You should refer to Risk Adjusted Return to understand this better. The most famous measure of Risk Adjusted Return is the Sharpe Ratio, which is also described in the text given in the image.

Sharpe Ratio = (Return from Asset - Return from Market) / Standard Deviation of Asset

As far as the way it’s represented in this graph, the top-left corner of the graph is the ideal place to be in (Lowest Risk, Highest Return). So, it looks like one peer has earned a higher return, but also has a higher Risk. Kajaria seems to have a lower risk and return both. It’s very difficult to make and apples-to-apples comparison here, because IMHO we have not even scratched the surface with understanding Risk. At the best, I can say that a graph of this sort can give an investor a variety of choices as to what kind of Risk he can tolerate vis-a-vis what kind of returns he expects.

Risk Adjusted Returns are largely used to judge the performance of a Fund Manager on a portfolio level. I don’t think it works well as an investing tool. Motley Fool did a nice article on the fallacies of investing, which covered Risk Adjusted Returns.

Hi, Im a newbie, learning to analyse financial statements. How is Cost of goods sold calculated?

Can I arrive at COGS by adding cost of materials consumed and purchase of stock in trade from the Income statement? Or is there more to it?

Hi guys, I have a small query regarding growth rate of a company . When we talk about growth rate ,does it means revenue growth rate of a company or EPS growth rate ?

Thanks in advance

I bought a stock at 430 RS but now its down to 300rs , I need a simple formula to find how many stocks do it need to buy to average the current trading price

If a company like excel crop care is going to merge a company named sumitomo chemical which seems to me is unlisted, then how i analyse this as a excel crop care shareholder.

Number of shares=[(PA)F1 - (P1)F1]/[P2 - PA]

PA = preferred avarage price of the stock after you buy the stocks second time

P1 = price of the stock when you bought first time

F1= number of stocks bought first time

P2= price of the stock when you buy second time

I have very few basic doubts regarding Upper Circuits

If a stock is in upper circuit,can a retail investor buy the stock( i tried but I could not as there were no sellers)

How is it decided that a particular stock should be in upper circuit

How come the price of the stock goes by a fixed percentage (either 5 or 10% or 20%) and how is the percentage decided @dineshssairam@Gaurav_Agarwal@phreakv6

Nobody can buy anything if there is no seller. If a seller comes for with small quantity, someone who has put a bid first should get those shares. I do not know how stock exchanges queue such bids. I assume this should be first come first serve basis.

Circuit fillers are applied by stock exchanges according to rules framed by SEBI. If you go to BSE website and search for the stock. On stock page you can find the circuit limit for that particular day.

Thank you brother .That answers a part of the question.

But I am not sure how SEBI decides that a particular stock should be on UC and by how much percent

@bala.y.krishna, Say e.g. I buy 25 shares of jagaran Prakashan@ 175.

I want the average to be 140

CMP is 130

Then number of shares I have to buy=

[140(25)- 175(25)]/[130 - 140] = 87.5

Approximately 88 stocks have to be bought.

In your case since the CMP is 300 and the average can’t be 300 again. Theoretically one has to buy infinitely many stocks to make that happen as you can see when you substitute in the formula. But for any other value it can be found using the same formula.

Hope it helps

Hi everyone, just had a question that has been bugging me. I read Prof Aswath Damodaran’s recent article on “Share Count Confusion”, where he writes:

“If Tesla is able to issue shares at a higher price (than its intrinsic value), we will have over estimated the value per share, and if it has to issue shares at a price lower than its intrinsic value, we will have under estimated value.”

I am thinking, he inadvertently wrote that backwards. Shouldn’t it be the other way around?

Link to the article:

Thanks in advance to anyone who can clear things for me!

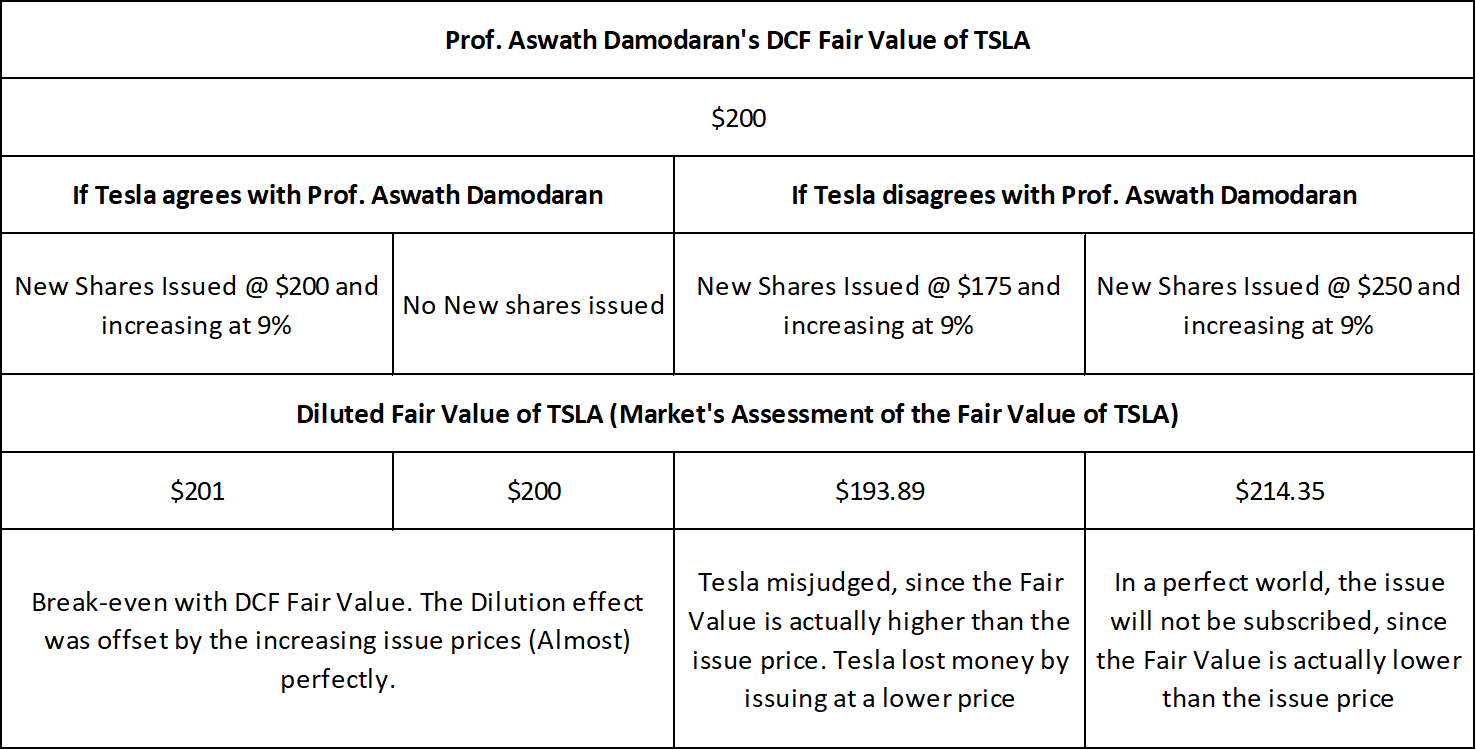

According to the Professor’s estimates, Tesla is fairly Valued at $200. And based on this initial issuance price, he is assuming that Tesla will issue newer shares at slightly higher prices every year for 8 years ($218 - $398.51). In doing so, the fair value of $200 rises to $201.92 (Because of dilution). But what the Professor is trying to state here is that, Tesla’s Value via the DCF approach ($200) and the Value via the Dilution approach ($201.92) is almost equal, regardless of the Dilution effect (You can consider it a break-even of sorts, where the dilution offsets the increased issuance prices).

However, if you assume that Telsa issues Shares at $250, the Value via the Dilution approach drops to $214.35. On the other hand, if Telsa issues shares at $175, the Value via the Dilution approach increases to $193.89. You have to understand that both $250/$214.35 and $175/$193.89 are the Value of Telsa now/in the same period. But at these higher/lower initial issuance prices i.e. alternative intrinsic values, the break-even is lost. You can input $250 and $175 in place of the $200 in the spreadsheet and see for yourself.

The Prof. is simply trying to prove a point, which he mentions just a little ahead of this seemingly confusing exercise: “If you are doing a discounted cash flow valuation, the right response to the expected dilution is to do nothing. That may sound too good to be true, but it is true, and here is why. The aggregate value of equity that you compute today includes the present value of expected cash flows, including the negative cash flows in the up front years. The latter will reduce the present value (value of operating assets), and that reduction captures the dilution effect. You can divide the value of equity by the number of share outstanding today, and you will have already incorporated dilution.”

So when you write “However, if you assume that Tesla issues Shares at $250, the Value via the Dilution approach drops to $214.35.”, you mean drops in relation to what? To me it seems it increases in relation to the previous number, which was 201.92

Same question for “On the other hand, if Tesla issues shares at $175, the Value via the Dilution approach increases to $193.89.”, you mean increases in relation to what?

I understand the overall concept, but this is what the confusion is about!

If the company is able to issue shares in the future at a price much higher than our current estimate of intrinsic value, how can we have over-estimated the value of the original share?

Let me try to explain this step-by-step (So that I myself don’t get confused in the process):

The Professor considers $200 to be the intrinsic value of Tesla. He used a DCF to arrive at this.

If Telsa issues new shares starting at $200, increasing at a CAGR of 9% for 8 years, the intrinsic value via Dilution Method would be $201 (Which is almost equal to $200)

If Tesla issues new shares starting at $250 instead (That is to say, if we assume that the Professor is wrong and the intrinsic value is actually $250), we find out that the intrinsic value via the Dilution Method is actually $ 214.35 (Which is lesser than $250, our assessed intrinsic value of Telsa). So really, why would Tesla issue new shares at $250, when the market thinks that the shares are only worth $214.35? They would just go buy the shares from the market, if they wanted to.

If Tesla issues new shares starting at $175 instead (Again, assuming that the Professor is wrong and the intrinsic value is only $175), we find out that the intrinsic value via the Dilution Method is actually $193.89 (Which is higher than $175, our assessed intrinsic value). In essence, Tesla misjudged their Market Value and issued at a price lesser than their intrinsic value.

In short, it’s a circular reasoning problem, highlighting the problems of share dilution / ESOP issues. It looks complicated, because it is.

The solution offered by the Professor is summed up in his own words:

“The Right Response: If you are doing a discounted cash flow valuation, the right response to the expected dilution is to do nothing. That may sound too good to be true, but it is true, and here is why. The aggregate value of equity that you compute today includes the present value of expected cash flows, including the negative cash flows in the up front years. The latter will reduce the present value (value of operating assets), and that reduction captures the dilution effect. You can divide the value of equity by the number of share outstanding today, and you will have already incorporated dilution.” (Source)

Footnotes:

Of course, the win case for Tesla is if it issue shares at $250 and it actually gets fully subscribed, which could very well happen in an irrational market.

On the other hand, even if Tesla issues at $175, it could very well use that money to produce more cash flows than the Professor actually assumed and so, be worth more than $200 (His assessment of Tesla’s Intrinsic Value). This would again be a win for Tesla.

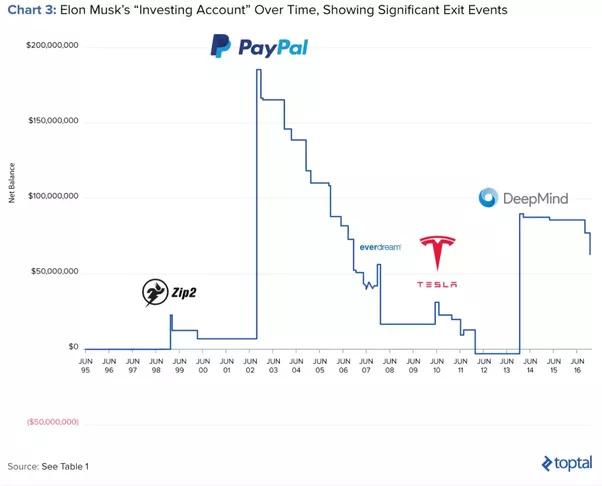

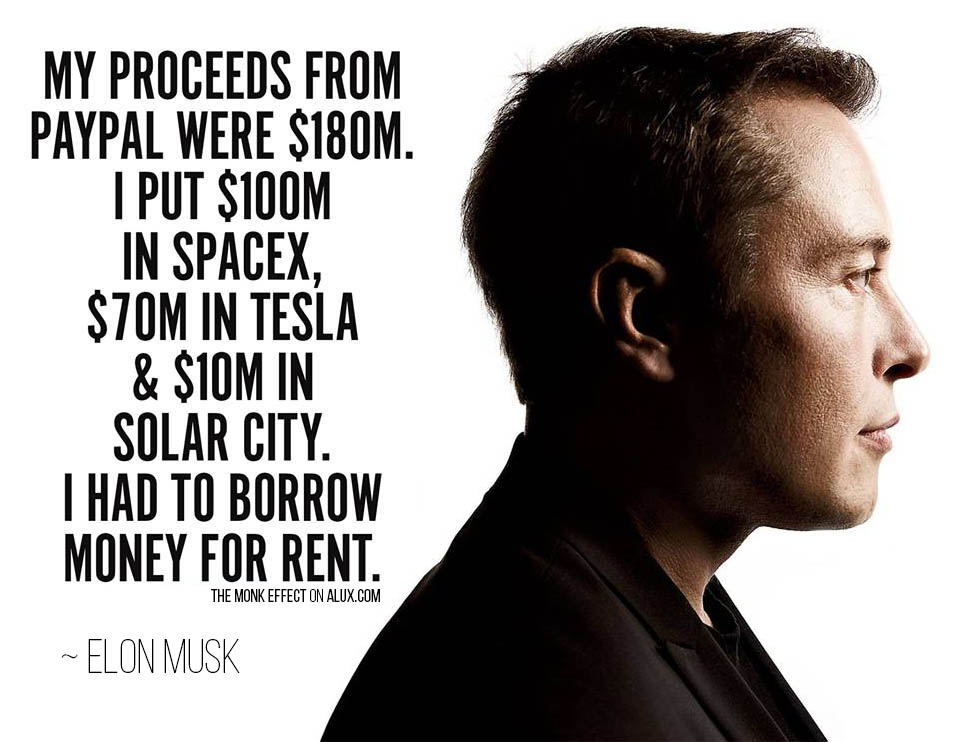

Unfortunately, keeping all estimations aside for a moment, Tesla actually trades at $345, way above all this. The only win I see for Tesla is if magically starts tripling its production (Especially of the Model 3) or if some deep-pocketed crazy person worth Billions of Dollars is crazy enough to lose money in order to allow Tesla to survive, and eventually win. A silver lining is that, Elon Musk is that crazy person. Look at his investing history, starting with PayPal - it’s a vicious chain of equally crazy and bold decisions:

I will go so far to say Tesla is Musk. It will make it or break it with him. If that sounds ridiculous, how about this:

I personally don’t identify with such a massive amount of risk tolerance. But you’ve got to give it to him for consistently disproving his critics and re-defining what’s possible.

Thanks for the detailed reply. Really appreciate it.

Whatever be the Prof’s estimate of intrinsic value via DCF, the intrinsic value via the Dilution Method would still be similar. It doesn’t matter what the estimate is, 200, 275, 150, or any other value. I get that.

I want to make my limited point though:

Given any intrinsic value arrived at by the Prof (or anyone else), if the company is able to issue shares at a much higher level (in this case, the market price for the shares is higher than the Prof’s estimate), the Prof’s estimate of intrinsic value will have to be revised upwards (in my opinion). That is, he will have under-estimated the value per share originally.

The same logic applies in case the company has to issue shares at a lower price than the Prof’s estimate. In this case, the Prof’s estimate will have to be revised downwards. That is, (in hindsight) he will have over-estimated the value per share originally.

Hence, I think his statement in the article is wrong.

“If Tesla is able to issue shares at a higher price (than its intrinsic value), we will have over estimated the value per share, and if it has to issue shares at a price lower than its intrinsic value, we will have under estimated value.”

As I said, I understand what he is trying to say (I have been reading his work since years), but the above sentence doesn’t make sense to me. That is my limited point.

Hi everyone, just want to know if Exchange has sought clarification from company regarding some specific News comes into Media than is there any time frame decided in which Company need to reply.

If company will not reply than what kind of actions Exchange will take or nobody bother in Exchange if Co. do not provide any clarification.