You maybe right. I misunderstood. But looks like it will have no effect as still even after opening of plant there will be shortage of Ibuprofen.

1 Like

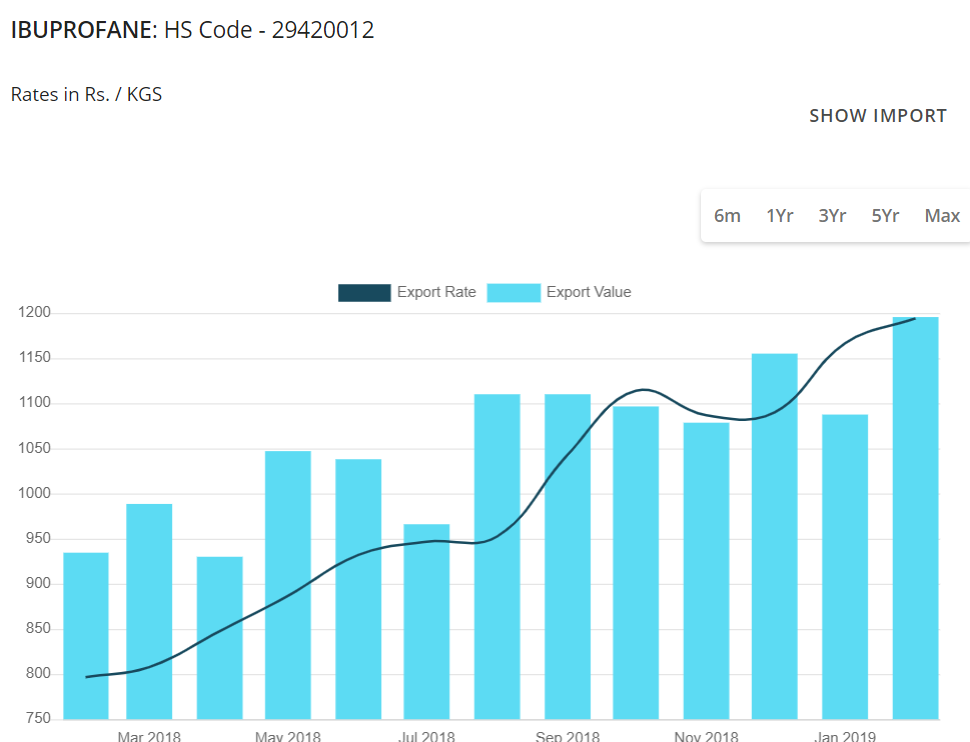

Anyone tracking current ibuprofen prices? Whats the current price in India and international market?

Hi @nityanandparab Can you please let me know the source for the data so that it can help all of us, many thanks.

The source is screener.in

1 Like

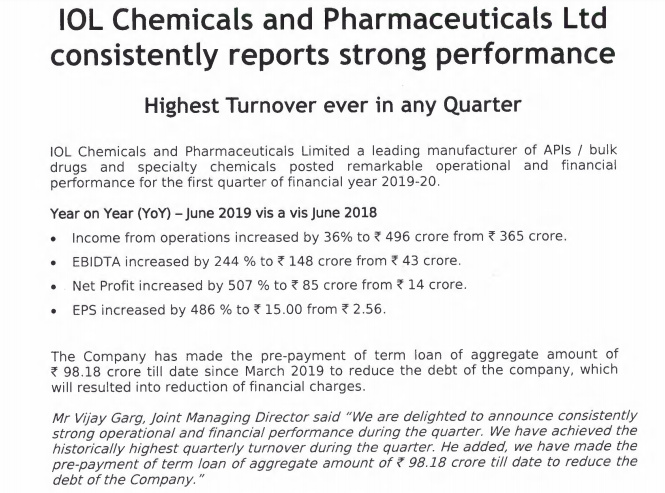

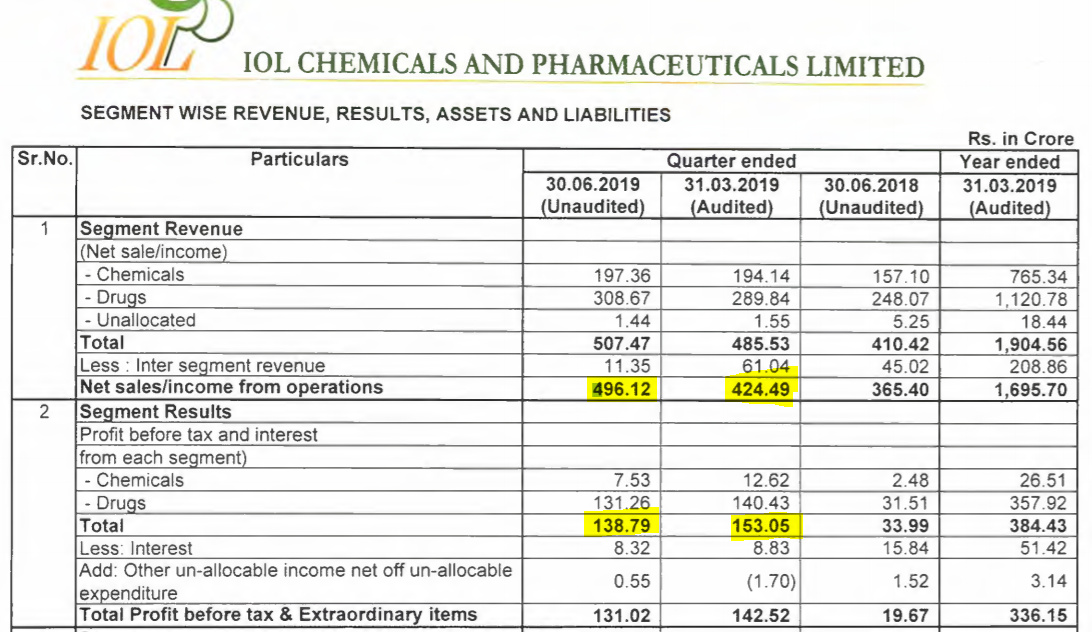

What a fantastic result ! 100 Cr np in Mar qr. Ending at 42 eps.

All concerns laid to rest.

Tommorow we may see a huge jump in share price and maybe end near 20% upper circuit.

I don’t know why my earlier post was mark as offended.

I think I would like to see why it was marked offended. Can the editor write me about it?

I will appreciate the reply.last year halfway that they expect sales to be 1700 cr. He was absolutely on dot.

The MD Vijay Garg said in one interview

Capacity increased by 20% in both Ibuprofen Maf and IBB as well. Loved that. Holding…

The EBIDTA margins HV improved from 28% in Q3 to 37% in Q4…

But the revenue has declined from Rs. 478 Cr in Q3 to Rs. 422 Cr. In Q4…

Any reason for QoQ decline in revenue??

1 Like

Mr Rao,

I am not too much knowledgeable person but all I can say, is don’t try to find perfection in every stock. Let Luck plays role too.

If one try to look at each and every aspect in every stock we buy or want to buy then we will not able to buy anything.

It is my experience that I am writing here. Even after looking everything , one ends up losing money in stock market. Viz. Rain Ind, Ril Com etc etc and the list is endless. So overall if stock looks good then go for it. If you will try to look at other stocks which has come out with excellent or good results, they are already quoting high with high Mcap too. IOL Chem is the only stock now which is showing huge profit and still available at Mcap less then the sales. 1700 Cr Sales and 1250 Cr Mcap.

I have written previously here that Mcap is the single most parameter for Valuation according to me. If Mcap is over 2-3 times sales, then very hard for the stock to give multibagger return.

When I bought in last June or July around 80, I was not knowing that Ibuprofen price will go up to such a high. My rationale was, at 80, I am getting a Pharmaceutical Co and a Speciality Chem Co. So Mcap below Sales, almost half of sales, it was a blind buy for me and bought good quantity.

The only thing I was expecting was, sooner or later the management will reduce the debt and the Interest will turn in bottomline. Same with Speciality Chem div. Sooner or later, it will start making profit. But it was my luck that Ibuprofen prices went up very high and I think it will not go down in next 3-4 yrs. It may stabilize but should not go down. 5-10% up and down is taken care of.

2 Likes

Thanks @ridesai makes sense, to be honest it was not a concern that I wanted to highlight, it was more of a observation, totally agree on the ibuprofen story.

Disclaimer : Invested

Rao,

The best part in this result of IOL Chem is, there is notes below that they paid 47 Cr of debt. That is huge. Just in 1 qr, they paid 47 Cr. Excellent going. Management is doing the right thing. I think at the start of the last year, they were having LT debt of over 500 cr. Let us see where it stand now after 1 year . The last 2 qrs were real extraordinary which will keep repeating and even excel them as the capacity of Ibuprofen and IBB has been increased by 20% and 30% respectively which will fetch 20% to 30% upside minimum is sales and can’t figure out what can be the bottomline. But conservatively I can put atleast 20% increase in bottomline minimum for whole year. The biggest advantage of IOL Chem is it is world 1st and only backward integration plant for Ibuprofen which has no effect of increase in price raw material, Viz, IBB.

2 Likes

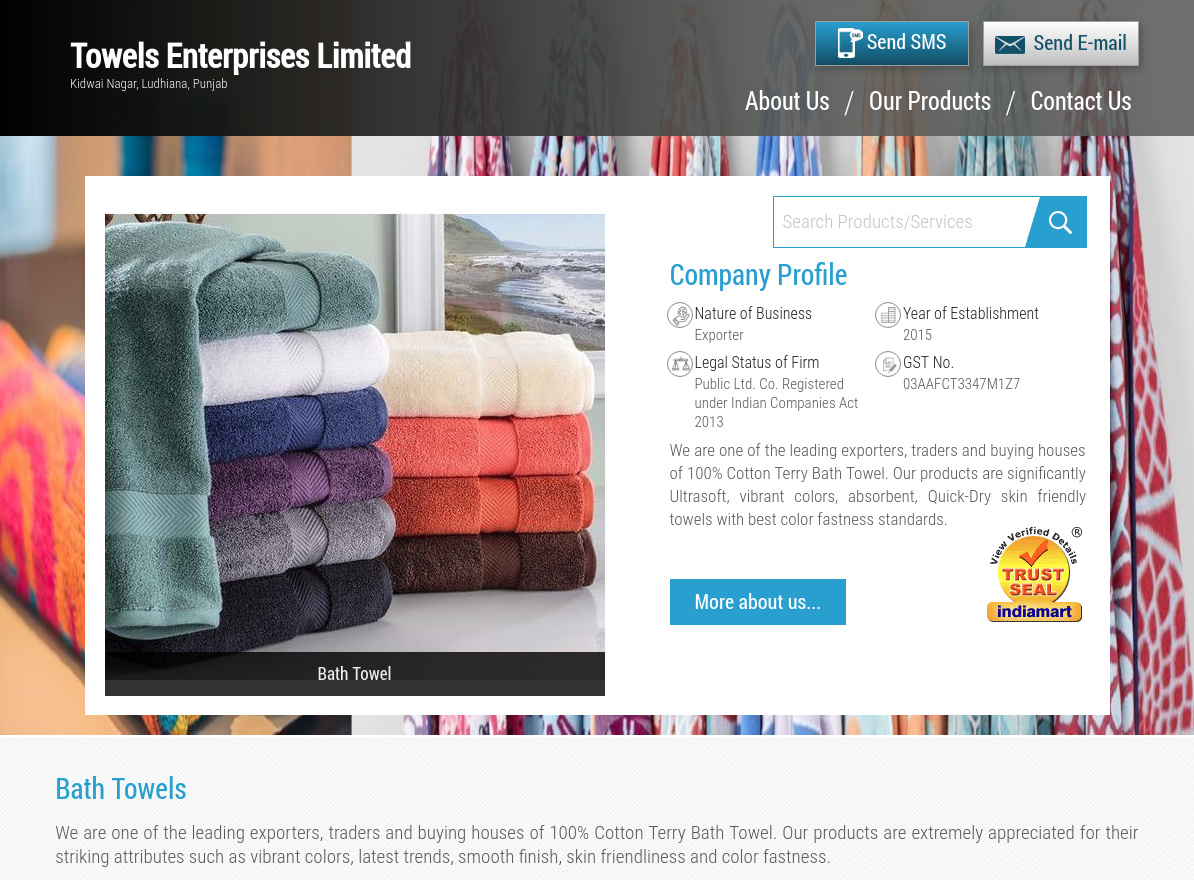

In related party transaction for fy19, company has disclosed purchase of goods worth Rs. 110cr from Towels Enterprises limited.

We need to answer the following

- Is company purchasing goods from promoters identity at market price or above market price?

- Why is company purchasing goods from company promoted by promoters?

Edit -1 (dated - 4-Jun-19)

According to the website of Towels Enterprises (www.towelsenterprises.com/) having registered office in Ludhiana, company is in business of Terry Bath Towel.

What kind of good worth about 100 crore a chemical company is buying from a bath towel manufacturing company?

4 Likes

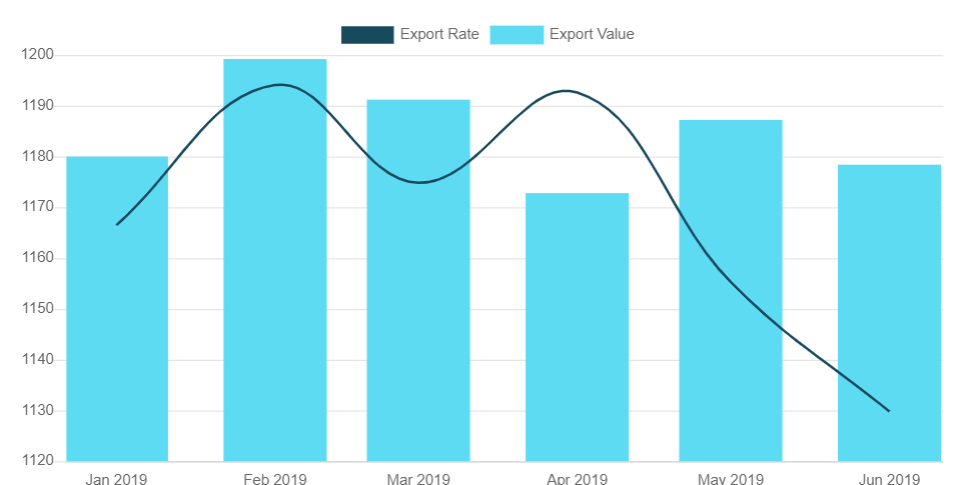

Hi Nityanandparab,

Can you share the latest ibuprofen prices which you can see on screener.in

Thanks in advance for the help

Watch to days interview-will also answer many earlier questions as well.

The data has not been refreshed after Feb 2019 in screener.

1 Like

That is a very good point. I appreciate your inputs.

I have written a mail to them.

Let me see what they send me in reply.

The company is of promotor group .TRIDENT . IOCCP is another independent venture from the promotors of Trident group . It is based in Barnala 64 acres of land . This company is largest backward integrated ibuprofen manufacturer company . It has captive power plant 17 MW of itself . The fuel they are using in boilers are green / biomass . They are improving bottom line by taking various measures (

However I am not big fan of TRIdENt group ) But this can be a good short term Candidate . BASF will open its plant in FY 21 . The new plant which is closed due to Technical reason have less capacity than IOCCL . On top of this many chemical companies in CHiNA has shit down .

Apart from towel company there is another related company Vivachem intermedite pvt ltd .

The other issue which I don’t like company is issuing convertible warrents to its promotor i.e Towel ent ltd total of 2500000 @ Rs 205 on March 19 out of which it has already converted 682000 warrents in to shares

Bulk drug contributed around 66% and 34 % by chemical division .

To your question the amount represents the amount they received from Mr Towel & Comp for Converting the warrents in to equity

Disc

Not holding Not a recommendation to buy sell or hold I am not a sebi approved Analyst strong text

3 Likes

Before announcement of quarterly results as scheduled on 12 August the management has lowered it’s loan book as promised in their concall. On 5th of August they have informed to stock exchanges that they have repaid 14 Crore of term loan.

link:-https://www.bseindia.com/xml-data/corpfiling/AttachLive/dc14f6cc-afe2-4850-85db-9a154632e394.pdf

2 Likes

Excellent results by company

https://www.bseindia.com/xml-data/corpfiling/AttachLive/e9edb0e9-b5c6-4d1f-a978-900313e28284.pdf

Overall good result with reduction of debt of close to 98 cr, margins have come down on a Q-o-Q basis.

The EBITDA margin was 36% on Q4FY19 and currently stands at 28%

Can this be due to the decrease of the price of Ibuprofen.

@nityanandparab - Would you please be able to share the latest price trend of ibuprofen if possible.

Disclaimer - Invested

1 Like