Intellect announces a large multi-million destiny deal win from one of the top 20 banks in North America, for a Digital Transformation program in Payments

1 Like

https://www.bseindia.com/xml-data/corpfiling/AttachLive/bfe2a70b-4d52-4c9c-8c8e-4634804a3ac7.pdf

https://www.bseindia.com/xml-data/corpfiling/AttachLive/dfea5ef6-e38f-498e-8c9a-6714200aea56.pdf

2 Likes

How do we know what is the ILF amount initial license fee, that The company are generated. As this is a product company, I LF is very critical for long-term profitability of a company like this .

Where can I get the details?

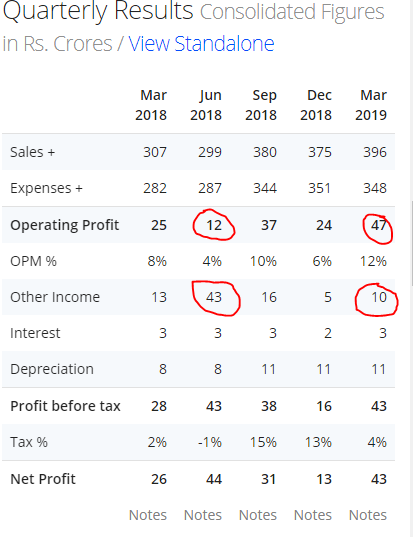

Compared to quarter 1 year ago results seem bad . But the year on year results for whole year FY19 is still good and those numbers are highlighted by management in the presentation.

Q4 YOY 32% revenue growth & 60% + pat growth in consolidated number. Results are good in all aspects. The only thing to note is other income of 37 crores towards a sale of land in annual consolidated numbers, which is one-time income, other than that it meets its projection. The market may not give a thumbs up but should hold above 200

1 Like

Now I see it… results not bad at all.

I listened to the concall of Intellect today. Some of the observations are:

Company management targets 20% cagr growth in topline.

There seems to be a healthy order pipeline for the company.

It seems to be winning big destiny deals which could be gamechanger going ahead. (they have given the details in the presentation). The number of deals and the size of deals both seems to be increasing. North American markets seem to be showing good traction now.

They are looking to exit the deals which are not too profitable.

The management says that company has now crossed the chasm and now onwards be on a good consistent growth path.

QIP plans earlier planned have now been shelved as the company now feels it doesnt need additional funds to grow. The cash burn continues even now but company seems to be on track to generate free cash flow from fy 20 onwards.

Overall it comes across as a company to keep on the watchlist.

disc: no position but on watchlist

8 Likes

The CEO of GTB was on CNBC today. One of the more interesting questions he was asked was whether IDA might look to spin off GTB. He was non commital on the issue but this got me thinking about GTB’s valuation within IDA.

According to slide 6 here GTB generated Rs678 cr in revenue in FY19 - https://www.intellectdesign.com/investor/presentations/investor-deck-2018-2019-q4.pdf

In slide 41 of their 2018 investor day presentation they guided to 30% net margin for GTB in FY19 - https://www.intellectdesign.com/investor/presentations/31-jul-2018-Driving-Digital-Leadership.pdf

This of course implies close to Rs200 cr net income for GTB in FY19.

Now depending on what PE multiple you ascribe, say 20x, does this mean the market is implying zero or even negative equity value to IDA ex-GTB???

HCL tech bought 6 or 7 product portfolio from IBM for $1,8 billion. Valuation and price are market directed. IDA with its product portfolio in full bloom may command lofty valuation for now there is risk of growth and other variables playing against it.

Intellect Global Transaction Banking (iGTB), the transaction banking and technology specialist from Intellect Design Arena Limited, announced the appointment of prolific trade thought leader David Hennah, Chairman ICC working group, Member of the World Trade Board and formerly its Co-Chair as Head of Trade Finance and Supply Chain. His appointment highlights the focus of iGTB in making their Trade Finance and Supply Chain Finance platform the market leading product across the globe.

1 Like

CRISIL has revised its outlook on the long-term bank facilities of Intellect Design Arena Limited (Intellect) to ‘Positive’ from ‘Stable’ and reaffirmed the rating at ‘CRISIL A-’ . The rating on the short-term bank facility has been reaffirmed at ‘CRISIL A2+’.

The outlook revision reflects continued improvement in Intellect’s business risk profile driven by higher market acceptance for its product suites, improving order booking, as well as healthy growth in revenues and operating profits. Expanding scale of operations will provide better fixed costs absorption, while increasing share of revenues from software licenses and developed markets will aid gross margins. The outlook revision is also supported by the steady improvement in the company’s financial risk profile, driven by healthy cash generation, and the same is expected to be sustained over the medium term.

During fiscal 2019, Intellect’s revenues increased by 33% compared to fiscal 2018 driven by large deal wins and steady monetization of the software product suites across geographies. Operational earnings before interest, tax, depreciation and amortisation (EBITDA) improved to 8.8% in fiscal 2019, from 6.9% in fiscal 2018, driven by a strong 67% growth in license revenues and higher share of revenues from advanced markets. Over the medium term, CRISIL expects Intellect’s annual revenue growth to continue at greater than 15%, backed by its healthy order backlog of (about Rs 1135 crore as of March 2019), strong deal pipeline (greater than Rs 3500 crore as of March 2019) and timely execution of large digital transformation deals. Operational EBITDA is also expected to remain at healthy levels.

The ratings continue to reflect Intellect’s growing stature as an intellectual property (IP)-led software product developer within the banking, financial services, and insurance (BFSI) domain, healthy prospects for software product companies in this domain and healthy financial risk profile. These strengths are partially offset by moderate, though improving, operating efficiencies, and exposure to intense competition in the products business.

Strengths

- Growing player in software product development and delivery, with presence across verticals within BFSI domain:

- Healthy demand prospects for product companies in BFSI:

Healthy financial risk profile:

Weakness - Moderate but improving operating profitability:

- High competitive intensity in the BFSI vertical for IT products:

Disclosure( Invested>5% of portfolio)

Amansa acquires 1.45% stake. Interesting timing, just before 1Q results.

Two Raiffeisenlandesbanks Go Live with Intellect’s Digital Trade Finance Solution

//www.bseindia.com/xml-data/corpfiling/AttachLive/69ba0929-1120-44d4-8c2e-41c74d7c1137.pdf

My con call notes from Q2-FY20 (thanks to researchbyte).

- Three accounts were cloud deals. Have not generated any revenue this quarters. If they had on-prem, we would have to celebrate differently.

- Moving to the cloud started two years back with Carter Allen.

- Current quarter costs are Rs 10 cr less than last quarters of the same year. Cost forward will around the present quarters.

- Large deal in signed in March.and implemented ahead of time.

- RTM focus on 20/21

- Cloud order book of Rs 375 cr.

- Next 6 quarters focus in Monetisation.

- For a market, we need three reference customer. After that, the sale becomes comparatively easier

- We are moving from Tier 1/Tier 2 customer in FY21/22.

- License fee deferral this quarters- double-digit million number. Purely license.

- Order book stagnant for last 4 quarters- Last 2 quarters slow on license booking.

- Capital requirement- No need to raise capital for 2/3 years (not sure if I heard it correctly).

- 50% of deals we are implementing in the cloud. Most of US demand in SAAS model.

- PE player does a multiple of 5/10 times revenue, not on PAT for cloud revenue.

- Traction for a partner is increasing. Large deal which we won along with IBM as a partner. We are going to US with IBM.

- The large deal may come in Q3 or Q4, but it is double digits—> More in Q4.

- We are aiming for 25% EBITA growth this year (and for the next five months).

- Become cash flow positive in Q1. We will become cash flow positive (Q4 will be) when we cross 50 million (not sure if it annual).

Note- I have tried my best to capture some points and there could be some discrepancy, please double check.

My thoughts

Cloud migration is causing a strain on IDA (Intellect Design Arena) reported number. Due to the nature of the cloud deals, it is unlikely to change rapidly. Instead, it will take its own time.

Even if the company is reporting PAT, it is consuming a lot of cash, and from Q4 onwards, they are expecting cash positive. Hopefully, that will lessen the need for capital going forward.

Intellect has branched out in too many product areas and trying to eat too much than they can digest. For example, they are investing in lot of products which covered banking and insurance segment. Product requires a huge upfront investment, which they have been doing it. But the cloud market is making it difficult for them to earn upfront license fee, as a result straining their balance sheet/profit.

Intellect is in a technology business, but they have certainly been very late in the cloud market. In their own word, their clouds sales started two years back, means despite in technology business and talking about buzzwords such as AI/ML/Digital and many more; they failed to get on cloud earlier. Now they have good traction in the market based on management comments, but certainly, they are playing catch up and facing the brunt from an investor in term of expectation mismatch.

The nature of the cloud market is such that the leader take the most business, and I can see Intellect has few products which are a leader or moving towards that direction in their own area. As per Annual report of FY19 four of the twelve products are ranked number 2 in their respective category by a research firm (e.g Gartner) In the cloud as the customer does not invest significant amount upfront, the critical factor for them is the functionality of the product. Hence the product which has good features- likely to the leading product- get the most customer. Hence, ,in my view IDA is well placed to reap the reward in future, but the cloud is throwing some spinner in their part so far. I think management is too much focus on license revenue which is fair, but as the market is migrating slowly (and later faster) towards the cloud, the management needs to settle their and investor exceptions realistically.

I agree to Mr Jain statement that the Indian market is not valuing company properly as the market so far focusing on valuing service company. Not many product companies and certainly not many cloud focus companies in Indian market which are successful; however, I do not expect the market to change the perception of cloud player soon. If IDA wants a different result, they have to change their approach or do thing little differently (e.g selling some products/spin-off of profitable product)

Someone suggested in earlier link about divestment of some product- I think that could be a game-changer, but it depends if Intellect wants to pursue that options. I am not sure if they have indicated it earlier, but it could be a catalyst.

I am trying to find out their monetisation plan but could not find out. I would appreciate if someone can throw some light on their monetisation plan.

Disclaimer- Invested for some time.

12 Likes

1 Like

Accolades from research companies- this time from Celnet for IDC product. The current version of the product (IDC 19.1) is announced as a winner amongst 14 vendor in Asia/Europe and Latin America.

I could not find the details reports on net, but I presume most of the 14 vendors will be top in their category. This goes in line with Intellect’s commentary that their 4 products (of the 15) are in top two in their respective category.

1 Like

One of the Business unit Heads for an emerging Vertical (Insurance) Resigned

https://www.intellectdesign.com/investor/notice/intimation-of-resignation-revised-02-07-2020.pdf

Any comments on Intellect after the Quarterly Results ?

Disc: Invested with a small position after latest quarterly results. Looking to add more.

The results just came out yesterday - any insights?

Results are good, and the management commentary is extremely strong and their narrative is that monetization phase has started. Their business model has moved to cloud subscription instead of one time license sale (I think couple of quarters back). So it is difficult to compare with revenues 1 to 2 years ago. It is complex product to understand and hence essentially we are trusting the management with their forward looking statements. The current valuations are not high in my view.

Note: Invested for long time.

1 Like