Just came across a reasonable thread on the Embassy IPO

1 Like

Not evaluated the pros and cons yet. However, rental yields tend to be around 7% in commercial and capital appreciation is very slow if at all. Commercial real estate is doing well and there may be a case for peak rentals in the commercial space.

Commercial rentals (and hence rental yields) are more volatile in India compared to the rest of the world. That said there is an immense shortage of high grade commercial space in India and clients are sticky and willing to pay top dollar.

Everything put together it could a good investment for someone looking for 10-12% ROI over 10 years. Anything more than that is not sustainable in my view.

4 Likes

@valuestudent

Only point which need special attention in tweet thread is how is arriving at post interest yield of 6.5%? Point 24-29 twits. I believe from presentation made by the investment manager that yield are what would accrue to investor (pre tax) are around 8.5% for FY20. The difference in yield is substantial and need explanation. Either my understanding is incorrect or Mr. Manoj Nagpal has mis understood the key terms.

Discl: I would wait for REIT to listed and then observe and does not intend to participate in IPO. My view may be biased and my understanding may be incorrect. Investors shall do their own due diligence before making any decisions.

2 Likes

I read the RHP of Embassy REIT and am not able to reconcile a few figures. I think the whole yield calculation is based on the NDCF projections given in the document which for FY 19 seems to be at 1600 odd crores. I think this is from where the yield is being calculated by most people.

But I fail to reconcile the revenue and the NDCF numbers. For an entity with 2100 Cr odd estimated revenues in FY 19 and 80% EBITDA margins, the EBITDA comes to around 1700 Crores. From this EBITDA the company should repay external debt (8000 Cr - Pre IPO and 4000 Cr post IPO) and also bear the interest burden apart from paying Income Tax. So, the NDCF should ideally be around 1200 Cr. What am I missing ?

I don’t want to participate in any IPO - I don’t want to buy anything which is being sold to me by a group of more informed people.

I haven’t done any research on this, but I do feel that if I am a pure cash yield chasing investor I will not go for an IPO which are anyways priced to perfection in general (may be I am wrong here but I will be right more often) for a yield which is close to 7-8-9% which I am hearing. This is quite commonplace in India to India in several other areas as well.

So everything now comes down to the hidden number in a real estate deal - which is capital appreciation. This is one thing that one would need to pencil down better - a) what should one assume for land value appreciation, b) find out how much of fixed asset would be in the form of land - for taking a better call, c) Along with the building maintenance (every year) and d) big capex (maybe every 15-20 years) as these buildings worn out and e) the impact on rent on age as many new swanky buildings come up in the vicinity - all these are crucial points to ponder upon. Most importantly if their is rapid capital appreciation resulting in lower yields (when compared to current value) - are the trusts allowed to sell opportunistically and return back the capital to investors ?

Net net I am willing to wait for the story to unfold. Also crucially, as told to me by the CEO of a sponsor of a InvIT - the reason sponsers want to offload their running assets into trusts in the first place is that they don’t want their capital to be stuck for 8-10% when they can make much higher cash returns on their capital in their main business of construction - I feel the same when I compare these trusts with pure equities - however I am sure that for many of the general masses it’s a good diversification. Although I don’t believe they are as risk free as they are sold to be. Only time will tell.

3 Likes

4 Likes

Could collect the following information about Affle (India). Request experts and elders to give views and suggestion on the potential and their views whether one can subscribe to this IPO.

Affle (India)

Affle (India) is a global technology company. It is a data analytics, market research and digital marketing platform. It undertakes advertising and promotional initiatives on cellphones on behalf of its clients. Apart from India, the company operates in South East & Middle east Asia, Europe, US, Japan, South Korea and Australia.

It has two business segments –

Consumer platform (B2C) Affle’s Consumer platform : Reaching out to new customer and facilitating conversations. B2C company / ad agency wins a qualified user (shopper) who is most likely to spend money on its product/ services.

The consumer platform aims to enhance returns on marketing spend through delivering contextual mobile advertisements

Enterprise platform (B2B) The enterprise platform, on the other hand, primarily provides end-to-end solutions for enterprises to enhance their engagement with mobile users.

| Region | # of consumer profile (in crores) [as on 31 Mar 19] |

|---|---|

| India | 57.1 |

| **Other emerging market **** | 58.2 |

| **Developed Market *** | 86.7 |

** Comprises South East & Middle east Asia, Africa and Others

*Includes North America, Japan, South Korea and Australia

| Region | Contribution of Revenue in Fy19 |

|---|---|

| India | 56.4% |

| **Other emerging market **** | 43.6% |

Source - Company

Over a period of time, the Consumer Platform is likely to add new customer data, track their interests and gauge responses to historical notifications. The accuracy of the prediction improves with every advertisement, as the systems incorporate new data and update the earlier one.

Wide industry coverage

The Affle Consumer Platform undertakes automated mobile advertising on behalf of B2C companies or advertisement agencies (that are hired by them). Affle’s clients (within and outside India) are spread across sectors such as e-commerce, fintech, telecom, media, retail and FMCG.

Brand Association

According to Frost & Sullivan, Affle is a leading advertisement tech solution provider in India.

Usually, since ad marketing contracts tend to be long term in nature (client stickiness) and barriers to entry are high, Affle stands to gain.

Asset-light characteristics

Since Affle’s business is tech based, it doesn’t entail substantial investments year after year.

| Financial (rs Cr) | Standalone FY17 | Standalone FY18 | Standalone FY19 | Consolidated FY19* |

|---|---|---|---|---|

| Revenue | 65 | 83.8 | 117.8 | 249.4 |

| Inventory and data cost | 32.4 | 42.4 | 62.3 | 134.1 |

| Employee Costs | 17.6 | 16 | 19.5 | 21.2 |

| Other Expenses | 12.1 | 8.6 | 11.2 | 23.7 |

| EBITDA (Margin) | 3.5 (5.4%) | 16.8 (20%) | 24.8 (21%) | 70.3 (28.2%) |

*After acquiring Vizury in Sep 2018

Affle’s core product

-RevX’s acquisition [in Jun 2019] was done to strengthen consumer platform. -Engaging with existing customers on Affle’s database to help them complete transactions on e-commerce market place (Vizury was acquired for this purpose)

-Building an online-to-offline (ensuring that online ads encourage people to do offline shopping by visiting a store and availing schemes / discounts / offers) Shoffr was acquired [in May 2019] for this.

In connection with the Consumer Platform , revenue accrues to Affle on a CPCU (cost per converted user) and ROI (return on investment) basis.

While CPCU model constitutes a large chunk of Affle’s topline, the company also earns revenue by the following :-

Curating ads for the advertisers to build awareness about their product / services

Encouraging a pervious customer to make repeat purchases

It owns platforms such as mobile-audience-as-service (MaaS), mFaaS for mobile ad fraud detection, ‘ad2campaign’ for mobile marketing, ‘Ripple’ for cross screen advertising and ‘mTraction TVSync’ for TV-linked digital advertising, among others.

Promising Potential

India is one of the largest cellphone markets globally. B2C companies / advertisers / e-commerce players are increasingly adopting digital advertising on cellphones. As per Frost and Sullivan estimates growth potential of the digital advertising market in India is about 39% CAGR.

2 Likes

Your view innovation facade please. More than a year since you commented

Indian Railway Catering and Tourism Corporation is a subsidiary of the Indian Railways that handles the catering, tourism and online ticketing operations of the Indian railways, IRCTC is coming up with an IPO that would open for subscription on 30th September, 2019. IRCTC Limited is the only provider to Railways for online ticket booking and catering services.

Positives : Continuous improving in the financials

Monopoly business

It is everyday essential of business and citizen of India

Have Land banks and lots of metal junkyards which if materialised can lead to gold mine.

The Rail-neer is growing publicity due to affordability and purity

They are upgrading and modernising and in process towards more professional catering.

it is backbone of economy .

Online booking creating a good revenue and free upgradation to upper class.

Attracting lots of talents

IRCTC operates the Lucknow - New Delhi Tejas Express which had its inaugural service on 5 October 2019 and is the first privately operated long-distance train in India.

Loyality cards : tie up with SBI & UBI

IRCTC eWallet is a scheme under which user can deposit money in advance with IRCTC and can be used as payment option along with other payment options available on IRCTC for paying money at the time of booking tickets.

conditions Registration Fee: Rs 50 + Applicable Taxes (non-refundable) Transaction Charge: Rs 10 + Applicable Taxes per transaction No cash refunds / No redemption allowed. IRCTC eWallet balance can only be used for booking railway tickets. IRCTC eWallet service can only be availed by users registered with Indian Nationality and with Indian Mobile Number,

ref : http://contents.irctc.co.in/en/AboutEwallet.pdf

another good app Imudra digital wallet

https://www.irctcimudra.com/home

IRCTC has its own air ticketing portal www.air.irctc.co.in & selling approximate 4500/- tickets on daily basis. In addition company is authorized to book air tickets on Government Account as per the Office Memorandum No. 19024/1/2012-E.IV of Ministry of Finance (DoE).

Business Segments ;

Catering

Packaged Drinking Water (Rail Neer)

Travel and Tourism

Negative

Being Governmental it is BABUSHAHI

Significant differences exist between Ind AS and other accounting principles, such as IFRS and U.S. GAAP, which may be material to investors’ assessment of our financial condition.

https://listing.bseindia.com/download/365101/IPO/IRCTC%20LIMITED%20DRHP_20190823183900.pdf

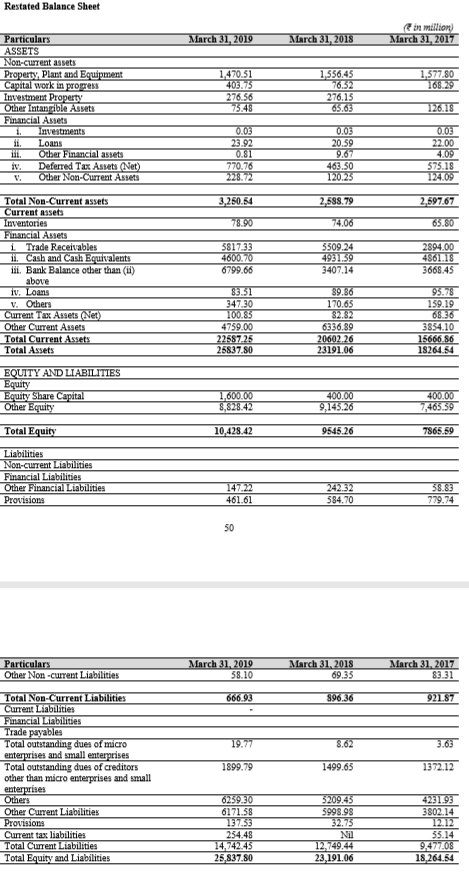

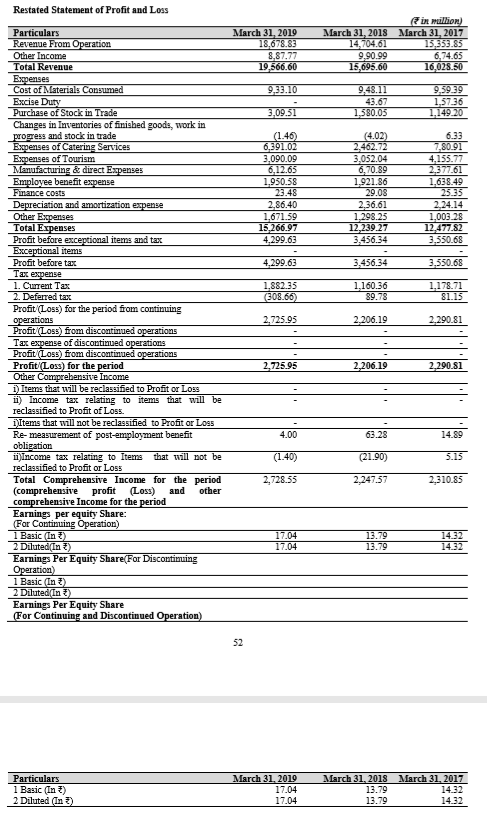

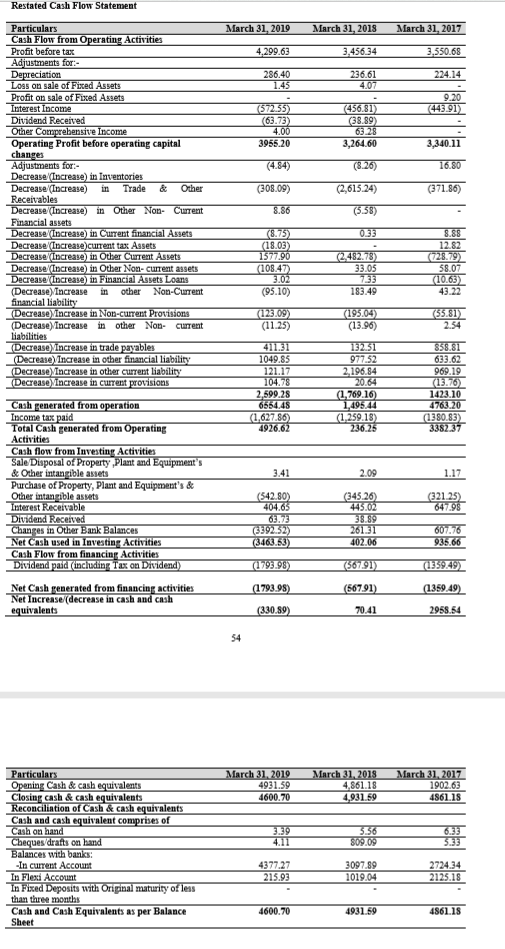

Balance sheet

Profit and loss

Cash flow statements

Could you please share your views @bheeshma @Vivek_6954 @Yogesh_s @phreakv6 @dd1474 @hitesh2710

Regards

5 Likes

I have looked at the financials when it filed it’s dhrp. They look good. If I recall correctly the co is having an roe of 27% or thereabouts and is debt free. Its payout is 47% which is also good. In my opinion it’s not a screaming buy but there is value on the table to be a good medium term purchase.

The future growth driver would be Cateen business as seen from last 3 years financial. The company has good cashflow generating service business (mainly internet ticketing) which has high margin, near monopoly and also controlled by Governent priorities. Very diffcult to value same and hence no idea how it would grow. The catering business has shown major growth in last 2 years but margins are lower. While traditional valuation parameters like PE, Dividend yield, cashflow generations are good to moderate, it would be real call on Government’s perspective to this business. In past they did waived the internet booking charge which affected the performance which just got reinstated.

Further, while the company is in existence since 1999, I am not able to understand while financials are provided only for past 3 years. It is too small period to see how business has performed over cycle. While all successful ingriedient of business like, cashflow generating , diversified, monopoly business are positive, Management being government result in undercertainity about growth and capital allocation. Investor shall consider all these factors and also his/her own risk return expectation while making investment decision.

Discl: While not decided at point, I may subscribe in IPO when it open. My view may be biased and I am not SEBI registered investment advisor.

2 Likes

A good brief about the IPO- https://finshots.in/archive/why-everyones-talking-about-irctc/

The only or the biggest negative seems to be government decisions which are not in the interest of the shareholder but the public at large. Without any peer to compare, how do we look at the valuation?

5 Likes

Interesting IPO. While a monopoly (read a firm wide moat) is always desirable, few things I would look before considering this IPO

-

The major growing revenue segment i.e catering is that really immune from disruption ? My last experience as a customer was horrible food and if I am not mistaken, the food price is baked into the ticket and can not be opted out of. Now if Govt under popular pressure decides to decouple the food from ticket price, will the food quality still find so many takers ?

-

Few years back some startups had started serving food in train from popular joints of the journey stations. Do they have to pay any licensing fee to irctc ?

-

Very relevant point raised in the above link - how do we gauge its valuation as there are no peers ? Typically we know that IPO are priced to extract maximum benefit for promoters. Is it the same happening here or is it another D’Mart ?

-

small point and pretty sure may be me crying wolf - with the improving road infrastructure and rising income levels , could rail travel be poached into by roadways and air transport ?

PS- Still thinking over whether to take the plunge or not. Going to read the DHRP and take a call. Not SEBI RIA

2 Likes

- Regarding point number 2. Yes, it seems that they would have some contract with IRCTC and they pay fee to IRCTC.

Check this

https://www.thehindubusinessline.com/economy/logistics/railyatri-app-integrates-with-irctc/article28250822.ece

and

https://www.medianama.com/2019/05/223-irctc-takes-railyatri-and-travelkhana-to-court-over-unauthorised-meal-services-our-take/ - Regarding point number 4. You are correct over last 4 years, number of railway passengers have remained flat. Also rail based tour packages have declined in gross revenue terms. I think it is getting poached by air transport mainly due to competitive air ticket pricing.

- Total railway passenger traffic has remained nearly flat over last few years:

a. 2014: 8,397 Million passengers

b. 2018: 8,286 Million passengers - Major growth driver as per DHRP is “Catering” and “Rail neer”. Catering has been transferred back to IRCTC from zonal railway as per changed 2017 rules. Their revenue from catering segment is now more than 50%. Focus on e-catering and capacity addition in terms of more base kitchen can provide growth opportunities. Currently IRCTC has ~40% market share of packaged drinking water of railway due to constraint in capacity. They are adding 10 more plants and target to capture ~80% by 2024.

- From September IRCTC is levying service charges on portal. Rs 15 for non-AC class and Rs 30 for AC class. Assuming 8300 Million passengers and current penetration of e-ticket at 70% and all ticket to fetch Rs 15 (share of upper class ticket is too low ~2%). This may add 87,150 Million to revenue in short term. (in this and next yeat) After which it should be stable.

- IRCTC has been mandated to run trains. Pilot project is to be launched on two tracks. IRCTC leases train from Railway and provide services on top of it, like insurance, baggage insurance, penalty if train is late more than 1 hour. IRCTC has freedom to set fare. As per simpified calculation, IRCTC would earn at least Rs 50 crore from these two trains a year, deducting all the charges and lease payments to railway, they should have Rs 5 cr as net profit. Though it is in very early stages, but if it works, this can provide long runway to IRCTC growth. Railway can develop infrastructure and IRCTC can provide value added

services. Refer https://www.thehindubusinessline.com/economy/logistics/irctc-to-flag-off-indias-first-non-indian-railways-train/article29511530.ece for more details.

3 Likes

Is the revenue from catering sustainable as the average speed of train increases i.e journeys taking less time?

Rail neer peddled via plastic bottles. Will ve interesting to see if IRCTC can come up with some eco friendly alternative to that.

Nevertheless an interesting IPO indeed.

There is some calculation mistake or wrong assumption here, which i could not find. I checked what was the loss to company when these charges were removed in Nov 2016. In FY 2017, company had earned 362.25 Cr as service charges. This number and calculated revenue number above (8715 Cr) varies vastly. At that time e-ticket penetration was 62% and service charge for non-ac class was Rs 20. Current penetration: 70% and service charge Rs 15. I believe around 362.25 Cr should come back to IRCTC. Reducing government’s reimbursement of 88 Cr. For this FY half of this number (362.25-88 = 274.25 Cr) should be added to PBT (launched in september only). Which should be ~ 137 Cr. At 30% tax rate. Should add 95.9 Cr in PAT. This would increase FY20 PAT by ~35% at ~367.6 Cr. FY20 Eps: 22.98. FY20 PE: 14.

1 Like

Would like to correct some figures so as to reach right conclusion:

From 1st sept 2019, IRCTC is charging convenience fees of Rs 15 for non AC ticket and Rs 30 for AC ticket. Since percentage of non- ac ticket is little more, lets assume IRCTC is charging on average Rs 20 per ticket Approx. 7 lakh tickets are booked per day thus total earning in a day would be 1.4 cr. i.e in a year IRCTC will earn approx. 365*1.4 cr.= 511 cr. Minus Rs 80 cr. of govt. reimbursement total earning from convenience fees will be 431 cr. Since charging convenience fees is resumed from 1st of September, hence for financial year 2019-20 only 07 months income of convenience fees will added in net profit. I.e means 251 cr. Minus 30% of tax, final profit after tax will be approx. 176 cr.

Profit of approx. 176 cr. from convenience fees will be added in existing profit for the year 2019-20.

Please correct me, if I went wrong somewhere.

1 Like

Why only last three year’s figures are shared by the company?

FINANCIALS OF IRCTC

- IRCTC’s revenues, EBITDA and PAT over the years are in Fig 3. Revenues, EBITDA & PAT have grown at a CAGR of 10.4%, 10.1% and 9% resp. from FY17-19. The 3 year nos. may look average.

- The PAT growth for FY19 was 23.5% from ₹221 cr. to ₹273 cr. IRCTC wrote off bad debts of ₹46.1 cr. in FY19. Adjusting for this the PAT growth would have been 37% for FY19.

- IRCTC had a RoE of 26.14% and RoCE 38.77% for FY19. This is excellent. The 3 year avg. RoE is 25%.

detail post on IRCTC

1 Like

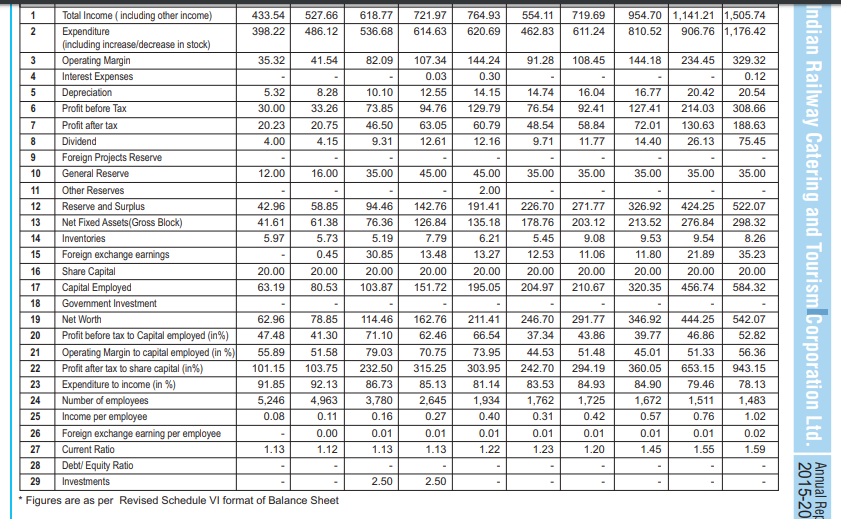

Find enclosed 10 year financial snap shot from FY19 AR of IRCTC.

The last 10 years AR are avaialble on web site in case anyone is interested in studing the past financials.

https://irctc.com/annual-report.html

A quick glance as number suggest that as against typical PSU, IRCTC has been quite efficient. Look at empolyee strength declined by more than 35% during last 10 years, while Total income increased by 12% CAGR over the decade. During same period, net profit CAGR is around 19% p.a. and Dividend payment CAGR is around 29% p.a…

This may be also due to many employee being deputed by railways and we need to understand exact relationship between Railway and ITCTC for manpower.

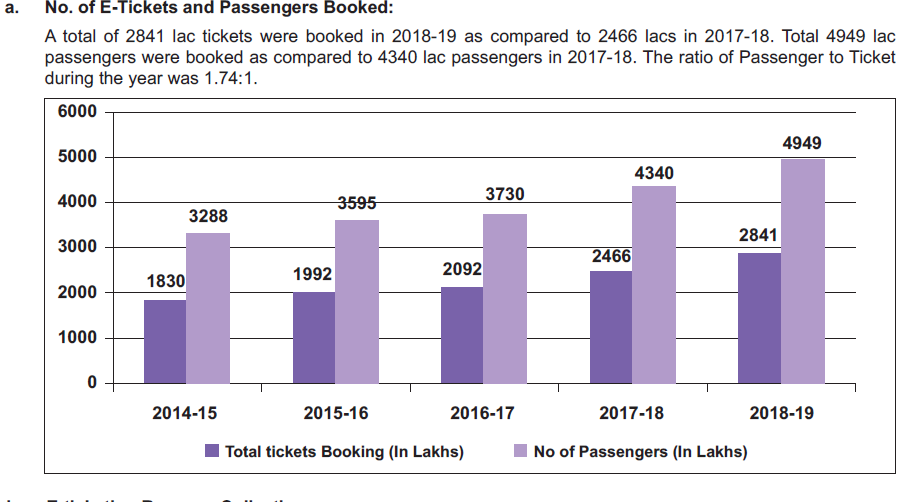

Ticket booking details:

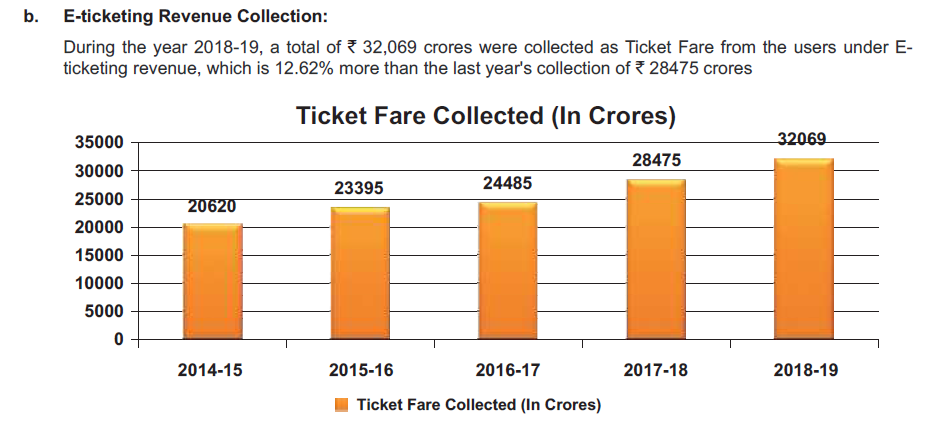

Total E Ticket revenuew:

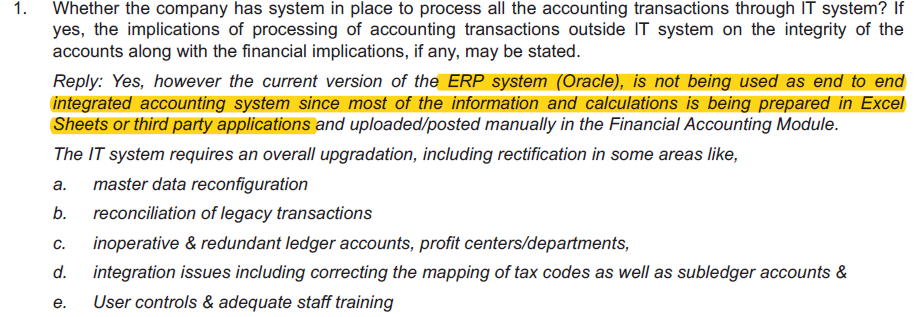

In AR FY19, there is comment about IT system of company in page 93 which is bad for a company claiming to have ticket booking. This is my view and may be wrong, but consider this observation as real issue.

This may be also due to many employee being deputed by railways and we need to understand exact relationship between Railway and ITCTC for manpower.

Discl: I got allotment in the IPO and my view may be biased. Investor shall do his/her own due diligence before making any investment decision.

6 Likes