Textile companies don’t generally have a good run. One could be a supplier, of sorts, to a textile company and have good prospects. Like, LMW. But, it is a tough nut to crack running a textile conglomerate.

Kitex had a delayed shipping from last but one quarter which got shipped in last quarter which made last quarter results look good but in fact it wasn’t.

Looking at the price-volume chart, it appears that the promoters of the stock have hoarded it at sub Rs.10 levels. Above this level is all a huge question, considering the subdued performance and a few important unanswered questions floating around.

I think due to slowdown in US economy,Indo count might have subdued results in coming quarters.

I feel Indo count should focus more on diversifying and selling their products to the Indian market.

Till then, one can hope of accumulation of stock due to low valuation till the end of a bull market.

I’ve read some of the the transcript of the conference call,and I think the promoters have a good vision ahead

Reading this thread for my understanding about "cyclical businesses and this comment from @Yogesh_s sir simply stands out. As they say, as soon as a cyclical company starts talking about capacity expansion at the time when margins are reducing, sell and run.

2 Likes

His comment on the interest rate is not correct though. The interest paid

by the company is a combination of the interest on loan (which includes

tufs subsidy) and bill discounting.

We can very well see topping down of cotton prices and consequent reversal of margin contraction from textile companies.

“According to the recently released data by the Cotton Advisory Board, India’s cotton output is estimated to be around 377 lakh bales with lower yield of 523.83 kg/ha for 2017-18 against 540.80 in 2016-17. Cotton acreage, however, has increased from 108.45 lakh hectares in 2016-17 to 122.35 lakh hectares in 2017-18. This is likely to be reflected in the increased production of the fibre crop from 345 lakh bales last year.”

2 Likes

Never trust a textile company !!

Can anybody explain the future of indo count industries?

So many controversial news with indo count. Im genuinely concerned as since past 2 years so many bad news with this company.

By that logic, nobody should be buying welspurn india,not even mutual funds.

This is not only 2 years. History goes back to 2008. Try to read what they tried to do around currency risk. Then , they did good things n got rid of poor past. However, knowing history is always important n in tough times the importance of long term character becomes more important than ever. Had taken a position a year back but after reading overall history, found there are better governed companies . By this I do not mean they are frauds, it’s just trying to get a feel of promoter mindset by its actions and factoring that on relative evaluation . The weigtages to these metric differ person to person but knowing history and factoring history before factoring future is more important in my opinion.

5 Likes

Hi, till january 2018 end, indocount was traded in derivatives (Futures & options) and lot if arbitrage funds (who play on arbitrage between cash market and F&O) had stake in it. Now, with stock getting out of F&O these arbitrage funds have to move move out of the stock. You can see the arbitrage funds present in money control. I hope now it is once out of F&O volatility will also reduce.

3 Likes

@shubhams95 IMHO what @jamit05 is sending out feelers that textile balance sheet should not be taken at face value. many textile companies like Raymond arvind century have been listed for 50+ years. welspun too has been listed since at least 2 decades. Except page industries, no textile company has managed to create share holder value. arvind raymond etc. from a 50 years perspective and welspun from a 20 years perspective have at best managed to match sensex returns. ambika cotton, kitex seem to caught in a funk for last 2 years by showing single digit sales growth. Mutual funds have been caught on the wrong foot for herd mentality for failing to do due diligence Satyam being the best example. I do hope indo count proves me wrong on above mentioned points.

Disclosure : not invested closely watching the financials.

2 Likes

At the end we should remember textile is a commodity business,few might become semi commodity. However, in b2b textile, when the end customer is suffering, how can supplier enjoy. Also, last one year has been time when all porter’s five forces have fired from wrong cylinders -

- Raw material prices up

- Realisations down

- Currency was unsupportive

- Competitors from lowest cost neighborhood country eating pie

- End customer having cost pressure

- New supply is easy with new money

So almost every company has suffered and if one looks at 10 year history of companies who have gone through more than 1 negative textile cycle, there are very few companies who have reputable financial metric to show.

Also, I hope everyone is aware of companies over all history (current hedging mess-up etc) to keep enough margin of safety while giving a price as there have been strong positive as well as negative points with the mgmt .

Attaching one ICRA report which is worth reading to understand current pain in this sector . Apparel & Fabric Industry-T-1-October 2017 (1).pdf (1017.3 KB)

3 Likes

Couldn’t understand this when demand from China declines substantially.

results of Indo count out. company have given dividend 20%.more over investor presentation is also given .

Kotak Securities have given the target of 130 Rupees for their client.

For some reason, investors don’t believe when ICIL management talks confidently about future. The numbers don’t speak the same language as promoters as margins have reduced.

I saw the investor presentation shared by the management two days back. They have launched some brands about which I couldn’t find anything online (except for their own website). I am not sure where they are selling these brands.

As per my knowledge, ICIL was about to setup its own network and market its brands independently in US and other markets. I guess they are still lagging behind in this plan. Anyone has more information about their own brands?

2 Likes

They do have their own brands and quality is awesome. I don’t remember the name now but I did buy them for my home. They are available in Bombay Dyeing showrooms and the quality of the merchandise is much superior to Bombay Dyeing merchandise.

I was talking about ICIL selling their branded stuff in US Market.

Bombay Dyeing stopped producing their own bedsheets and they have shifted focus to real estate. As per one report i read, they will probably remain in marketing only.

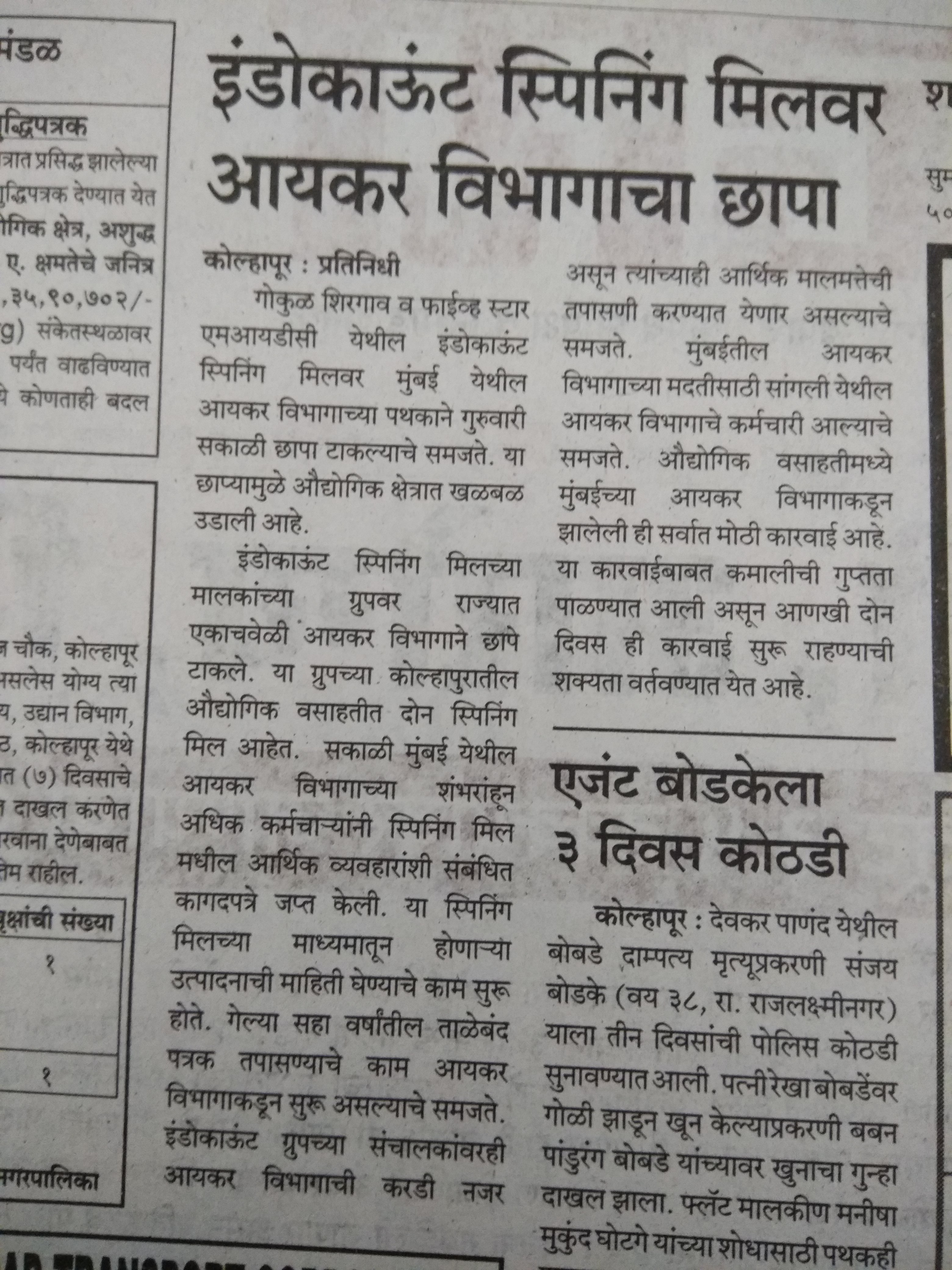

Are there any insights to be drawn from this kind of a news for an average investor?