Moksh Ornaments Ltd - IPO Preview

Story

Moksh Ornaments is a Mumbai based wholesaler of traditional basic jewelry like bangles, chains and mangalsutra. Company does not manufacture or design or retail jewelry but works with third party designers to design the jewelry, get those designs and samples approved by jewelers and then get those designs manufactured on a job work basis. Company has a factory in Bhiwandi for procurement, inspection and dispatch functions.Company works on a gross margin of 4% and a net margin on 1%.

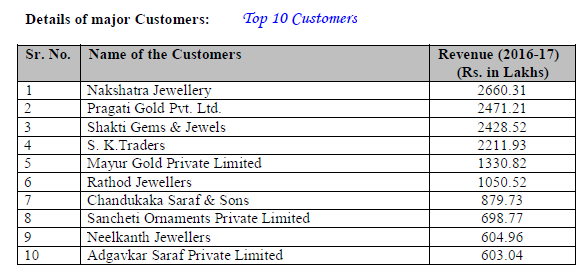

Top 10 customers

Procurement Policy

Company is largely de-risked from gold price movement since it is sourcing gold under gold loan schemes of suppliers of raw material. Text from IPO prospectus.

We follow a procurement policy aimed at de-risking the business from gold price

fluctuations by sourcing gold for our business operations under the gold loan

schemes from our suppliers. Under such arrangements, the price of gold

purchased is not fixed on procurement, but rather within the applicable credit

period, on the basis of prevailing gold rates on sale to customers, thereby

minimizing any risk to us relating to gold price fluctuations between the time of our

procuring the raw material and selling the finished product to our customers.

There are no listed competitors in wholesale jewelry segment as all listed companies are either manufacturers or retailers.

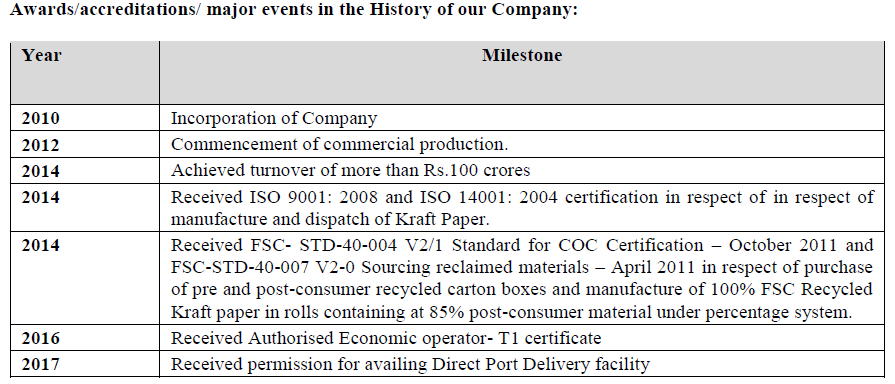

Brief History

- 2012- Incorporated. Took over businesses carried on by promoters Amrit J. Shah and Jawanmal M. Shah as a sole proprietor of M/s. Jineshwar Gold and M/s. Padmavati Jewels respectively.

- 2014 – Additional capital infusion.

- 2015 - Additional capital infusion.

- 2017 – Converted to public limited company.

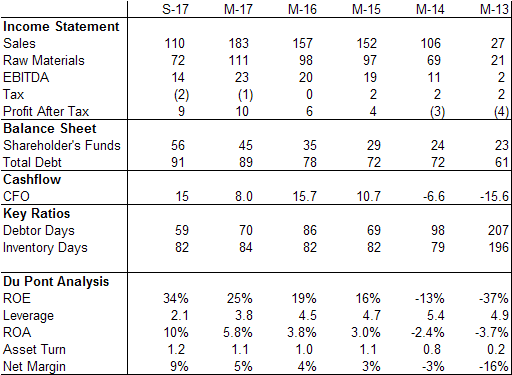

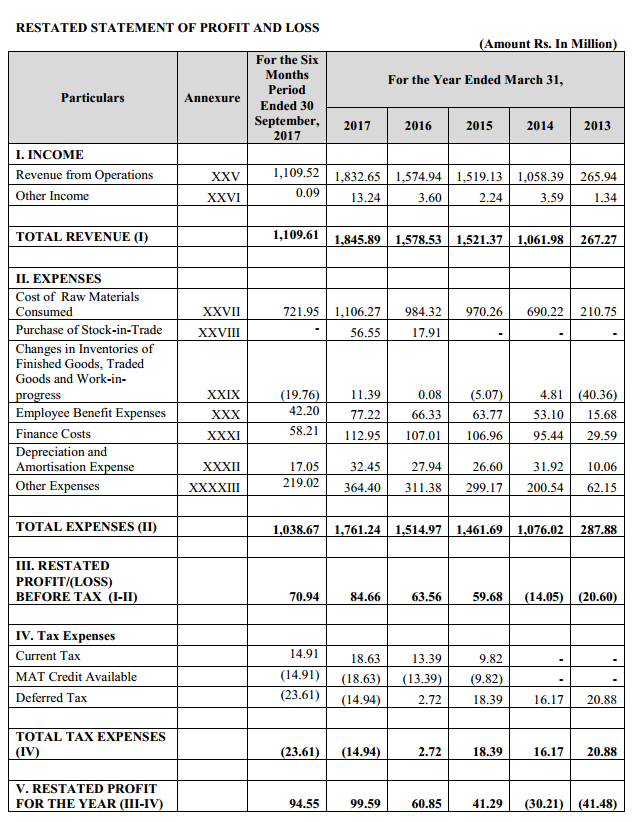

Financials

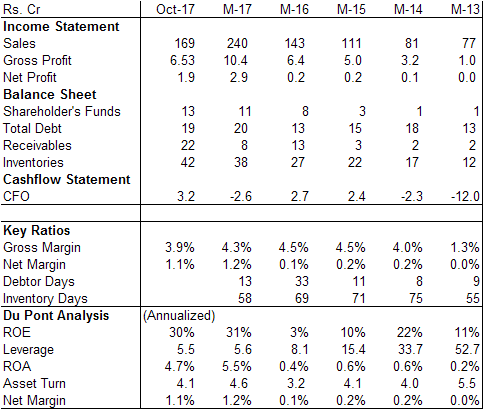

Sales have gone up 3x in 4 years while gross margins are steady at 4%. Net margins have gone up only recently as operating costs have stabilized so operating leverage is kicking in. Debtor days have remained low and total debt has remained stable even when sales have grown sharply. ROE is good at 31%. Drop in ROE in FY 15, and FY 16 is due to additional capital funding.

Corporate Governance

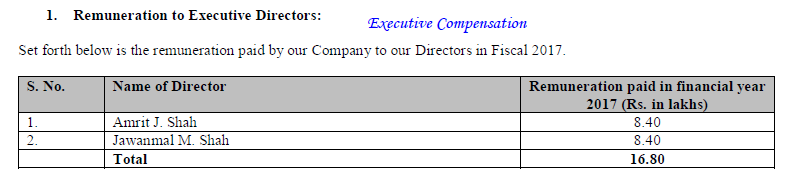

Company is promoted by 74 year old Jawanmal Shah and his 45 year old son Amrit Shah. Both have about 30 and 20 years of experience in jewelry respectively in the jewelry hub of Mumbai. Both own 40% of the company each and rest of the Shah family own the remaining 20%.

Promoter Salary is reasonable.

Dividends - Company has not declared any dividends during the last five financial years.

Tax Payments - Company is booking tax costs at full rate and actually paying those taxes too.

Debt Repayments – Company has repaid debt when additional equity capital was raised.

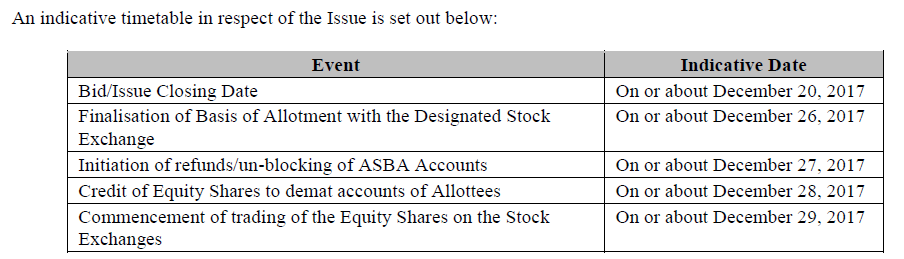

IPO Details

Company is selling 29.82 lakh shares at a price of 37 Rs. Number of share outstanding after the issue will be 107 Lakhs valuing the company at 40 Cr on a post issue basis.

Objects of the issue

Out of the 11 Cr to be raised from IPO, company will use 7.4 Cr for working capital, 3 Cr for repayment of debt and remaining 0.6 Cr for issue expenses.

Valuation

Company is asking for a valuation of 40 Cr on a post issue basis. Company is almost doubling book value from 13 Cr to 24 Cr. On an annualized PAT of 3.3 Cr for FY 2018, P/E works out to be 12 and P/B works out to be 1.7. Leverage will come down from 5.5 to 3.3.

Investment Rationale

Company has managed to grow sales 3x in last 4 years. Company’s customers are chain store jewelers. Jewelry business is going through a transformation where organized chain stores are taking market share from local jewelers. Company is helping these jewelers by outsourcing manufacturing function so jewelers can focus on retailing and brand building. Company mainly deals in traditional basic jewelry so obsolescence is minimized. Designs are approved in advance from customers and gold price risk mitigated by its procurement policy. Company has a relatively rigid return policy. Company has managed steady gross margin of 4% over last 4 years. With a net margin of 1%, company is not taking too much value from supply chain so it is likely to keep customers and grow business. Company has won repeat orders from key customers.

Key Risks

- Net margins have gone up only in last 1.5 years. This could turn out to be a pre IPO bump.

- Operating cost actually declined in FY 2017 while sales jumped 60%. This sounds unusual.

- Company is asking for a 70% premium to book value most of which will be cash. Valuation appears to be on the higher side.

- Company has no brand, factory, or organizational setup. This is still a father-son story with 8 employees. Execution and scaling risk is high.

- Customers could decide to in-source manufacturing and designing, rendering company’s business unviable.

- Company does not have any written contracts with customers. This is mainly a relationship business.

- Company works on wafer-thin margins.

Disc: Applying for IPO. Viewed invited especially negative.