One of the general concerns with PSBs is that a healthy bank might be merged with an ailing one.

Just want to confirm that this cannot be done with Jammu and Kashmir Bank since it is not owned by Government of India.

Thanks

One of the general concerns with PSBs is that a healthy bank might be merged with an ailing one.

Just want to confirm that this cannot be done with Jammu and Kashmir Bank since it is not owned by Government of India.

Thanks

Can anyone explain this?

I was going through the annual report of signet industries 2017 .Page 30 says the promoter shareholding is 51.84 ,but in the explanation it is given that the promoter shareholding is at 73.58 and that the remaining shares are struck at the clearing members.How to interpret this?The promoters have been trading in their own shares?And that too a huge number of shares!!!Are they essentially manipulating the stock price?

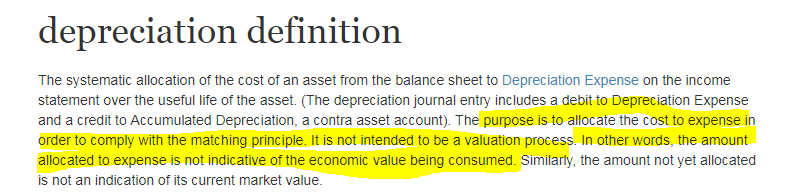

MY QUESTION IS REGARDING DEPRECIATION

Question:In income statement many times the maintenance charges are deducted.(ie maintenance of machinery,maintenance of building).Now often it varies from the depreciation charges for the year.My question is since depreciation is a not physically paid out,it is an amount that is held by the company,even though it is not shown in the balance sheet.

PART 1:What does the company do with this depreciation money,which is not reflected on the balance sheet?(it is not reflected in the netblock)Please answer

PART2:If let us say that the depreciation charged for the year is 15 crore and already the maintenance charges are deducted in the income statement,what is the purpose of depreciation?Is it only to claim tax benefits?Or is their any other reason.

PART3:If the company is already maintaining the plant,then technically the net income of the company is more by 15 crore(the depreciation charge).Then are companies more profitable than they look?

SPECIFICALLY I WANT AN OPINION REGARDING EVER READY INDUSTRIES annual report 2017 page 144.Clearly the other expenses include repairs and maintainence of plant ,machinery and software.Then what is the point of a seperate depreciation charge of 15 crore on the income statement?

Part 1: depreciation is an accounting entry which is of course reflected in the balance sheet as accumulated depreciation. This is a negative entry against fixed assets. The effect of this entry will be reduction in the value of corresponding fixed asset every year.

Part 2: maintenance charges is different to depreciation charges. For example, take a car which might have an useful life of 10 years after which time it needs to be replaced. Maintenance charges are all charges in the 10 years relating to replacement of spares, regular servicing etc which might occur more frequently. Depreciation is a provision which will enable to replace the car itself after 10 years. The tax part is it is not possible to claim a capital expenditure (put simply an asset with useful life of more than one year) straight away and it has to be claimed as depreciation over the useful life. That is we cannot claim the whole car as expense in year 1. We need to claim over 10 years as depreciation.

3. Company is not generally more profitable than they look as depreciation is a real expense as well. The company will need to replace the asset after useful life and therefore incurs the depreciation expense in year 1 itself than over its life. However the cash profit can be more than accounting profit as the corresponding expense will have already been incurred in year 1 and from year 2 onwards this will be only an accounting entry.

Thanks for the reply,

It seems i have not made myself clear in the previous question,let me give a specific example.

In 2017 eveready paid almost 13 crore as repairs to machinery,buildings and software as a part of other expenses in the income statement.You can look it up in 2017 annual report Page 144 .Then the company also deducts 15 crore as depreciation expense.Now depreciation is not a physical charge,in that you are not paying it to someone.It is held by the company as you said in a contra account to the fixed assets…

My question is many people say that depreciation is a approximate estimate of maintenance expense and hence is deducted to account for maintenance .But here the company is already paying for maintenance of plant and machinery.

Secondly,Let us say a company bought a machinery worth 100 crore and deducts 10 crore depreciation every year,then will the company have about 50 crore worth cash in its account by YEAR 5, and 90 crore by year 9?Since it does not have to replace the machinery till year 10(assuming the machine does not become obsolete before)

Thirdly,where exactly is this cash related to depreciation held physically?I am not asking in which account is it held?I am asking in a physical sense .In bank accounts?as cash?

Depreciation is not an approximate expense for maintenance as maintenance and repair are on top of depreciation. Depreciation is an approximate expense to replace the relevant fixed asset after its useful life.

In the first year, when the company spends Rs100 it is not expensed straight away. Only Rs10 is expensed as depreciation, although it spends whole Rs100 in year 1. This means it shows Rs90 this year as additional income although it already spent Rs100. From year 2, it only reduces the additional income Shown in year 1 and therefore does not have any additional cash from depreciation.

Cash in relation to depreciation is not held physically as it has already been spent in purchasing that asset. So the depreciation amount is only a reduction in value of the relevant asset.

I am not sure if i follow you.How can depreciation which is calculated using historical cost,be a useful estimate of replacing the asset after its useful life?

Secondly,I know for a fact that ,whenever a company purchases a fixed asset like machinery for cash,then they dont have to show it on the income statement.The only entries recorded are credit cash and debit fixed asset.There is no debit or credit to an income statement account.

I am not sure how to deal with this .

Would anyone give a clearer picture regarding the above question?

Depreciation is not a science. The percentage of depreciation and even the life of an Asset are all assumed. The major aim is to facilitate a true and fair view of the financials and also allow for cash reserves in case the Asset needs replacement.

My question here is depreciation is not a physical flow,so let us say the company sells goods for 100 crore to its customers,it receives physical cash.Then it pays for raw materials to its suppliers pays for marketing,pays salaries to its employees,pays finance cost to banks and taxes to government.All these are physical outflows.However depreciation is a non physical cash flow as it is not paid to someone.SO let us say if a company has a depreciation of 10 crore and net profit of 2 crore,then the company actually retains 12 crore,as it does not have to pay depreciation to anyone else.

My question is basically where does this money get stored?Is it stored as cash?

Another question that arises is lot of indian companies deduct a separate expense called repairs to machinery in the income statement.It is often clubbed under ‘other expense’.Generally plant and machinery make the largest part of the fixed assets ,but they have a long life 20-30 years,then one Valuer of the company may say let me make 12 crore each year(adding back depreciation 10 crore to profit 2 crore) as long as i can and sell off the assets for salvage value(he does not intend to replace the assets i.e run the company after a while).He may say that if he can run the company for atleast 7 years,he may make 12*7 =84 crore,whereas relying on the profit alone he will never be willing to pay 84 crore for the company which is almost 42 p/e (84/2)

Look when company buys asset of say 100 cr then where do they get money for it ? The first option is to call your reserves and second is to take debt. Lets assume they bought the assets from reserves, now 100cr has gone in one single instance and in that year asset should be expensed completely in the P&L statement but what company does is expense it linearly over a period of time so that it wont affect the P&L disproportionately. Now when company expense say 10cr as depreciation charges than that is not a cash outflow but an accounting expense since the cash has already been flown out.

Hope I’ve made myself clear.

Thanks

I totally agree that we dont need to understand these accounting technicalities in detail,but according to gurus like bruce greenwald,even though cash flow from operation is what we make ,we need to deduct back depreciation ,because depreciation is an estimate for the maintenance expenses of the company.But in india not only do companies deduct depreciation,but also pay for maintenance of the company seperately.

ALL companies add back Depreciation in the Cash Flow Statement. If there’s a company which doesn’t do that, that’s a bad Accounting practice.

I think you misunderstand what Greenwald said. He probably meant that an investor needs to add Depreciation back when trying to Value a company.

If you look into the article,people there have taken depreciation to mean an estimate of maintenance capex.However indian companies already record expenses of repairs to plant and machinery in the income statement.So what is the point of deducting depreciation?Again i may be missing something here,but as suggested in the article if depreciation is a rough estimate of the company’s maintenance ,then if the company already deducts maintenance charges,then there is no reason to deduct depreciation from the CFO.

Depreciation is not the rough estimate of maintenance. It is rough estimate of value lost from the asset you already own. That is to arrive at the book value.

If you bought an asset for 10 lakhs and you depreciated for 10% every year in straight line method, at the end of 7 years, the maths will be like this.

Year 1 - 10 lakhs

Year 7 - 3 lakhs assets (after 7 lakhs value depreciated)

So the book value will be 3 lakhs of the asset, but not the actual worth of the asset, that would be different because the asset may even last for another 10 years. So someone may be ready to buy these assets for 5 lakhs.

Here the fuel cost and maintenance cost is totally not in the picture. They have been expended off in the income statements all these years. Even the depreciation gets expended off.

I have a question . Would appreciate if someone can guide on this.

When we look for the commodity or raw material prices which are used in an industry , we should search for the domestic prices trends or international prices trend. Quiet possible that company may buy in domestic markets , international markets or may be both. How to be sure of this,

For example , if a chemical company is buying some chemical as raw materials , how do we know its buying from domestic or international market, Since prices may vary in both markets. Also I know their should be a positive correlation in both the markets but to what extent.

Depreciation is not a cash flow which will go out or come in. It is an accounting entry. That’s why the accumulated depreciation amount is added back in net profit while calculating cash flows.

You have paid the cash and got it converted to asset. So the money is gone here.

Later on your asset loses its value, that is depreciation. Money doesn’t move here.

In income statement since every year you deduct the depreciation, for the actual cash flow purpose, you are asked to add the depreciation.

Hope this answers your doubt.

Revist all the answers you will gradually understand everyone is trying to say the same thing in different perspective.

Notes to the Accounts usually gives the break up of Raw Material Imported and Raw Material Indigenous. Director’s Report also mentions at the end Foreign Exchange Used and Foreign Exchange Earned which can give an indication.

Actually my doubt had been different.I got a good link written by professor gleenblatt which answered my doubt.

My original doubt was why indian companies were not only paying for repairs of machinery and at the same time deducting depreciation(which prof greenwald says estimates maintenance capex).

My mistake was that i was thinking maintenance capex of the assets was the same as repairs to the company’s assets.

Thanks everyone for the help.