I agree with your assement. I just feel there could be headwinds in this sector for near term. #2 could be hard with competition and I feel it could reflect in the top line as well.

I like the business, just feel the current valuations are not justified especially with crude going up.

Article on Business Standard about why Aditya Ghosh had to quit.

The article states that Aditya Gosh was not focusing on Customer satisfaction on issues like Pratt and Whitney engines grounded, groundstaff mishandling a passenger. Also the issue of shifting the terminal.

While I’m not sure how they got the exact info from, that does make sense to me. One thing that stands out and might not be good for company is that the company is planning to have different sized flights based on distance.

Besides growing in size, the airline is also looking at an overhaul of strategy, shifting gears from having a single aircraft variety to wide-body aircraft for long-haul operations.

“Sebi is examining the cause for the worst drop in seven months in InterGlobe Aviation shares before the company announced the resignation of its president Aditya Ghosh”. “The market regulator is investigating a 6.1% drop in the company’s shares on 27 April as well as the reasons behind the delay in the disclosure of Aditya Ghosh’s exit by the company”

My opinion is that these matters of high profile exits get known or well anticipated within the organization in spite of best efforts to keep them confidential.

Therefore fall in share price was eventual and an individual,s departure however good he or she maybe, may not affect the well established systems at indigo.

Stock down from ~1490 levels when I posted this to 1190 today due to high fuel costs in Q4 earnings. Do you still think a stock with inherent commodity exposure can command a ~20x multiple to earnings on decade low oil prices? Try looking at global airline comps (even in fast growing markets for tourism such as China/SE Asia) and you’ll not find more than a handful of airlines more expensive than Indigo.

How to make a balance between absolute valuation using DCF and relative valuation using PE or PB ratio…even at a price of 1300, the indigo is fairly priced on the basis of DCF model…and correctly so because of the large cash its holding it is capable of exploiting new opportunities for growth…

Assumed FCF Growth

Year 1-3

10%

Year 4-6

8%

Year 7-10

6%

Discount Rate

10%

With the above assumptions which are quite modest in my view as this year also company has grown by 15%, the stock is fairly valued at 1300…the cash holding have further improved this fiscal…

Discount rate of 10% for such a risky business is unrealistic. I would use something like 18% as the discount rate for this business. Also I am not sure on what basis are these FCF growth rates arrived at. Would be helpful if you elaborate on this.

I have following observations with respect to indigo -

Company has got 12923 cr in as current assets…if we reduce a long term debt of 2241 cr from it the company has huge surplus cash…per share it comes out to be Rs 278…now as per my reading of peter lynch book, buying one share of indigo will also give you Rs 278 cash…so effective value of that stock is somewhere Rs 928 today…this will give us a PE of around 15.49…

I have uploaded an excel sheet for your reference where i have assumed a growth rate of 15% for next three years followed by decreasing growth rate…I think aviation industry in India has good scope to grow…I have taken FCF as (op cash flow-capex)…i have got the capex from morning star website…rest details in excel sheet are from screener.com…

With respect to the discount rate, indigo has generated positive cash flows since previous three years with FCF in huge excess of net profit…previous year this has been due to 1732 cr rise in payables and low capex…i think the cash flow statement shows and excellent buisness model which is able to convert all the profits into the cash…thats why total cash with the company has increased by 4000 cr this year…

so i feel a discount rate above 12-14% will be too harsh to the good reputation of the company…however we can use different values for the discount rate… Interglobe Aviat (2).xlsx (171.1 KB)

Im new to investing with few months of experience…so any contrary views are most welcome…

Good study, thanks! I too had point no. 1 in mind (And Lynch’s Chrysler example). Most airlines worldwide are in debt, hence Indigo definitely qualifies among the handful that Sarang mentioned.

I also feel growth of 15% is very conservative, and hence the correct assumption for now.

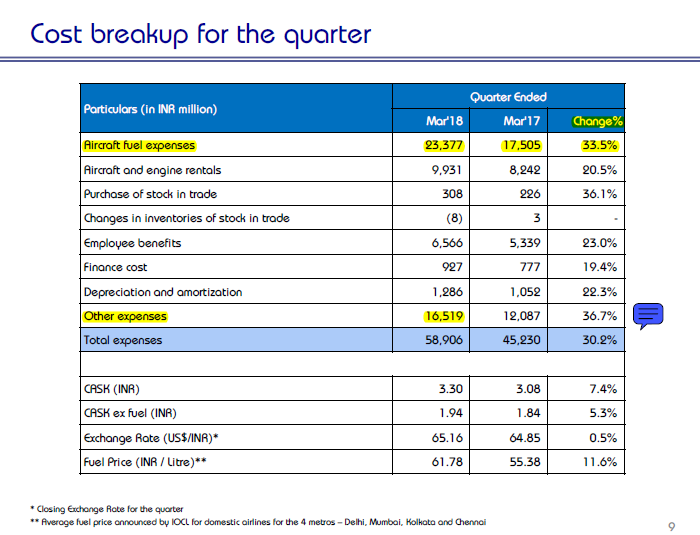

I would like to draw attention to the high “other expenses” in Q4.

Do anyone of our friends have a view on this?

At a macro level, crude my rally upto $100 depending on May 12 decision on Iran and also in run up to Aramco IPO. Definitely an amber flag for an year or so (if not red)

Yes, i have also noticed the increase in other expenses but during the conf call no one asked any questions about it…so we will have to wait for the annual report for any explanation…

Also, with a cash surplus, Indigo is better prepared for a stressful economical situation when compared to spicejet or jet airways…

As per Rahul bhatia’s views during concall, indigo will not step back from agressive fare competition as they believe that the low fares during times of higher crude price are not sustainable…Indigo is better positioned to provide low fares for a longer duration at present…management hopes for better pricing in coming times…

Today spice jet results have come out…im tracking both indigo and spice jet…however indigo has a much larger share than spice jet in my PF…

On comparison of results from the two airlines, fwg things are revealed -

Spice jet is able to attract more no. of passengers as compared to indigo…this can be seen from an increase in load factor of 95%…which means that 95 pcnt of its seats are being occupied by the pax.

Spice jet has higher yield also which has increased by 8% as compared to the decreased yield of indigo…it means that pax are willing to pay more to spicejet or spicejet is better positioned to pass the cost to pax.

But the indigo beats spicejet in terms of CASK and PASK (profit per avlb seat km)…indigo has much lower cost for seat KM than spicejet and thus a higher profit on seat KM basis…spice jet has a PASK of Rs 0.29 while indigo has 0.49 PASK…

on the basis of above comparison following inferences can be made -

Indigo has higher profitability and more focused on providing the cheapest services…but this may be leading to a deterioration in sub par services…

Spice jet is focusing on maintaining a higher load factor with better services in the same segment but this may be leading to lower profitability…

I’m myself a frequent traveller and I travelled both by SpiceJet and Indigo. As a passenger, what I felt is SpiceJet flights are more congested with respect to leg room and in flight space as compared to Indigo. Also, ticket price of Indigo is a little cheaper than SpiceJet, atleast that’s what I’ve observed whenever I booked. As far as the service goes, I don’t find any notable difference between both, and I find Indigo to be more comfortable.

Disc: Not holding SpiceJet. Indigo forms around 5% of my portfolio.

One more point is Indigo flights are a little bigger with more number of seats as compared to SpiceJet. Indigo is a 3+3 seater per row while SpiceJet is 2+3 seater as I remember. That could be one of the reasons for IndiGo’s less occupancy