Came across this news and found relevant for the group.

Floating wind farms are being tried in other parts of the world.

Came across this news and found relevant for the group.

Floating wind farms are being tried in other parts of the world.

Does anyone here know about the on ground preparedness of the various OEMs wrt implementing the projects.

Are players like suzlon and gamesa at an advantage due to their long-standing India operations?

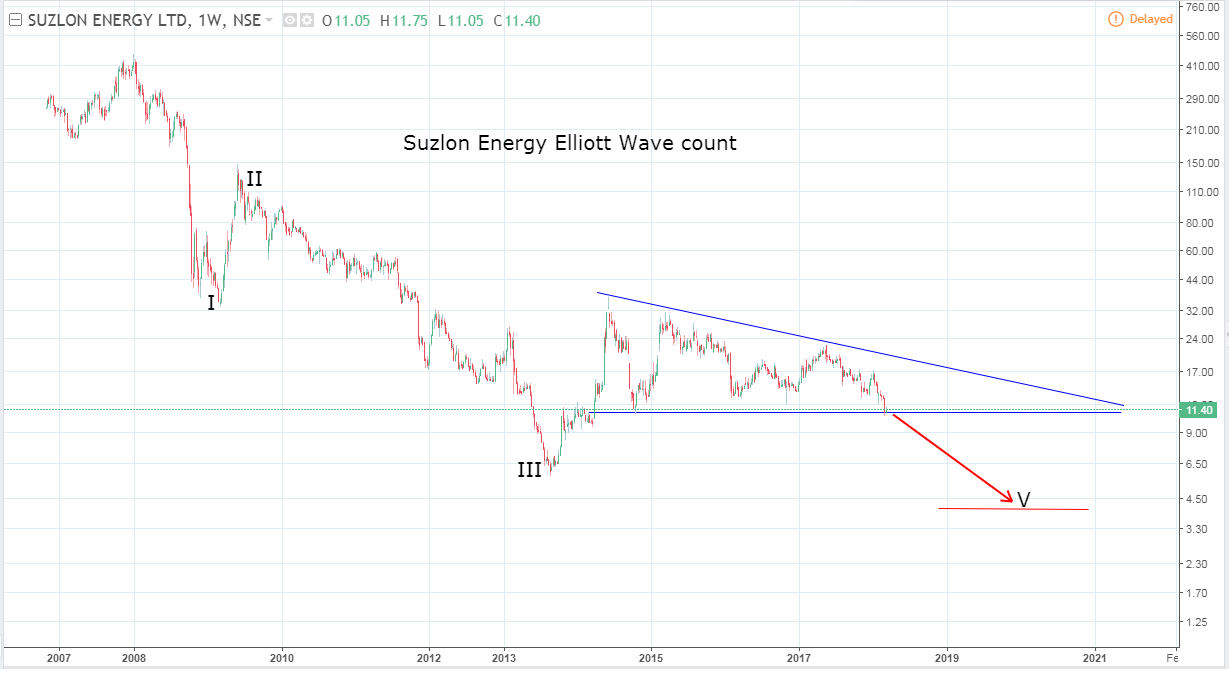

@Mehnazfatima Suzlon seems to have made a long legged doji in today’s fall… it is also at the channel botttom… does the chart look interesting to you? Also, any further views on the potential on the business side, with heavy auctioning going on…

rgds

Ankit

I am disappointed with the fall in march because from April onwards it’s the beginning of a new era for wind players. But I am holding on to my investments in suzlon. This sort of price we may not see again. Suzlon may execute more than 2300mw of wind energy for fy19 and earn around 2-2.5 rupees eps.

In their latest investor presentation, inox has shown calculations that show good rate of returns for IPPs even at a tariff of 2.5 rupees per unit. They have taken per mw wtg cost of 6.5 crores. Those who worry about margins for inox and Suzlon should go through those calculations.

Inox seems to be the most desperate WTG player. They matched the lowest bid in SEC1 and also bid low in SEC2 auction to bag some capacity. Now Inox has clearly said they are not looking to do more than 1 GW this year. Thus new capacity auctions would go to Suzlon and Gamesa. That is why they didn’t care about low price auctions. Some people think WTG manufacturers have no leverage but fact is that total manufacturing capacity in India is 12GW and if 10 GW is to be done each year, that means IPPs will have to go to Gamesa and Suzlon. I believe that’s why auction prices are going up now.

There is another way of looking at it. If one buys all the three players in equal proportion- Suzlon, inox and sanghvi then effectively the risk is eliminated from portfolio. Such a strategy would enable investors to invest a bulk of t heir portfolio in wind energy stocks with very less risk and great upside potential

I had tried such a strategy in sugar stocks. Results were quite good.

Some would say its risky, i say it reduces risk.

Elliott Wave super degree cycle suggests there is more downside. There may be short-term upside moves (caused by cycle degree corrective moves) but in long-term, I see downside, unless we get a truncated 5th wave. In that case, stock will take a complete U turn and start behaving bullish. This first wave of the first grandsuper cycle will complete in another 3 years.

Currently descending triangle is going to break out (99.9% downwards breakout). Since it’s a long-term chart, even the breakout may happen in a span of few months. Here’s the chart.

It’s not leading/ending diagonal. It’s horizontal triangle (descending). In leading diagonal, both the trend lines (formed by connecting peaks, and by connecting troughs) will be in the same trend, either uptrend or downtrend. In horizontal triangles, one of them will be flat (i.e. ascending or descending triangle) or both of them in different trend (i.e. symmetric triangle or expanding triangle). Horizontal triangles usually appear in the 4th or B Elliott wave positions. Here in the long-term chart, it’s appearing in the 4th Elliott wave. Also for horizontal triangles, the internal wave count is 3-3-3-3-3. It’s the case here. Whereas for leading/ending diagonal triangles, the internal wave count should be 5-3-5-3-5. That’s why diagonal triangles advance in one direction.

Hello PE_Ratio! thanks for your response… And agree with your observation, however this is how it appeared to me in smaller fractals when i drew the first chart above… to your point of truncation, yes because of Divergence, i’m of the view that the 5th wave was truncated, post which the LD started, which has crossed 78.6% Fibonacci Support mark and now staring at 81% mark which can give a possible end of 2 … looking forward for your inputs on this.

A fairly detailed and good article on the wind industry - what went wrong and expectations going forward:

Infact, the latest press release from Sanghvi Movers along with Dec results - https://www.bseindia.com/xml-data/corpfiling/AttachHis/66440d94-4d84-48c7-a1de-588d6d7ec157.pdf gives a good overview of the industry. As per these articles, things have been better for the industry for this March quarter given the recent auctions by government.

Can anyone throw some light on the attached news bite which appeared today? Are these order wins already reflected in their order book shared in Q3 update?

This now takes the order book to 1640mw

Hi Ayush,

Wouldnt we be better off playing the theme through Sanghvi Movers than a Suzlon/Inox Wind.

With the Auction regime, the days of supernormal profits for IPP’s are almost over.

.

Govt promising 10giga watts of wind power auctions in fy19

https://cleantechnica.com/2018/04/02/indian-state-to-launch-3-gigawatts-of-solar-wind-tenders-soon/

tariffs rising in the latest SECI 4 auction…

Pls take the calculations in INOX ppt with a pinch of salt. These are simplistic calculations and the financial models used by IPPs are much more complex. The 12% IRR in INOX ppt is pre tax and pre depreciation. Whereas IPPs look for post tax, post depreciation returns. What I am indicating here is that to arrive at same returns after accomodating tax and depreciation, INOX may have to reduce price of turbine and/or O&M. Alternately IPP will have to reduce benchmark IRR.

Having said this, IPPs are mainly keen on Equity IRR and project IRR should be greater than their cost of debt. Typically, the benchmark is post tax Project IRR of 11-12% and Post tax equity IRR of 15%.

If Inox is able to bring in investors for the projects it has won under IPP (which should be possible as per economics), it will be able to sell at a slightly higher price compared to projects which are won by other IPPs or Inox where they are just WTG suppliers (and installation). Because Inox has won these projects, it may have a slight upper hand.

I am yet to study SECI tender document to confirm for myself if the projects won by an IPP can be sold. In past there have been restrictions on sale of solar projects under SECI. Unless this is ascertained, there will be an element of risk. What if the projects cannot be sold for ‘x’ years ?

Further, it might become difficult to secure debt with the current NPA stress in banking system. Not many banks provide debt to IPPs for renewable energy projects. Most Pvt sector banks do not (maybe Yes Bank and L&T finance will). IDFC is not keen unless it is a operating wind asset. ICICI and Axis do not and will not given their current mess. REC, PFC are not known to be quick and take several months. This will also adversely impact cost of debt and hence project IRRs. Accordingly, I see financial closure as a risk and will be keen to understand the developments on that front

With all the negativity here come one effecting news