This company went to major problems by buying overseas business and struggled the last decade, now they sold that and slowly turning around, by seeing the results and euphoria(???).

Can someone who is closely following and expert on debt and FCCB, please explain how they r going to repay them in the coming years so that v have a clear picture; how they survive like if they don’t get enough orders or competition or again buying other business???

Any input regarding specific timeline/plan for CDR exit? Did mgmt provide any clue in this regard? What about actual applicable GST rates for the sector vis-a-vis current and expected?

Nice contrasting viewpoints. Arguments in this thread range from

Turnarounds are a farce

This is not a turnaround because it was aided by policy

Even other companies in the sector have also done well.

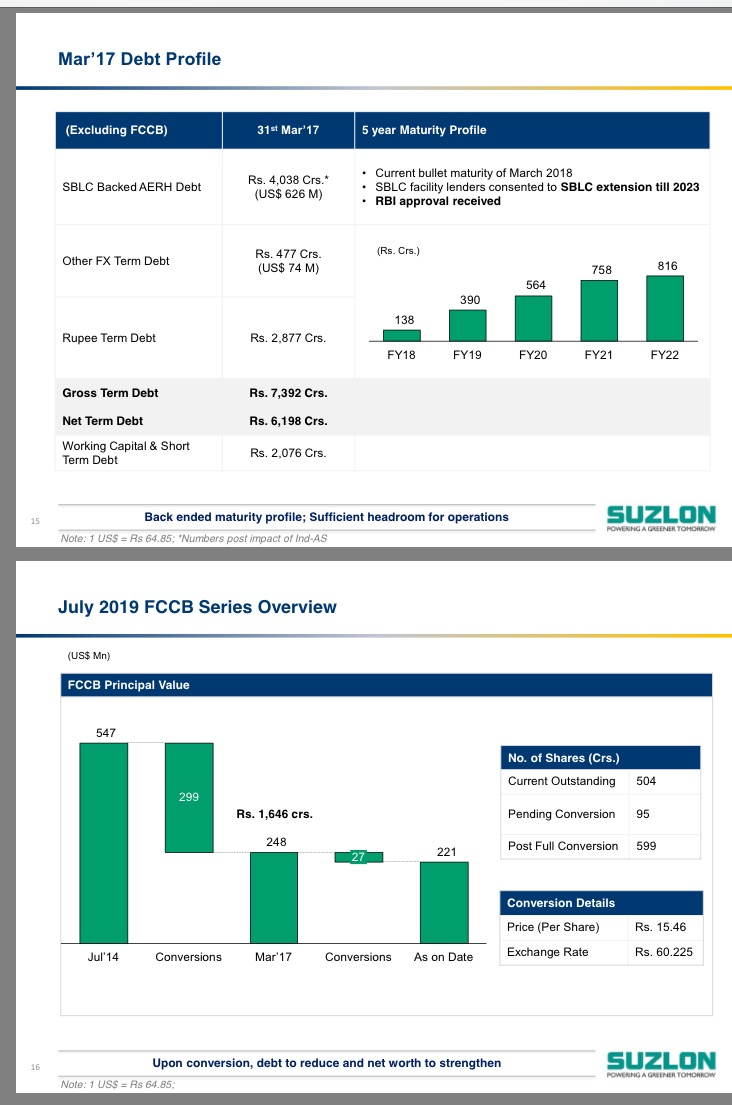

Oh the debt! What about the debt?(??)

They bought and got burnt with Senvion and sold and extinguished part of the debt - Yes. They have had three quarters in the green so the turnaround is confirmed I would assume, especially with a healthy order book and sectoral outlook. If not, perhaps I don’t understand what a turnaround is.

Am no expert but I can try. They have a long term debt of Rs.6,198 Crores. This is apart from the FCCBs. They are back-ended payments (Chart in your post). They are currently doing sales of Rs.14,000 Crores and an EBIT of Rs.3000 Crores on that roughly. Does that debt still sound daunting over a period of 5 years?

As for FCCB’s, 500 Crore shares are going to go up to 600 Crore shares. I think this is already around 506 Crore shares. Dilution is constantly in the picture in EPS calculations and no one is ignoring that.

Let’s not misunderstand Suzlon for a steady compounder or a stellar business you would want to hold for years to come. This is a turnaround value trade, and has been since late last year. Horses for courses.

Absolutely! Without the tailwinds, the turnaround would never have materialised. Without a competent management that opportunity may have gone a-begging.

I beg to differ here. Suzlon has done poorly against Power - BSE by your chart. See the dip through 2016. That’s the turnaround we are talking about.

Sanghvi movers is bound to move with the wind sector as 80% of their revenues is from there if am not mistaken. I don’t see the relevance of it in the context of Suzlon being a turnaround or otherwise. No one is claiming that the management conjured a turnaround against govt policy and all the odds.

Disclosure: Invested and will remain invested until sectoral headwinds emerge or the stock turns expensive or the winds stop blowing.

Contrarian views are not only welcome but encouraged.

Another point which will certainly be a factor if you are a trader focused more on the price volume action is the sheer amount of supply of outstanding suzlon shares. It has more than 5000 million shares outstanding.

The point is that the change in perception about the earnings of suzlon will at a practical level translate into demand for suzlon shares which has to overcome the supply of shares.

This make it even more important to focus on the prospects of the business for individual investors esp in companies with a mammoth amount of shares outstanding.

It would require a huge structural change in the earning power of suzlon extending well into the future for demand to overcome supply.

It was despite the float that the price moved 50% in the last 4 months from Rs.13 to Rs.20 in first gear. I expect it to continue to do so, hopefully in a higher gear. It is a slow but steady progress which at no point felt too “expensive”, unlike the rest of the market during the period. Right now mutual funds holding is only 1% but there was a healthy interest from top fund houses in the concall post results. Let’s see.

Dear @bheeshma , I appreciate your efforts with the comparative charts. I rate your charting skills very high and try learning from your charts more often that you would know. The points you make are also valid. I agree that Suzlon’s performance has mainly come from the sectoral tailwinds. Also, I do not challenge your views on the price action as you have clearly demonstrated its movement in line with the power index. Lastly, I also agree with you that the rally in prices during Jan-May 2017 may have already factored in the current fundamentals. In fact I would not even comment on Monday’s stock movement as it might be subdued despite the euphoric targets expected by everyone. Having said that, I would like to go beyond…From the clutter of short term price movement and quarterly numbers, lets look at Suzlon from a long-term strategic standpoint. Thats where I feel the real unlocking of value is going to happen. And that is what will set Suzlon apart in the longer run from its peers. My investment thesis is based upon three premises which I would like to present for the benefit of all and would like to get counter perspectives or loopholes. Since the document got a bit longer than I expected it to be, I thought a pdf file in attachment would be good. So please read it and share your thoughts…Cheers Suzlon - An investment case.pdf (89.6 KB)

You have done a comprehensive analysis and presented various scenarios. But I think it would have been better had you included one more element in your analysis.

There are three things which eat up a companies earnings…depreciation, debt / interest payment and finally taxes. You have omitted the impact of taxation.

As clarified by J.P Chalsani in earlier concall…Suzlon wont by paying any taxes for the next 4-5 years. This is on account of its accumulated losses earlier. Hence, this aspect contributes to a good jump in eps of suzlon going forward. As debt is reduced and no tax is deducted from earnings…Suzlon may see a good jump in eps in FY 2019.

Since market is an advance discounting mechanism…I think the stock price will first go up significantly in the next 12-18 months and thereafter, there will be longish consolidation period where the price waits for the earnings to rise and catch up…

While the market participants and brokerages envisage a rise in stock price which is back ended, I am more inclined towards the view that the rise in price will precede the rise in eps…I am more bullish on suzlon in the next 12 months…and after that expect a 3-4 quarters of sideways movement…just like what we have seen in some other stocks such as spice jet, Chennai petroleum,escorts, kec international, titagarh wagons, beml…and a host of other stocks.

By getting caught in the minute details abd micro analysis, Investors are missing the bigger picture. Renewable energy, without any incentives (such as GBI or AD) has emerged more competitive and efficient than thermal power…in India as well as globally. And this is just the beginning…better designed and more efficient products are in the pipeline. This will tilt the balance more and more in favour of renewables vis a vis thermal energy. Furthermore, in renewables there are no uncertainities in the form of cost escalation, land acquisition, environmental clearance, coal linkage etc.

It is almost as if we are witnessing a revolution in energy sector…and Suzlon is a good enough company to get exposure to this second green revolution which is noe underway.

Taxation point is well taken. The other players would be facing reduced accelerated depreciation (from 80% to 40%) and GST rate of 5%. Both in effect would increase their tax liability. Suzlon benefits as they can carry forward their previous year losses for coming 8 years. JPC was bullish when he said that all reported losses would be covered within 4-5 years.

May be you are right with your 12-18 months target if it is the momentum play you are after. It also depends on what your 18 month target is and how your exit strategy will pan out. The price action as I have mentioned in 12-18 months would depend upon several factors - PE assigned (debt factor), impact on margins, high free float, FCCB sell offs, political mood etc. My case, however, is focused on value unlocking through long term strategy play. Suzlon would need more than 18 months to pull all levers to grow. I believe that if there is no significant change in macro-economic factors and if Suzlon continues to execute its current plan, then it will be debt-free, among top 5-6 global players,and a part of Nifty 50; all this by 2023. It seems a very bullish call at the moment but not an unrealistic one.

I had highlighted the Indian stance on ‘the reciprocity in dealing with foreign players who do not allow Indian companies in their domestic geographies’ in my case. This is an example of it…

A formal office memorandum, expected in a month, will insulate the power transmission sector from companies based in countries that do not allow Indian entities in similar projects, a senior power ministry official told ET.The restriction will be gradually extended to the power generation and distribution sectors as well.

Very nice write up @Nolan! I have also been tracking and have been invested in Suzlon and agree with your assessment.

Its turning out to be a very interesting case where a company which was totally written off and bankrupt has been making a strong comeback. Specially at a time when there are some headwinds to the sector. Its interesting to see the contrasting difference in commentary of Inox and Suzlon and this gives more confidence for now.

By headwinds i mean - withdrawal/reduction of incentives and the greater attractiveness of solar sector. The way the rates have fallen, this could disrupt the wind sector.

Solar PV cells are at 18% GST slab. I think this will pretty much even out price falls in solar cells for the next year or two so those aggressive bids of Rs.2.44 per unit and so on may not be the norm going forward which will put Wind on a somewhat even footing. Once the hybrid policy gathers steam, Suzlon will stand to gain the most out of all renewable players.

Dear @ayushmit I hold a different opinion here. Please consider my views on the points you have raised:

1.Reduction in incentives / Falling prices – Reduction in incentive shows that the industry is stepping out of infancy and does not require government support anymore. Going by the concept of Industry Life Cycle, it seems that the renewable industry is set to enter into a growth phase where the volumes will surge exponentially. Now when the volumes are high, the customers have the bargaining power to negotiate better rates/prices. So prices go down. But the loss of price margin gets ‘over’-compensated by a greater volume growth. Because the law of demand says that ‘as the price goes down, demand/volume further increases’. The real impact of this transition will be seen only at the company level where the companies having more efficient operations (lower costs) emerge as beneficiaries over companies who are less efficient. It’s a common evolution process every industry goes through its life cycle which at the company level separates the wheat from the chaff. Hence incentives removal/reduction and pricing change would only increase the size of the wind energy sector. Suzlon will benefit from these measures due to its low cost leadership. Inox may lose unless they take some hard decisions quickly (of which I’ll share my views separately for the benefit of Inox investors.)

2. Wind Vs Solar – I think industry experts have two ways of looking at this issue. Some say that renewable sector is a debate about solar ‘OR’ wind. Others say that there is no debate because its solar ‘AND’ wind. I say that India will take it from wherever it comes (solar, wind or even hydel). Renewables industry in India is having a giant target to achieve (175GW) and they are running on a very tight schedule (2022). If Modiji wants to keep his promise to Obama (US) and if he wants to improve India’s ranking as an investment destination (for his Make in India initiative), then he cannot afford to procrastinate on critical infrastructure issues like power, roads & transportation etc… Secondly, the wind energy technology (due to lower LCOEs) and GST taxation would act as a balancing factors between solar and wind. Lastly, in a matter of 2-3 years the competitive scope for Suzlon will change from local to global, where this debate would lose relevance.

Hi everyone, I have been closely following this thread. As I am new here, and studied finance, global trade, macro economics and renewable energy as a subject recently, Suzlon came to me as an interesting case study both from academic discussion POV and from investment POV.

I really appreciate everyone’s effort here, for this very well mannered, data driven discussion here,taking both fundamentally and technical points into consideration.

I was waiting for the annual results to arrive, however, I do not conviction on my analysis till now, but I am steadily building it with help of this forum.

The annual result looks promising. Next 1 year will be very cruical for Suzlon, then it will be used for case discussion for a classic case of turn around.

Thanks every one!

Disc: Today I invested in Suzlon, hoping to hold it for a long time.