There is no fixed rule. What I do once the price falls after I buy depends on my conviction. If I am very combined I will buy more. If my conviction is less I will probably sell and preserve capital if the story is not playing out as anticipated.

There are lots of books on Indian businesses, though not as many as US ones. You can strt with Business Maharajas/Legends by Gita Piramal. Recently there are quite a few new ones like Bandhan - the making of a bank, Havell’s - the untold story, business the emani way etc.

Thank you so much. In my case what happens, generally do not keep cash in hands to buy more on price fall. Then have to wait and watch but in this case price may fall to way lower level and hard to average at current price. I will start looking into capital allocation framework.

Is it advisable to keep stocks which have v low allocation in your portfolio (less than 1% or may be less than .5%). It becomes v difficult to manage these and track the companies. But if the portfolio becomes large , small allocations like less than .5% also looks a decent amount in absolute no.s

Should we sell these and reallocate them to higher weightage stocks ? or we can ignore it and let them be in considering a v less allocation. Because .5% on 100 rupees is only 50 paisa but on 1 crore it becomes 50 thousands. What should be the minimum and maximum allocation of a stock in a well diversified efficient portfolio.

@Rohitsharma,

Investing is (mostly) an art so they may not be any correct or wrong answers. What I do is, aim to have atleast 2% allocation per stock. If it is not 2% yet, then I will increase allocation. For increasing allocation, I will do only when I’ve strong conviction. So, if I’m not convinced I will sell.

But sometimes we may receive a stock as bonus. For example, Sundaram Finanace demerged their investment holdings in a separate company and gave Sundaram Finanace Holdings. Thomas Cook will also demerge Quess shortly. In this case, I would maintain a separate demat account for low allocations or gift/transfer my holdings to my wife’s demat.

Generally, I will sell my low allocation stocks and add to higher weigtage stock.

Is there a parameter which can tell incremental capital required for incremental sales growth.

For example. If sales has to grow by 1 % next year then how much more capital company has to invest overall in the business for that 1% more sales?

Consider a company ABC has NET PAT almost equal to net CFO over the last 10 years.

The company has been growing at a very good rate and am happy to pay the PE it demands,just by analysing the net CFO and net PAT it has earned over the last 10 years

However, the amount of trade receivables have been increasing ,which is almost equal to half of Net CFO collected over the last 10 years

Trade Receivables= Half of Net CFO.

Should I be worried about increasing receivables, even though am happy with net CFO over the last 10 years .Should it be a red flag

My query is whether Trade receivables is factored as part of Net CFO or not?

Yes, it does. Net CFO typically accounts for an increase in Trade Receivables (i.e. Net CFO = Net Profit - Increase in Trade Receivables). But it’d be useful if you disclose the name of the specific company, so that further inquiry may be done.

Just FYI, Ind AS 7 outlines the rules related to Cash Flow Statement, where you can also see the definition on the treatment of receivables (Points #19 and #20).

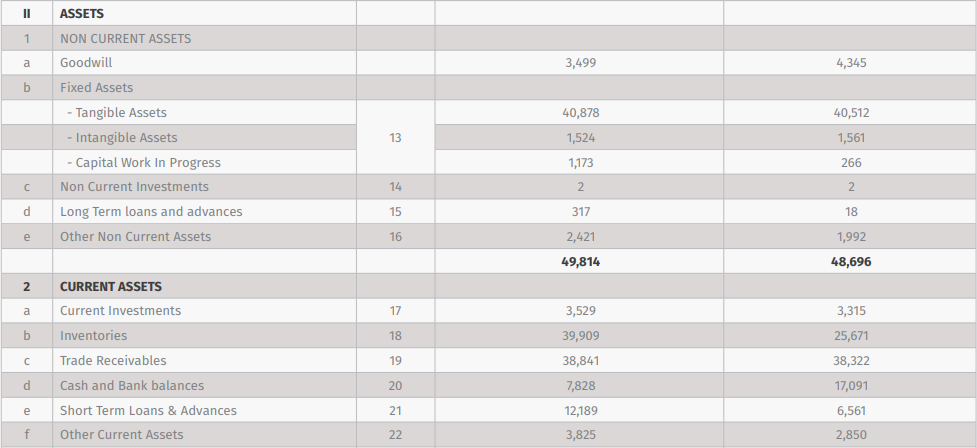

However the receivables as on 2017 annual report was 130 crores which is almost half of CFO for the last 10 years.This has led to the confusion between Trade receivables and Net CFO

The company consolidated q4 numbers are yet to be released and reason cited for delay was “challenges in adopting of New Ind-AS accounting standards” and they have new Auditor ‘Deloitte’

I have one more question related to above data mentioned in the last post:-

Assume for some reason receivables become 0, then the cumulative CFO figure of 280.16 will be more or less or remain same?

(Also I assume cumulative PAT will remain same at 219.55. Correct me if I am wrong)

Sorry for putting my question in between, but i was looking for answer to above since long.

Hi Everyone, This forum has been of great help in learning the ropes of investing.

I have a basic question related to the calculation of capex.

From one of the blogs capex is calculated as follows

Capex:

(GFA + CWIP) at the end of the year – (GFA + CWIP) at the start of the year

OR

(NFA + CWIP) at the end of the year – (NFA + CWIP) at the start of the year + Depreciation for the year

I was trying to calculate the Capex for the below balance sheet but couldnt figure out which is GFA and NFA.

can some one help me with this.

If a small retail investor wants to visit the plants/manufacturing units/offices of the companies just to see the ground reality. Do they allow them ? if yes, what is the procedure for it ? To whom one should contact ?

If they don’t allow , than how can we verify these ? like how are the plants and manufacturing processes ? Do we have to rely on annual and market reports only ?

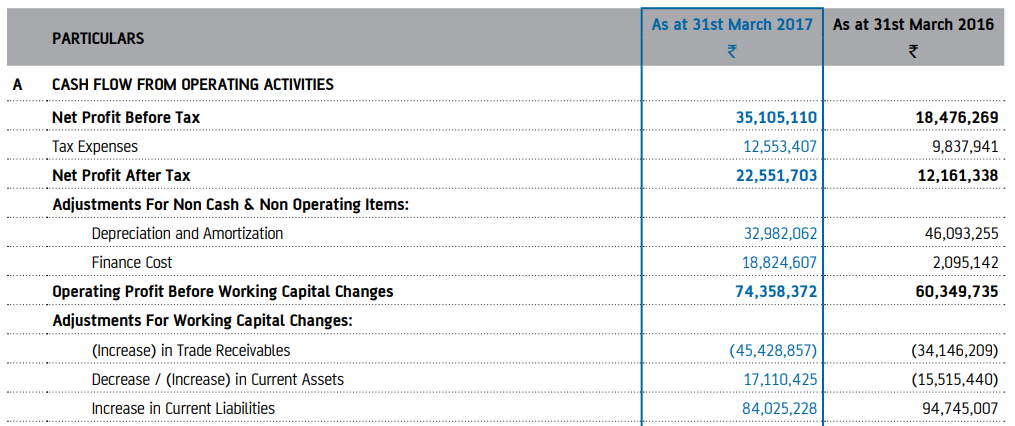

It looks like while Trade Receivables has increased, Trade Payables/Current Liabilities have also increased:

This might have led to the offsetting effect, resulting in CFO not being affected so much. But very high Payables/Receivables are not objectively good unless its in the nature of the business (Ex: FMCG). You should definitely pursue inquiry along these lines.

Hi all,

I am trying to create a check list for large cap stock. Can anyone suggest me what are the check list must required before buying any large cap stock ??

Thanks in advance…

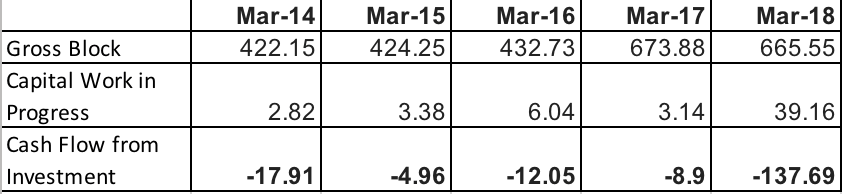

This is from Nocil, In Mar-17 gross block increased significantly however there was no mention of this investment in cash flow from investment. Where did this Gross block increase come from.

This is due to increase in carrying value of fixed assets consequent upon using fair value as deemed cost. Please see the notes on First Time Adoption of Ind (AS) on Page 60 & 61.

@Chandragupta : Thank you for your response. I looked at AR and found there gross block value is different from the one I mentioned above which is from screener

Even if its incorrect, then is there any direct relation between gross block and cash flow from investing ?

Can you please explain little more on how the gross block is effected by accounting rule you mentioned.

EDIT

Looked at this years AR and found the mentioned of accounting standard change you mentioned. It seems they changed it retrospectively hence screen shot posted above from last year AR is not matching this years data and the screener. Thanks