I am starting a new thread on Jash Engineering…

Find it really interesting and am waiting for insights from other members.

This company got listed in October 2017…

http://www.jashindia.com/ =They have been in this industry for 60 years.

Sound management - please let me know if that is not the case…

It is a leading manufacturer of water and sewage treatment equipment, plans to raise ₹58 crore through an initial public offering (IPO) on the NSE Emerge, the SME platform of the NSE.

The company’s products are approved by major municipal corporations, sewerage boards, consultants and large engineering, procurement and construction (EPC) companies in India and over 25 other countries such as the US, the UK, West Asia, Hong Kong, Singapore and Malaysia.

The company boasts clients such as NTPC, BHEL, L&T and SAIL and has four modern manufacturing facilities in Central India.

The company issued 40 lakh shares through the IPO in a price band of ₹115-120 a share. The IPO comprised a fresh issue of 22.60 lakh shares and an offer-for-sale of 17.40 lakh shares.

Link intime were the registrars to the issue. http://www.linkintime.co.in

https://www.youtube.com/watch?v=xPjAixzfLvc = the IPO video =It is in HINDI.

Out of the ₹58-crore IPO, the company will use ₹23 crore for capital expenditure and working capital purposes and ₹4 crore for general corporate purposes; ₹31 crore would be mopped up through the OFS = AS PER THE RHP.

L D Amin, Chairman, said through a series of acquisitions and technical joint ventures, the company has created a strong revenue growth in the international market such as West Asia and the US and has transformed Jash into a global player in water control gates, screens and valves industry.

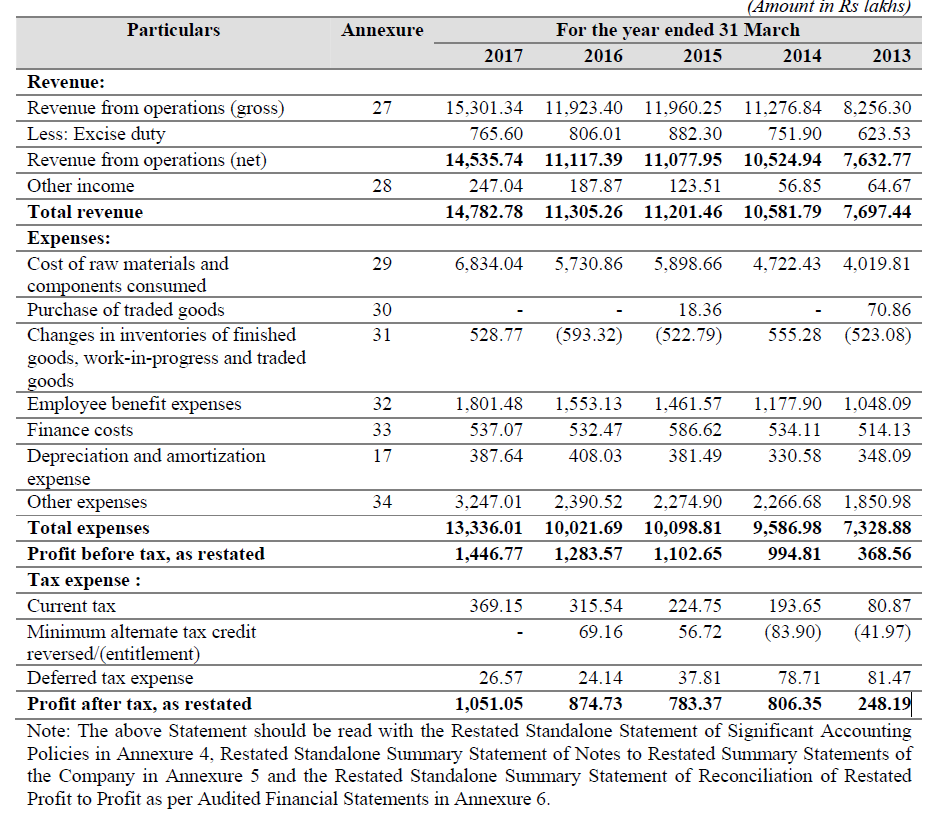

The company registered revenue of ₹161 crore last fiscal.

CHECK THE PRESENTATION HERE:

or here: https://www.youtube.com/watch?v=uIlWVRlkpGg

Claims they have 70% plus market share for watergates. Exports to 30 countries worldwide and has subsidiaries in 4 countries.

They have a US subsidiary= http://www.jashusa.com/

Acquired Mahr Maschinenbau -Austria and has 10 other international tie-ups.Check the presentation.

Some questions:

- has anyone met the company promoters and can shed more lightstrong text

- What is the market size and margins for the various products they manufacture: Water control gates, Mechanized screening systems, Screening conveying and washing systems, Knife gate valves, Water hammer control valves, Energy dissipating valves, Archimedes screw pumps, Micro hydro turbines, Clarifiers, Clariflocculators, Flash Mixers, Degritters, Aerators, Thickeners, Gravity Decanters, Trickling Filters, Digester Mixers, DAF Units and solid handling valves

- I have the projections which I have based on my understanding? Has anyone tried to analyze their results and carried out some estimates

- Is there any broking report or research report on Jash Engineering

Not invested.