Results are a final testimony to much debated turnaround story. What was bullish is the wide representation from MFs and Brokers in the concall. They must all be considering their position now. The EPS is enough to drive Suzlon above 25 almost instantly but I would refrain from talking about the price action. What is more important is that Suzlon’s future in next 2-3 years seems secured.

CDR exit is the next milestone which seems only a matter of procedural compliance. The added responsibility going forward would be to act quick on strategic initiatives alongside managing day-to-day operations.

After CDR exit some other key strategic initiatives in the pipeline are:

Listing of subsidiaries to reduce debt

Expansion to overseas markets to grab offshore opportunities

Focus on hybrid solutions to capture solar synergies, and

Rolling out new product/s through R&D (which they suggest would improve the PLF further by another 10%)

If this plan is efficiently executed, then I reckon Suzlon would be among the finest case studies of corporate turnaround to be taught in Indian B-schools.

All these years forex was negative. Now its positive. So in a way it neutralizes their position. Macroeconomic factors are factored into pricing. So the price discount in last few years due forex losses would be compensated for now and henceforth. Besides, it reminds me of good furtune Mr. Modi had when oil prices tanked soon after he came to power. Reminds me of the adage ‘fortune favors the brave’.

Well result is good no doubt but not that great as it seems…

Look at the forex gain…

Also look at diluted EPS…

After subtracting forex gain calculate diluted EPS again…Then you will get actual numbers

Hi it will be interesting to see how the prices behave in the coming 2 or 3 weeks. It will also tell us a lot about how the market behaves. The context is of course that the suzlon turnaround story was anticipated well in advance by many market participants.

The key question to ask is whether prices have discounted the growth prospects? and if yes by how much?

This is the precise meeting point of technicals and fundamentals. if anything - suzlon is a case study on that.

@Akash_Padhiyar If you are comparing 2017 with 2016 numbers, then its not an apples to apple comparison as one month Senvion (divested subsidiary) performance was included in FY16 numbers. If you exclude those numbers, then probably you would see a fair growth in FY17 (with or without forex gains). Also, this year the company gave three excellent back to back quarters which confirms the turnaround robustly compared to last financial year.

The market was pricing in a turnaround but to the extent of an EPS of Rs.1 FY17E. Actual FY17 EPS is Rs.1.67 (Rs.1.57 Diluted). HDFC Sec research report had this at 90 paise with a price target of Rs.24. The actual EPS is 75% higher than estimate. In terms of TTM EPS, this could improve further after Q1 FY18 to about Rs.2 at least. Am not sure what P/E will be assigned but HDFC research reports are usually conservative so I would assume the price target will be revised by 75% which puts it at Rs.42.

FY18 is looking quite good as well with the order book already at around 1562 MW including 231 MW in solar. Contrast this with 1700 MW in FY17. Management sounds confident of doing about 2400 MW in FY18 which is 30% higher than FY17. This will mean an FY18 EPS of around Rs.2.40. Tanti confirmed multiple times that they have no issues with the order book. Contrast this with INOX Wind which says its order book of 1300 MW stands irrelevant as they were PPAs signed under the FIT regime.

Going forward, there are multiple triggers as well

CDR Exit should happen in the next couple of months.

Hiving off OMS and SE Forge business would unlock value and reduce debt which will further improve earnings.

Increase in market share looks imminent as Suzlon’s S111-120 turbines have a 40% PLF - the highest in India. With dropping unit costs, this will be a total game changer. Tanti already mentioned in the call today that almost all of the current orders will be using this turbine.

Eyeing the global market again to diversify.

So what is in the price is only a turnaround of getting to the green. This lush green, is definitely not priced in as my math above highlights.

The market has the final say on these matters. As far as suzlon goes i am more interested in the verdict of the market. At a personal level it is a great learning experience. I am eager to learn from the market than from tanti.

Lets not be so harsh on Tanti mate. Promoters do make mistakes, but how many have the resolve to make a comeback? That too by putting in personal wealth on the line? We have heard of companies like Kingfisher and Unitech and their promoters in India and Suzlon could have gone the same way. Irrespective of where Suzlon ends up, the promoters deserve respect for the pain and efforts taken in staging a turnaround of this magnitude. if the story turns out picture perfect, then (being a professor) I would definitely have a few lessons to teach my students.

suzlon offering windy land sites to bidders and signing exclusivity agreement along with pre bidding tie up… With those bidders most lkely to win in auction. After this the IPPs have to buy WTG from Suzlon only.

More than 80-85% of the order book of Suzlon is for the new WTG S111 120m…which has a PLF of around 40%. Except for Gamesa, nobody else has such a high plf product in India. Inox talks about a comparable product which is in the pipeline. But it takes atleast one year for it to be developed, installed and validated for a yearly performance. Till such a time Suzlon will dominate the field and may well capture 40% market share that it seeks. And by next year, when the competition comes up with a WTG similar to S111, Suzlon would already have moved ahead to S128 which is 10% more efficient than S111.

Suzlon has developed the product S111, tested it, validated it, and them installed production capacity for 1800 mw…Inox is still in development stage.

Thus the field now is clear for Suzlon…ADVANTAGE SUZLON

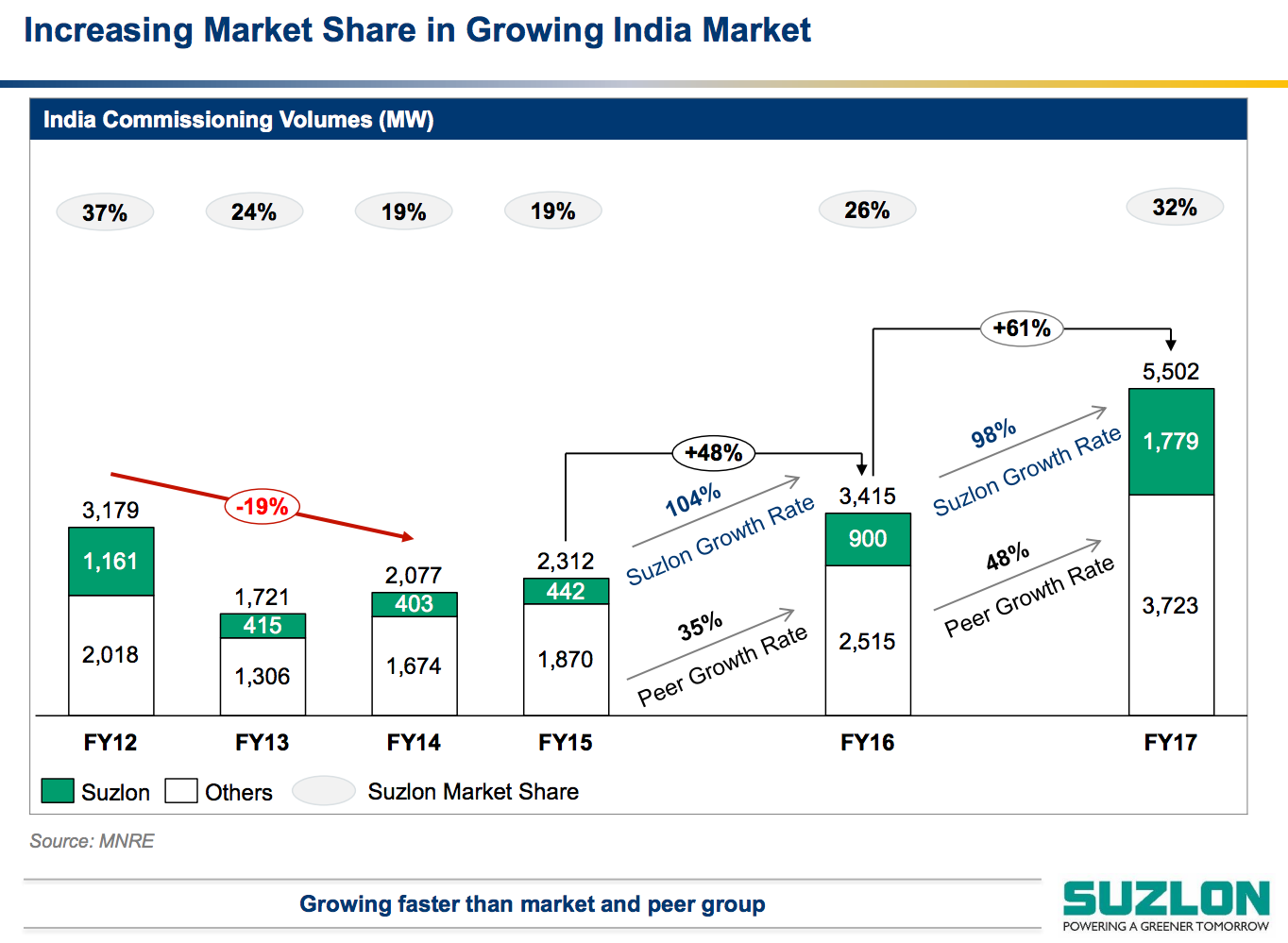

Absolutely true. To understand how feasible Suzlon’s claim to 40% market share is, just look at this trend. Suzlon has grown 104% and 98% in the last two years. Assuming 6GW commissioned volumes in FY18, Suzlon has to only grow at 30% (1779 MW to 2400MW) to get to 40% market share. Inox Wind is down and out in this battle, at least for FY18. Earlier it was Gamesa, Suzlon and Inox Wind which had 80% market share. Now its going to be Gamesa and Suzlon having 85% market share for FY18 due to falling unit prices and better PLF turbines that only these two possess.

Good set of numbers by Suzlon and turnaround seems to be on track. Revenue and Earnings are set to grow at fast pace in coming 2-3 years if they execute well.

One thing I find hard to assess is the amount of dilution we should expect in coming 2-4 years wrt FCCB conversions. Too much of dilution may result in lower EPS growth even though earnings grow rapidly.

What are your expectations about expected dilution? How should we look at it?

One basic question. I heard Suzlon is included in F&O but why there is upper and lower circuit limit. The reason I am asking is if it has to breach 21.75 52-week price, there is not much movement as Upper limit is 10% of today’s closing.

My sources in the power sector don’t have good things to say about the promoter. There was talk going around that they have just been channeling black money in the last few years. Though I can’t personally vouch for it, but my general feeling has been similar talking to some senior people in the industry.

Disc: Not invested and won’t till the current promoter is in charge.

With all the bullishness surrounding suzlon, there is a tendency to look at suzlon in isolation as a management turnaround. Some pictures are in order

Here is the yearly chart of suzlon compared to the BSE Power Index ( consists of 18 companies including suzlon - have attached the list at the end of this post)

It is bit of a chicken and egg situation. The sectoral tailwinds helped the management to turn the company around. At the same time, management had to get quite a few things right to take advantage of those tailwinds.

Disclosure: Not invested in Suzlon, but invested in Inox Wind.