNC’s and big Indian players have massive advertising budget as well as market reach to distribute their product, which won’t be easy to match for JHS. E-commerce (Amazon and others) are providing a level playing field and allowing JHS to sell directly to the consumer, but it won’t be easy and they themselves may (I am tempted to say will ) be strong competitor

We know MNC (Colgate) and MNC manufacturers oral products, but every other departmental store (Future group, D mart) along with e-commerce player is or will manufacture their private label. Also, Amazon and other e-commerce players will also manufacture their own product. So the competition will be huge.

How much profit are they able to generate in future will their price in a medium term? At the current profitability level and the price does not offer a margin of safety.

This reminds me of a quote from quote from Benjamin Graham-“Good investment ideas cause more investment mischiefs than bad one”.

I am not saying this is a bad one or they will suffer in future. Just that share price has risen multiple times in last 12 months make me cautious.

Dear friends I have checked jhs product on Amazon .they are charging 50rs to deliver product.this will be a hindrence on reflex buying.i think they should give free delivery and cash on delivery option.

I think this is Amazon’s policy for all orders less than Rs. 599. Any order less than Rs. 599 is charged minimum Rs. 50 delivery charge.

I think Aquawhite’s main business will come from big retail chains or local mom and pop stores as I don’t think people go to Amazon for small items like these. These seem like impulse purchases while at Big Bazaar, etc.

Disclosure: Not invested but tracking.

3 Likes