IOL Chemical & Pharmaceuticals ,Company primarily operating in 2 verticals Speciality Chemicals & Active Pharma Ingredients.

The Specialty Chemicals division produces Ethyl Acetate (87000 TPA), Iso Butyl Benzene (9000 TPA),MCA (7200 TPA),Acetyl Chloride (5200 TPA) for use in a variety of end products like flexible packaging, pharmaceuticals, textiles, food processing, pesticides and paint industries.

Active Pharma Ingredients (API) division in Pain Management(Ibuprofen with installed capacity of 6200 TPA) and its derivative and salts, in Life Style Drugs (Metformin Hyderochloride, Lamotrigine, Fenofibrate etc) are developed for commercial distribution across the globe. Presently, 6 API’s are already commercialized and 10 API’s are in the advance stage of development.

API segment journey

Initially started with Mono-chloro Acetic Acid (MCA) and Acetyl Chloride as raw materials for pharmaceutical product called Ibuprofen. Later As part of Backward Integration plan, IOLCP commenced a new plant of Isobutyl Benzene (IBB) having annual capacity of 6000 MT to ensure ready availability for important raw material of Ibuprofen. With this company became World’s only integrated Ibuprofen plant. Subsequently the plant is approved by USFDA, EUGMP agencies.

Similarly company completed a co-generation plant of 17MW to meet the energy demands of its production units. company completed these plant setup / capacity expansions with an investment outlay of Rs.256 crore.

Currently the plant is running with 60% capacity utilization, no fresh investment is required for further capacity utilization.

The backward integration with specialty chemical products will facilitate the company to be more cost effective in the production of Ibuprofen will not need to depend upon suppliers for the raw material and price trends.

Players like Vivimid, Shasun or Granules India has to depend on IOL CP or Jubilant Chemicals for ordering the Raw material for preparation of IBUPROFEN.

Siting strong demand growth for ibuprofen , BASF is setting europe’s first plant in germany with a cost of 200 million euros which is operational by 2021.

https://www.basf.com/en/company/news-and-media/news-releases/2017/06/p-17-260.html

Good clientele:

The company has strong business relationships with a number of prestigious clients such as Ranbaxy Labs, Dr Reddy, DS Group, CIPLA, Uflex Industries, ITC Limited, ICI Paints, Asian Paints, Pidilite, Rallis India, Hindustan Polymide, Gujarat Super Phosphate, and Avon Organics Ltd.

Financials:

Positives:

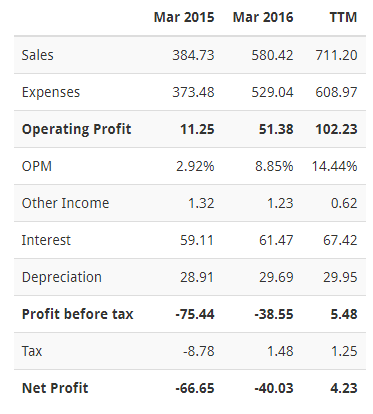

- One of the Primary reason for investing in this stock is turn around in financials from a loss of -66cr in 2015 to -40cr in 2016 to +4cr profit in 2017 .

- Margin expansion(9% to 15%) coupled with increased top line (580cr to 711cr) YoY.

- Strong product growth globally for Ibuprofen (where company is getting 18% margins from this segment without any fresh capex considering 60% plant capacity utilization), in fact company reported 6 straight quarters of increased top line.

- Management acumen in turning round the chemical products business from 40cr loss to 4 cr loss this year.

- Company success in Latin America is going to be replicated in Europe with recent EUGMP certification.

http://www.bseindia.com/xml-data/corpfiling/AttachHis/a55d52c1-f0ed-449f-acab-b12cdaa43b35.pdf - The synergy in business verticals made it possible for the management to built pharma plant, moving away from traditional chemical business to high margin pharma segment. Any new player to venture in plant setup and integration will take 4+ years time (Even world major BASF europe plant estimated time).

- Promoter increased the stake from 39% to 41%.

Negatives:

- High debt on books, D/E ratio of 2.4 is very high ,though recently CARE upgraded long term borrowings on account of improved financials. This is the main reason for undervaluation of company i feel currently.

- Equity dilution in 2015.

- High inventory to support the pharma operations.

Investment theme: Classical case of turnaround of a company where one division is loss making versus the other which is profit making. Slowly the loss making unit will trim the losses and subsequently market players rewarding with market capital of company same as sales over a period of time.

Disclosure: Invested recently, currently stock price is trading at 63rs.

as there was no action on this thread.

as there was no action on this thread.