What is relation between roe and price to book and how market values generally 15 20and30roe companies in bull and bear markets

The direct relation is:

P/BV = (RoE - g)/(r - g)

Where P = Price, BV = Net Worth, RoE = Return on Equity, r = Cost of Equity and g = Profit/Dividends Growth Rate

Of course, this relation is applicable only for a stable-growth firm. But the logic being, a company earning a higher RoE tends to have a higher P/BV. The derivation, if you’re interested, is here.

2 Likes

Hi ,

Can anyone please tell me how can I find out , how much time it usually takes to reflect increasing/decreasing raw material prices in P&L statement. For example , if metal prices are low and its a raw material for any industry , when its effect will be reflected in P&L , in recent quarter or next quarter results. How can I calculate this or at least have a fair approx idea.

Namaste sir,

I am glad you have this thought of talking basics.

I am looking for basics in fundamental analysis. Basics of Balance sheet, Profit and loss and Cash flows. how to read them, what to look out for and ?

Please help

namaste ,

Amrish

For Beginners , you start reading books like one up on wall street , beating the street by peter lynch and Buffetology. Once you completes them , you can start reading the intelligent investor by Benjamin graham.

1 Like

hi seniors,@dineshssairam @Donald @hitesh2710

Need your help in understanding the cash flow statement (i have been working to create my own DCF Template)

I want to calculate the FCF of Meghmani Organics, but got stuck with the value of capital expenditure.

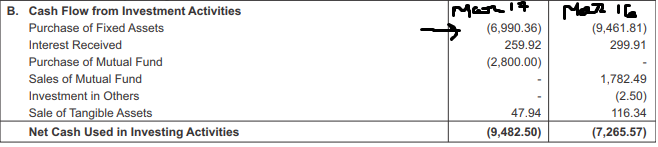

In the annual report (2017), the purchase of Fixed Assets (March 2017) is shown–>6990.36

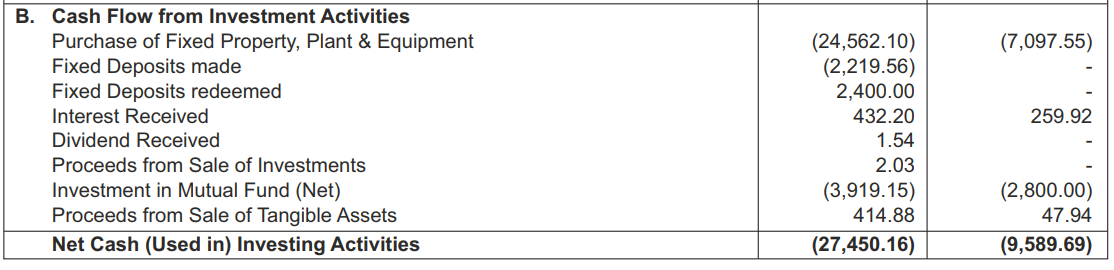

While in anual report (2018), the purchase of Fixed Assets (March 2017) is shown–>3124

My doubt is why the purchase of the fixed assets (2017) is not same in these two annual report? and how should i calculate the FCF value using the above values

Thnks in Advance

Are you sure you’re looking at the Consolidated statements in both the cases? Looks to me like you are looking at the Consolidated figures for 2016-17 and the Standalone figures for 2017-18. Here is the Consolidated CFI for 2017-18:

There is still a minor difference, which could potentially be chalked up to accounting policy changes. An accountant may be able to help you better here.

Thanks @dineshssairam for your prompt reply.

My bad, i was looking at the different statements (as rightly pointed out by you)

hi @dineshssairam,

sorry for disturbing but i am stuck again and need your help.

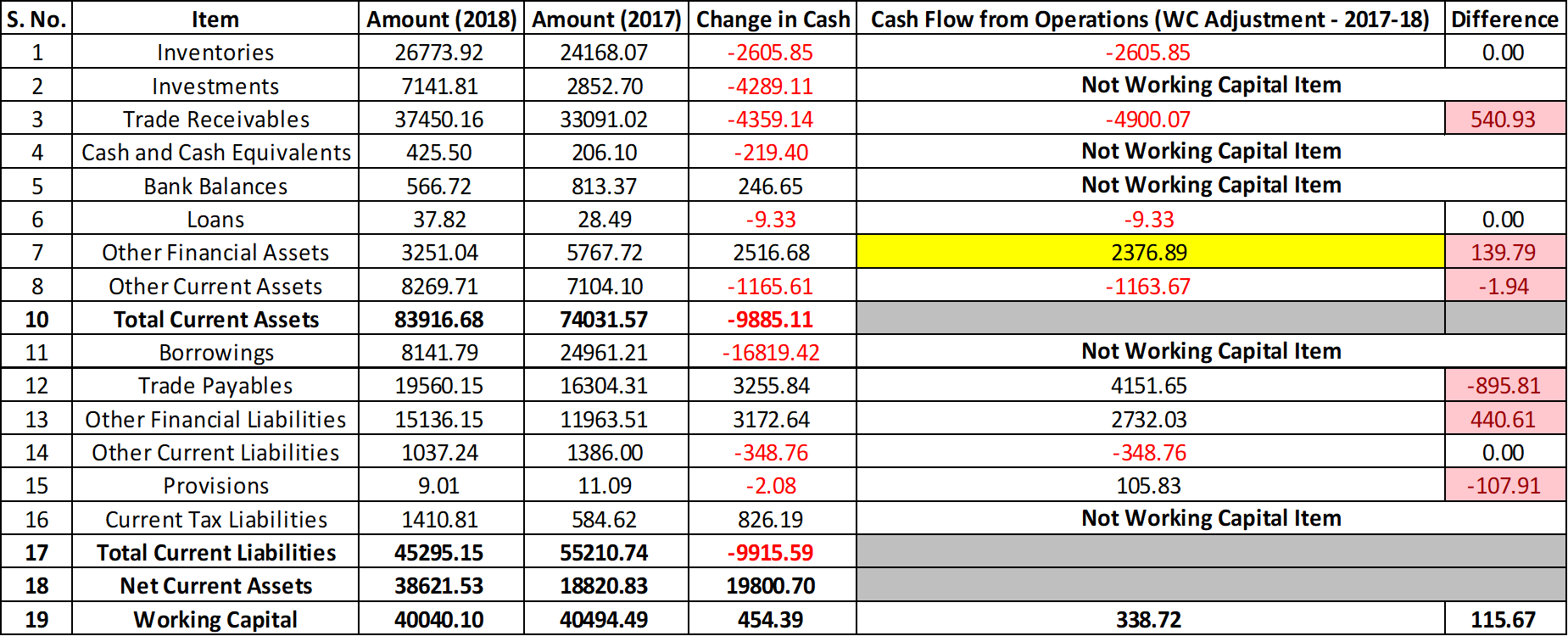

While calculating the free cash flow, we need Change in Working capital as Input.

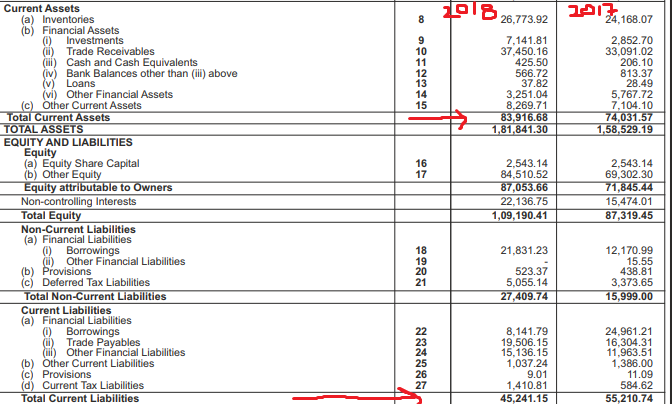

in Order to get the data for 2018 calculation, i took out the balance sheet for 2017-18.

i Calculated change in Current Asset (83916-74031=9885 Lakhs),

Then i calculated Change in CL (45241-55210= -9969 Lakhs)

Finally, i got Change in WC=9885-(-9969)=19854 Lakhs=198 Crores

The above number needs to be deducted as cash outflows from net income in the process of calculating the FCF.

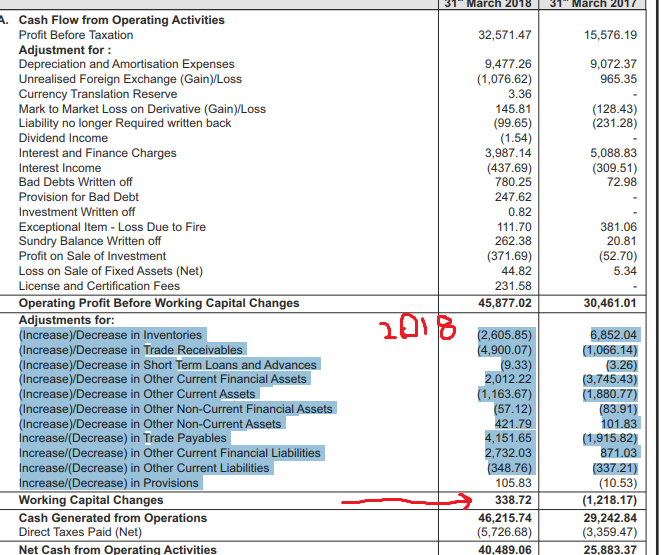

But (in order to do recheck) when i analyzed the Change in Working Capital through Cash Flow Statement, it gives completely different number (as they have also included Non Current Item).

you will observe that the working capital changes in cash flow is only 338 Lakhs (as compared to 19854 Lakhs that we have calculated using Balance Sheets)

PLease let me know if i am missing any point.

Working Capital is not the same as Net Current Assets (i.e. Current Assets - Current Liabilities). The simplest definition of ‘Working Capital’ is ‘Non-Cash Current Assets net of Non-Debt Current Liabilities’.

In this specific case, I would personally calculate a WC decrease of Rs. 454.39 Cr (i.e. A Cash Increase of Rs. 454.39 Cr):

(Download: Meghamani Organics WC Calculation.xlsx (12.3 KB))

By the way, if you refer to the Notes to Financial Statements, both ‘Non-Current Financial Assets’ and ‘Other Non-Current Assets’ seem to be just bank deposits and such, which should ideally be considered as Current Assets. Anyway, I have considered them as ‘Other Financial Assets’ for the purpose of this calculation (I have highlighted this figure in yellow).

Even still, my calculation does not actually match with what’s represented in the Cash Flow Statement of the company. It’s off by Rs. 115.67 Crores. Indeed, there are several minor discrepancies in the figures I calculated and what’s shown in the Cash Flow Statement (Highlighted here in red).

This could be an accounting adjustment, where an Accounting change has happened (Say, the sale of a Current Asset), but the cash has not been received by the company yet, therefore creating a discrepancy in Cash Flows.

2 Likes

Does the interest rate on debt for Indian companies -usually fixed or variable in nature ? And where can one understand this from the annual report or any other filings…

Hi,

Is there any way to calculate Average Sales of 3/5 years in Screener?

Hello all my friends.is there any app or site to show historical valuations of a company for atleast 5 to 10 years i.e price to book price to earnings price to sales ?

www.ratestar.in does show you that on the chart.

3 Likes

check valueresearchonline.com, where they show march 31 year end nos. like market cap, BV, PE, Closing Price etc…in their Financials Tab.

3 Likes

I was looking into the P&L of ThomasCook India and was not able to make out the PBT: the PBT for last year has increased from 248 to 5999 crores, is this because it was able to sell the Quess Corp? Does that mean that the company is having lot of reserves?

Usually variable. Yes, you can search for interest rates in the annual report. An abstract way would be to calculate ‘Interest Paid / Borrowings’ from the financials.

There’s no direct way. But perhaps you could try this:

- Sales and Previous Sales are already available

- If you do Sales / (1+3yr Sales Growth)^3, you’ll get Sales from 3 years back

- If you do Sales / (1+5yr Sales Growth)^5, you’ll get Sales from 5 years back

- There’s no way to get Sales from 4 years back

Add Step 1, Step 2, Step 3 and divide by 4. This should be a good proxy for 5yr Average Sales.

2 Likes

Thanks. It is working.

Let’s say I want to figure out the following for a particular company.

- Has the promoter purchased a particular stock recently?

- Has a particular individual purchased a particular stock recently - say I want to find out if Ratan Tata has purchased any Yes Bank shares in his personal capacity?

- Has a particular foreign fund (hedge or mutual fund) - say I want to figure out if Oakmark Emerging Markets fund purchased any Repco Home Finance stock recently?

Is there an easy way to find this information regularly?