Infobeans technologies (NSE SME listed) to be a good fundamental value pick. It’s continuous growth story.

It’s current mcap is around 170 crore and free float mcap is around 45 crore. (market price is around 70 rs).

Promotor holding is 74%. It’s ipo price was 58.

Company Description:

InfoBeans Technologies Ltd (ITL) is engaged in software development services, specializing in business application development for web and mobile and operate at Capability Maturity Model Integration (CMMI) level 3. ITL services can be broadly categorised as storage; Virtualisation, Media, Publishing and eCommerce. In India it operates out of 2 facilities in Indore and Pune employing more than 600 people across locations. As the company has prominence in exports, it has established local presence in the North American market by way of a 100% subsidiary, which has 2 offices located in California Georgia, USA. ITL is ServiceNow partner for implementing their software

This company is listed on NSE SME. It’s CAGR is > 20% in last 5 year.

Investor Presentation (after Q4 March 2019)

INFOBEAN_03052019150338_NSE_INTIMATIONTFORPPT_138.pdf (3.9 MB)

Resource retaining is always challenge to any IT company. If we see this company top level management, all are associated with this company since long time which is eventually benefiting to company.

Company has presence in North America, Europe and Dubai market and rapidly spreading its footprints across the globe.

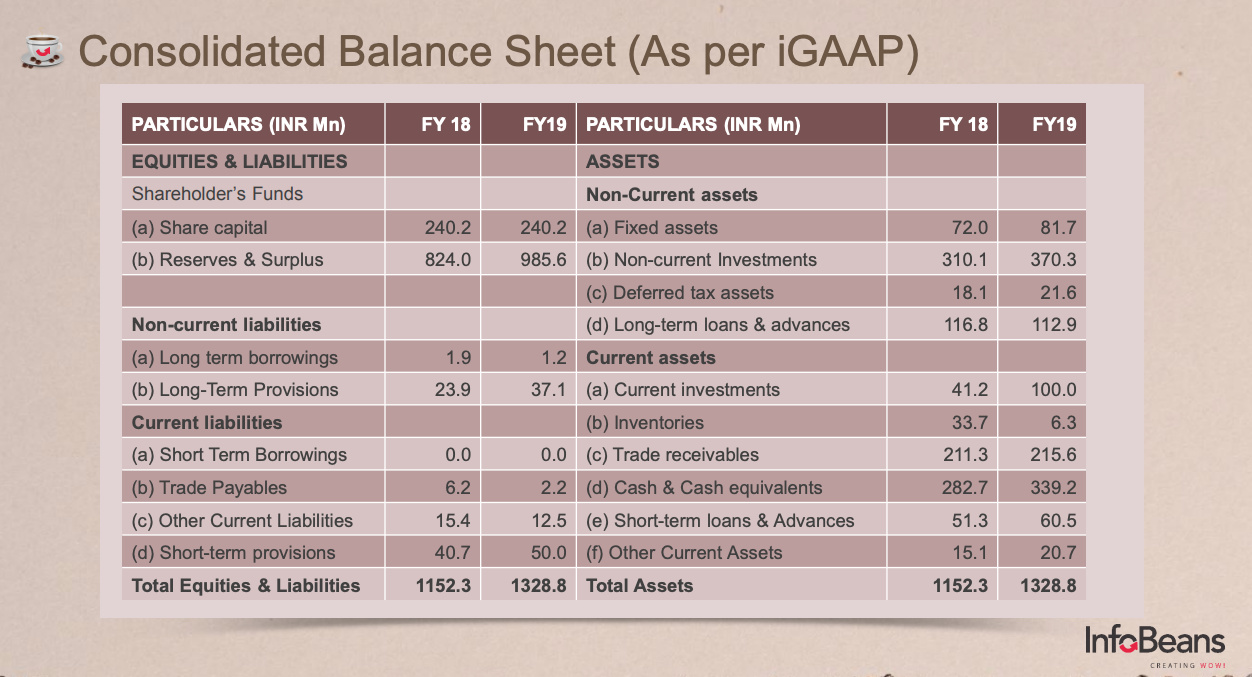

Effectively company has 34 cr rs cash in hand and have total investment (long term/ short term / non current investment) of 58 crore. Company has 98 cr reserve and surplus. It has zero debt ( against long term/ short term provisioning).

Total cash + investment = 92 cr and current mcap is 170 crore.

It’s topline increased 23 crore to 120 crore in last 6 year

it’s virtual debt free company.

Disc. Initial entry into the stock at around 60 rs. Invested.

Risk: In IT industry, technology risk is always exist in digital time and any type of global slowdown could also impact in revenue.

4 Likes

is there any value add that this company has which others can’t offer?

What is the client size - are they repetitive?

What is the reason for decrease in margin so sharply in FY19, is it finding it difficult to compete on services?

What are the plans of management to achieve above market growth and how?

Why the name is so similar to “Infibeam”? IS there any relationship between the two, otherwise why would somebody want to be a copycat brand? Even though Infibeam is hardly a brand, given the value destruction in the stock.

There is no relation with infibeam. Most of IT companies start with Info name can not be Infosys. Infobeans is independent company and has no relation with any listed company. Pls go through investor presentation to get formation, corporate and promotor details.

4 Likes

SME companies are small market cap size listed companies which can give multi bagger opportunity as per company business growth and scale up. As we know, We can not compare SME companies with main market listed companies. This company has been posting profit and seeing good growth in topline and bottomline.

As said in their investor presentation, they have repetitive clients and added 17 new clients in this FY 2018-19.

These new clients revenue will reflect in upcoming quarters.

In FY-218-19, Infobeans shifted to their new campus in Indore and opening new offices to get more business in many countries which adding starting cost. Company has huge cash in books and this expansion strategy should not reflect on company financial health. Although Infobeans has declared 1 rs dividend for 2018-19.

Waiting for annual report and investor call to get more details.

2 Likes

I had researched this company few months back and I dont have buffett like memory. So whatever I vaguely remember posting it here. I believe promoters are from IIM Indore and from Indore. Promoters raised the funds for an acquisition in US but were not able to find suitable company which can be merged with company’s culture. Promoters seemed to be honest guys. I wanted to invest but could not as I was not allowed due to low liquidity.

Any update on why the margins dipped this quarter? Margins were stable in last many quarters. Not sure if this is one off. I don’t see call transcript. If you have or can acquire that information, it would be helpful

It’s going to migrate in main board market. Now you can buy.

Company is increasing their global presence and opening offices in many countries to get more business. It’s adding starting cost in company books which eventually will be benefited in long term. I don’t see any other expenses which putting extra burden on P&L. Company is virtual debt free and huge cash in hand. Company is on expansion spree. Be ready to take ride with company growth in coming years.

Hi Anand,

This company is a good candidate for further research. However, just wanted to let you know that using word like “multibagger” or “ready to take ride” etc feels like you are marketing this company here. Are you anyway connected to this company?

3 Likes

I’ve been holding shares of this company since it’s ipo and only have this connection. My view may be biased. We usually mention multi bagger, bull run, taking ride etc for continuous growth stock. Many growth stocks like Bajaj finance, Honeywell, TCS always give multi bagger opportunity and these companies are big giant in their sector. We can’t compare SME company with these leaders but always encourage investors to invest for taking long term multi bagger benefits

This company need to be researched in deep level. Never ever seen such strong balance sheet in any SME. Expecting good run in coming years as mentioned in above comment. It’s long term holding.

What you think about promoters?

IIT n IIM people can also fudge accounts.

1 Like

fully agree with you in Indian market scenario after seeing Leel, prabhat dairy, vakrangee etc.

Anil Ambani is also MBA graduate and see how his empire collapsed. Even one of MNC Richoh India (one of leader in their sector) also shutdown their India operations due to same issue.

In Indian market, It’s very difficult to find honest and investor friendly promotors. Even you find good promotor company that will be expensive.

Why DMART is expensive ? Promotor is one of big reason.

I heard from people and their company workers that Promoters are honest people. One promotor live in USA and handling North America business operations and customer relations.

Need to keep eagle eye on company corporate actions and growth plans in upcoming quarters.

I’ve had a chance to talk to all 3 of them. FWIW, my impression:

-

each one has a clearly defined individual charter, with little overlap

-

each one seems to know their area well (Mitesh - Sales, Avinash - HR/Finance, Siddharth - Eng)

-

The move to NSE board is an example of something that was mentioned on earlier calls, and then actually is being done

-

On the flip side, the inorganic growth plans for which money was raised haven’t materialized yet. This has led to a ton of cash on the books. If/when the acquisition happens, there’s going to be risk, because the size they’re going after is a reasonably % as compared to their own revenues (120cr rev, and looking to buy someone with 40-50cr). Integration, margins etc…

-

The company has been around for a while (18 years?), and has just had its first 100+ cr year. Management and process ability and to deal with scaling beyond is unknown

3 Likes

If someone spends some time , they can easily see the kind of IT these guys are part of. Some of infobeans’s line of work are highly competitive now as we see many run of the mill companies. Doing a cms in Drupal for example is a good example of low grade IT that has too much competition. Please read and explore before investing.

Disclosure: spent only 1 hour and not invested.

1 Like

From the investor presentation:

- 17 clients added as compared to 8 clients in last fiscal

- 7 Fortune 500 customers out of 49 active customers, of which 3 Fortune 500 customers acquired this fiscal

- 90%+ repeat business

Is a cost advantage (Indore primarily) their only USP that’s getting them this growth (there are a million ways one can define “repeat” business, so we have to take the 90% with a pinch of salt I think)?

Yes, building a site using a CMS, or automated testing aren’t exactly “difficult to move to another client” type engagements. Deep product engineering is. It would be a great question for the next investor call/meet.

Disclosure: Invested, tracking exposure.

Infobeans will be migrated to NSE mainboard from 15th July’19

InfoBeans Technologies acquires philosophie group Inc of USA in a cash out through its wholly owned subsidiary InfoBeans Inc

Infobeans-Technologies-Ltd-Acquires-“Philosophie-Group-Inc.-USA-1.pdf (782.7 KB)

Infobeans-Technologies-Ltd-Acquires-“Philosophie-Group-Inc.-USA-1.pdf (782.7 KB)

3 Likes