New Investee company. ShoeKonnect is a B2B marketplace for shoes focused at the unorganised footwear retailers.

1 Like

A few thoughts I have on Info Edge.

Sustainability of Naukri?

Naukri has competition from LinkedIn, iimjobs & other players. Tech businesses tend to have shorter life cycles as compared to other traditional industries. Disruption happens frequently, particularly when there is a change in channel/medium (Desktop to Mobile - Facebook had to acquire Instagram & WhatsApp to remain relevant) or technology (Several examples in ad tech where technology changes every 5 - 7 years).

Naukri seems to have seen its best days already. Recruitment space is ripe for disruption. Although hard to pin point where exactly the disruption is going to come from but it is coming for sure.

Info Edge’s continuous ability to make great investment decisions?

Zomato and PolicyBazaar have turned out very well but apart from that there isn’t much. VC is a tough business and IE is in a difficult spot. They have a $2Bn valuation and people want to see how can it reach $5Bn in 5 years.

VC business needs to have 3 things at the very least:

- Ability to raise capital (Which Info Edge has from Naukri cash flow)

- Great Investment team

- Great deal flow

While I can’t comment on the capability of Info Edge’s investment team but honestly I don’t know the names of any of their team members while I know the names of most people working at a Sequoia, SAIF, Matrix, Nexus, and so on. Which at least tells me that their deal flow is not that great. They can still deliver a 15-18% return on their investments and that kind of returns in US would mean you are in top quadrant however in India we have the likes of HDFC bank or HDFC Life where you have to just time your entry well to lock in a return of 15-18%.

Capital Allocation / Financial Investor Vs Strategic Investor Dilemma

I am not bothered about high other income or high amount of investments on balance sheet. What bothers me is that pulling off a VC fund through IE kind of structure is supremely difficult. Key question is are they a strategic investor or a financial investor?

If they are a strategic investor then I would want to see majority ownership. This approach would be similar to what Berkshire Hathway does. Acquire majority stakes in companies and businesses they like. If IE’s calling card is expertise in tech, then they should be consolidating the sub sectors of technology they are present in and enter into other sub sectors where they can turn around things the way BH does. There is a great opportunity in reducing the overall marketing cost for 99acres for example by consolidating real estate classifieds and start generating cash there.

IE does a bit of Amazon i.e. incubating new businesses which is great and should continue. However their VC investing model is flawed because when there is a rockstar performer in its portfolio (like Zomato) then IE is not be able to participate in future rounds and maintain/increase its shareholding. In fact IE is forced to sell part of its stake. And this also implies when portfolio companies are raising really large amount of money (Like >300crs) IE will not be able to participate leaving most of its large amount of cash unutilized.

At the same time in companies which are not doing well, IE would be expected to keep on guzzling more money. Now there is a valid argument that if Info Edge doesn’t give up its shareholding in rockstar performers then it would be difficult for its investee companies to raise future rounds of capital. One way to move away from this dilemma is give away ROFR and other rights which can potentially lead to sub optimal exit for a portfolio company and a dealbreaker at the time of subsequent fund raise. And they should announce this approach publicly so that everyone gets this message and starts considering them more like a financial investor instead of a strategic.

7 Likes

I have personally used few of the products from the IE’s investee companies and do not feel they are of superior quality. This constitutes Zomato(obviously), Naukri.com, Jeevansathi.com, Happily unmarried, PolicyBazaar,and Mydala. Among these the only product whose experience I enjoy is zomato. All the other products seem to be second or third preference for me and a bunch of my friends who are active internet users. Though this does not really help me in making an investment decision, it does reduce my conviction in the future of IE’s portfolio. Also the way 99acres dealt with housing.com’s disruption in tech does not instill a sense of great innovation from them.

Having said all of that, since one big win can turn the numbers around, I will surely say that the zomato gold experience has been quite stellar. I find very good restaurants in the list and have frequently found myself choosing restaurants with zomato gold over the ones without, simply because I can save a quick buck. I have also found that people who have bought zomato gold are really happy with it and are actively campaigning it in their networks. There was extensive media coverage about initial resentment in the restaurant owners about dealhunters clogging their restaurants with zomato gold but I spoke to a bunch of restaurant owners in the last one month and they seem quite happy with the increased footfall. And since zomato is still privately funded, VCs typically tend to assign extremely bloated valuations to minor increases in vanity numbers due to FOMO(compared to the harsh scrutiny on publicly traded companies). I feel that the stake in zomato held by IE might see steep jumps in the near future due to revenue numbers from Zomato Gold.

Been an investor in Info Edge for a year, essentially going by the option value of subsidiaries logic. While I agree that management is good, core operations(Naukri, 99 acres, Jeevansathi, Shiksha) are more than factored in the price and value is essentially a function of how the investments do (again mainly Zomato).

I think the company was lucky to get into some good companies before the PE space really took off, today with the likes of Softbank, Tiger Global, IDG & Ant offering stratospheric valuations I doubt too many promoters will prefer Info Edge as an investor. over them So essentially the investments they are having Zomato, Policybazaar, Meritnation are what one needs to take into account.

I was very upbeat on Zomato, it is a monopoly in the food social/ review market place and seemed to be moving towards to profitability based on the advertising model. Further Deepinder Goyal seems to be a very level headed guy and the only CEO of a startup who has publicly said that discounts do not work, they are not a strategy for customer retention. Even in the food delivery space Goyal had earlier written in his blog that their strategy would be to depend on restaurant owners to deliver (correctly stating that they could never match the economics of a restaurant delivery boy who is also working there) or through third party delivery agencies (who will do both food delivery in peak hours and non-food other times). Essentially strategy was to leverage their position as the app one used to check a restaurant to get into food ordering without setting up one’s infra and avoiding cash burn as much as possible.

In last few months however due to Runner their main delivery partner going bankrupt they had to buy him out and get into their own delivery infra. Further I feel strategically due to Swiggy getting a lot of funding at higher valuation than Zomato as well as Ola/ Foodpanda & Uber Eats getting into the business in a aggressive way, Zomato has also had to step up marketing, customer acquisition costs in the food delivery space (discounts are also there though lower than others). Now I understand newer investors like Alibaba are very gung ho on food delivery and making the company invest a lot in those areas, which is reflecting in the hiring they are doing at all levels.

Food delivery IMO is a black hole which is going to take up a lot of cash. With only Swiggy & Zomato one may have hoped for some sanity eventually but with Ola & Uber all bets are off. One only has to look at Ola’s numbers of some 4000 cr loss on a turnover of 1300 cr. As a businessman I am not sure whether I am more confounded or offended !! After these numbers they are willing to invest humungous amounts in what IMO is a business with nebulous co-relation to core business. While Zomato may still get higher valuations, food delivery undoubtedly is a space which will see growth in turnover(which is all PE’s seemingly care about) I do not have the appetite to stomach the losses that IMO seem inevitable.

Disc - Invested but slowly exiting…

7 Likes

Another interesting video highlighting acquisition strategy of Info Edge

- We have very little role in success of our investee companies, all credit to the entrepreneurs

- What we look for while making investments

- We look for clear value proposition

- Eg of policy bazar, showing insurance comparison is beneficial for customer

- Good founding team

- Evidence of some natural traction early on

- Solving customer problem

- We don't look sector wise or top down, we prefer to look at individual companies at whats bubbling up

- Zomato has got some natural structural advantages as its customer acquisition cost is very low due to its restaurant discovery business being the most popular

- Funding is abundant for winners in a sector and scarce for others who aren't able to scale up

7 Likes

Hi @phreakv6, @lastgenesis, been enjoying this discussion, naukri is a pretty unique bet in the Indian market. I work as a VC, so I’d like to add my two cents.

-

I would not buy into InfoEdge for option value. Firstly, InfoEdge is no Softbank or Naspers - it doesn’t have the financial clout and ability to raise funds from public markets like these entities do, or the ability or appetite to do huge growth rounds - these tech / corp investing conglomerates are mostly late stage investors who gain substantial stakes in market leading tech companies i.e. already highly valuable companies. Secondly, even Softbank and Naspers have significant holding company discounts applied to them - Softbank’s market cap of ~$100 BN vis a vis their ~29% stake in Alibaba worth ~$130 BN - and thats for a large operating business and holding in a publicly traded tech behemoth (they also have Yahoo JP) besides other PE investments and a whole bunch of startup deals - so the valuation of these companies globally at least is not the sum of their parts. Basically the option value of their startup investments is fully discounted. Naspers similarly has a ~$105 BN market cap and the value of its residual stake in Tencent (after divesting 10%) is $160 BN! We also know of Yahoo, whose stake in Alibaba did little to save them.

-

Secondly, as last genesis points out, they were v fortunate to get some stellar founders and businesses for cheap early on, which they will not win in today’s fund environment. There is enormous competition in the PE / VC space and it is highly unlikely any quality company will be available to a strategic / non-financial funder for a cheap price unless they’re the last door they knock. For tech option value, I’d actually pick Reliance Industries and Jio / Media if and when they get listed - they are the only players with the ability and intent to follow a similar strategy.

-

I am actually v bullish on Zomato personally, and while this will likely lead to a nice payout to InfoEdge sometime in the future, I can’t see how this will percolate upto shareholders in any significant way. Zomato and Swiggy will continue to aggressively fund raise, and if I had to guess I think they’ll be largely taken out in the next rounds of financing - so if there is money to be made it will be made soon. Its unlikely they will be permitted to remain in a significant capacity in Zomato by the next set of large rounds ($200 MM+). Ali Pay has already reduced them to 30% - this transaction also seems to have happened at a secondary valuation of $300 MM ($50 MM consideration for 16% stake as per public reports), which is a huge discount to the primary issuance (differing secondary and primary valuations is common in venture deals) - so this casts a doubt on their ability to monetize their illiquid stakes to their full value.

-

To lastgenesis’ concern about the viability of the food delivery space - you are correct that it will be a cash black hole, but both companies will raise substantial rounds as there is tremendous interest in the space. However, the model itself is v viable and has healthy margins - there are at least three listed companies I know of globally - Just Eat (UK), Delivery Hero (Germany) and Grub Hub (US) - each with hundreds of millions in revenues, profits and valued between $5-11 BN (Yelp is also listed andvalued at $3-4 BN) . Meituan, which is considered the largest, is valued at $30 BN privately. So there is plenty of room to grow, and great businesses to be built.

-

PS: I think Naukri’s actual classified business has a lot of value with some revamps, but its very overpriced at current levels.

17 Likes

great points, agree totally. Info edge is a good company, in addition to Naukri I am also hopeful for 99 acres as real estate picks up, but at current valuations there is no point in holding it. It was 3-4% of my portfolio but i have exited around 1300 - am open to investment if valuations come down.

My optimism on Zomato in addition to the great product was based on the fact that the advertising business is a great potential money spinner and they were kind of not so aggressive in the food delivery space (atleast as far as putting their own money went). Zomato I agree valuations are likely go up in subsequent rounds but like you point out Info edge will not get full benefit and to a much greater extent I am not comfortable with the entire start up philosophy of only burning cash with no profit in sight. Till cheap money is there all is cool but when the next downturn comes (which to be fair doesn’t seem to be coming in near term), a lot of guys are going to be caught naked…

2 Likes

A recent purchase by Zomato and some articles outlining their strategy going forward. Since Zomato is a big part of Info Edge’s investment portfolio (28%) outlining the same here

Articles outlining Zomato’s future strategy and what makes them different from their competition

I did some work on understanding this opportunity better. I studied the Annual Report of Sysco (the global leader in sourcing business). Here are my notes for the same

1 Like

It is actually the case where Mr. Hitesh Oberoi is looking into the internal businesses namely Naukri, Jeevan sathi, 99acres etc and Mr. Bhikchandani along with his team is looking into other investee companies and new oppportunities.

Which is a great model to be considered, as they have their focus on their respective businesses.

2 Likes

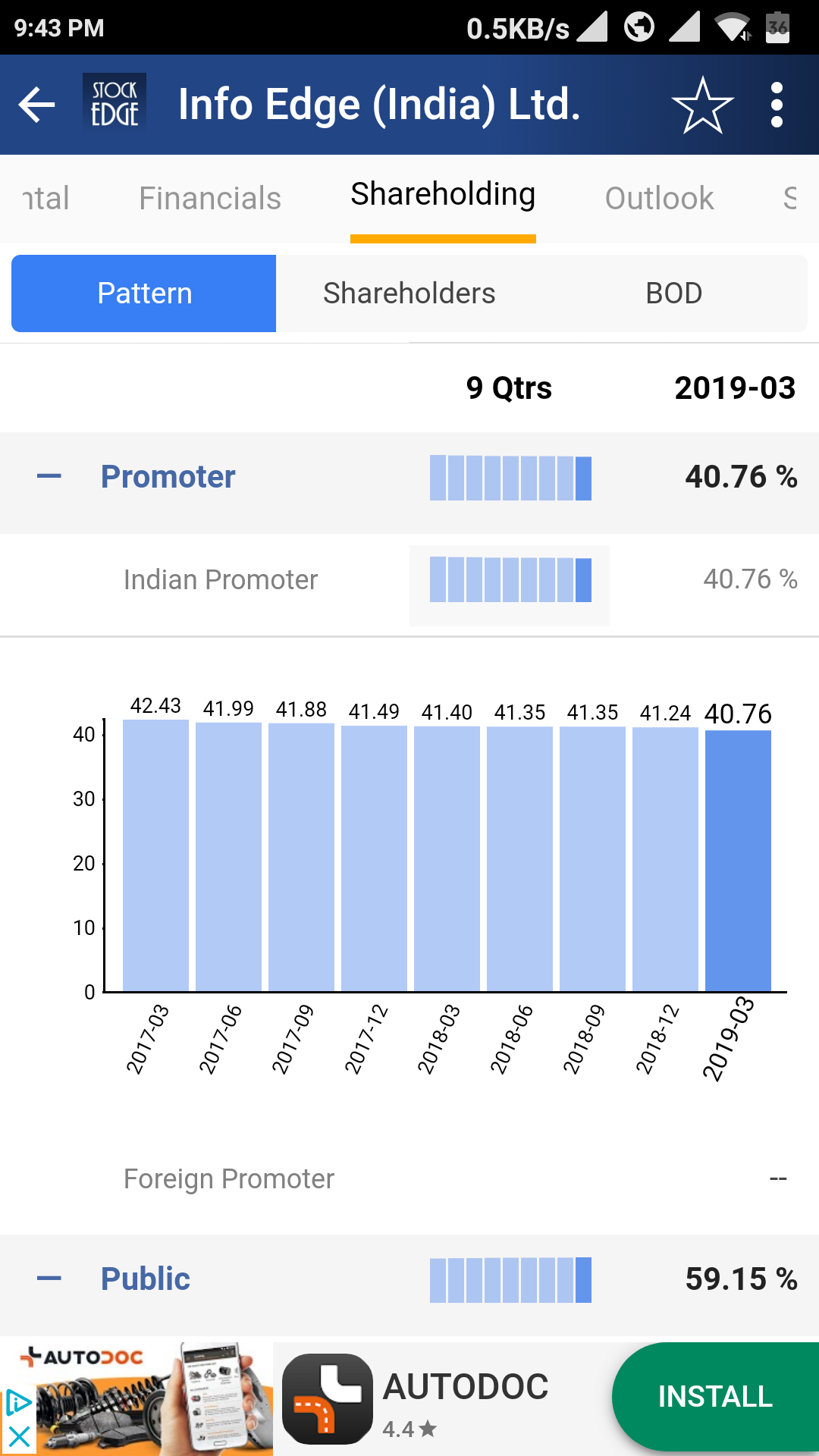

Over the last few weeks there has been disposal of shares in open market by promoters groups. Can this be a red flag ?

Looks like Happily Unmarried and sub-brand Ustraa (grooming range for men) (Info Edge holds 47% of HUM & Ustraa) are doing rather well for themselves.

In fact Ustraa seems to be doing better than Happily Unmarried, as some of its products have reviews running in the 500-700 range.

https://www.amazon.in/stores/node/3851372031

This sort of broad based disposal by promoters is never a good sign, so its better to be watchful.

2 Likes

Guys, whats the reason for such high valuations for a company with unpredictable PAT over the years

1 Like

please post the screenshot of selling by promoter, unable to find anywhere.

Revenue goes 3x, while costs go 6x.

How do you evaluate the prospects of a company that’s losing money so fast? I think I’ll never understand the world of VC/PE.

1 Like

You have to look at it in a scenario of ZIRP/NIRP where billions of dollars are looking to build assets of tomorrow. It’s like trying to figure out the utility value of art - it’s futile. It might be worth nothing for someone while it could be worth a lot in certain circles of “Art collectors”. I am not going to say one is better than the other but that’s just how it is and its merely an observation.

Coming to Zomato, as they improve the number of deliveries per rider/hr due to operating leverage - its currently at 1.4 (improved from 0.9 last year) and reduce losses per delivery from the current Rs.25 level (will happen over time with habit building), they could even get into the green in about 5 years time. The last mile cost per delivery as well could improve in the long run if fuel costs drop (this is inevitable with long-term outlook for oil). When looked at from a unit economics perspective, it doesn’t look very bleak.

The key is that they have a business that solves a real problem and adds tremendous convenience. Over time, meals delivered per household per year is bound to go up as people inevitably outsource cooking. All this will add good operating leverage going forward. The key though is cheap long-term money - long as it remains that way, valuation will keep going up and funding will help the cash burn and grow business. Not judging if its a good or bad thing but saying that that’s just how it is.

16 Likes

why is there constant reduction in promoter holding ?

1 Like

@A_shah - Yes the promoters have been reducing a little bit with every passing year. I don’t know if its their habit of selling stake in Investee companies that is carried over to the holding company or something else. It is not terribly concerning but something to think about. However, retail holds around 2% and that has been the case for long here as most of the holdings are with FPIs and MFs. At least its not a distribution to retail, which would be a thing to watch out for here. My guess - it could be because they are finding small promising businesses with higher RoE elsewhere than they can manage with the higher base here.

6 Likes